The financial services firm has quite improbably become one of the fastest growing companies on the planet. It lists its shares on the Nasdaq, is incorporated in Las Vegas, but for all intents and purposes runs its operations mostly in Kazakhstan.

As a December investigation by the Foundation for Financial Journalism showed, Freedom Holding’s ballooning profits have resulted from baffling and opaque business practices that its management is not keen to discuss.

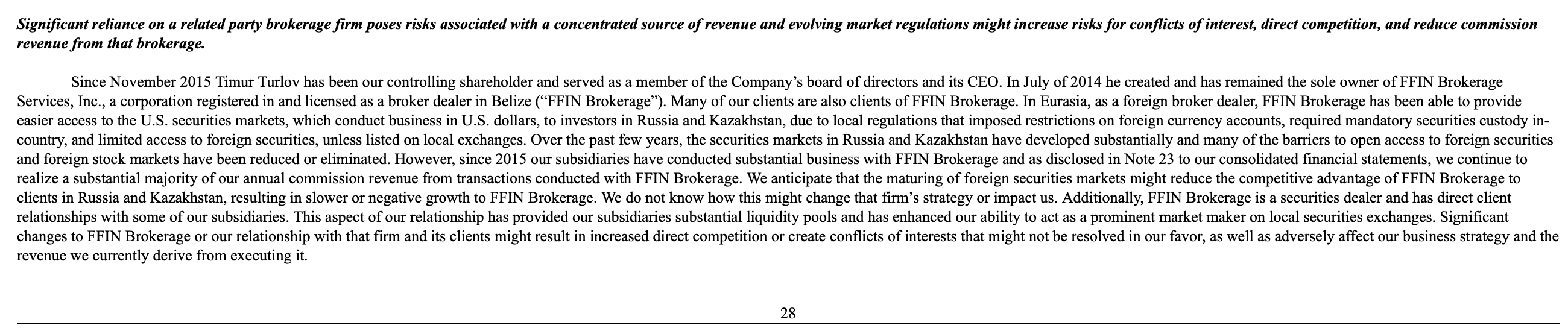

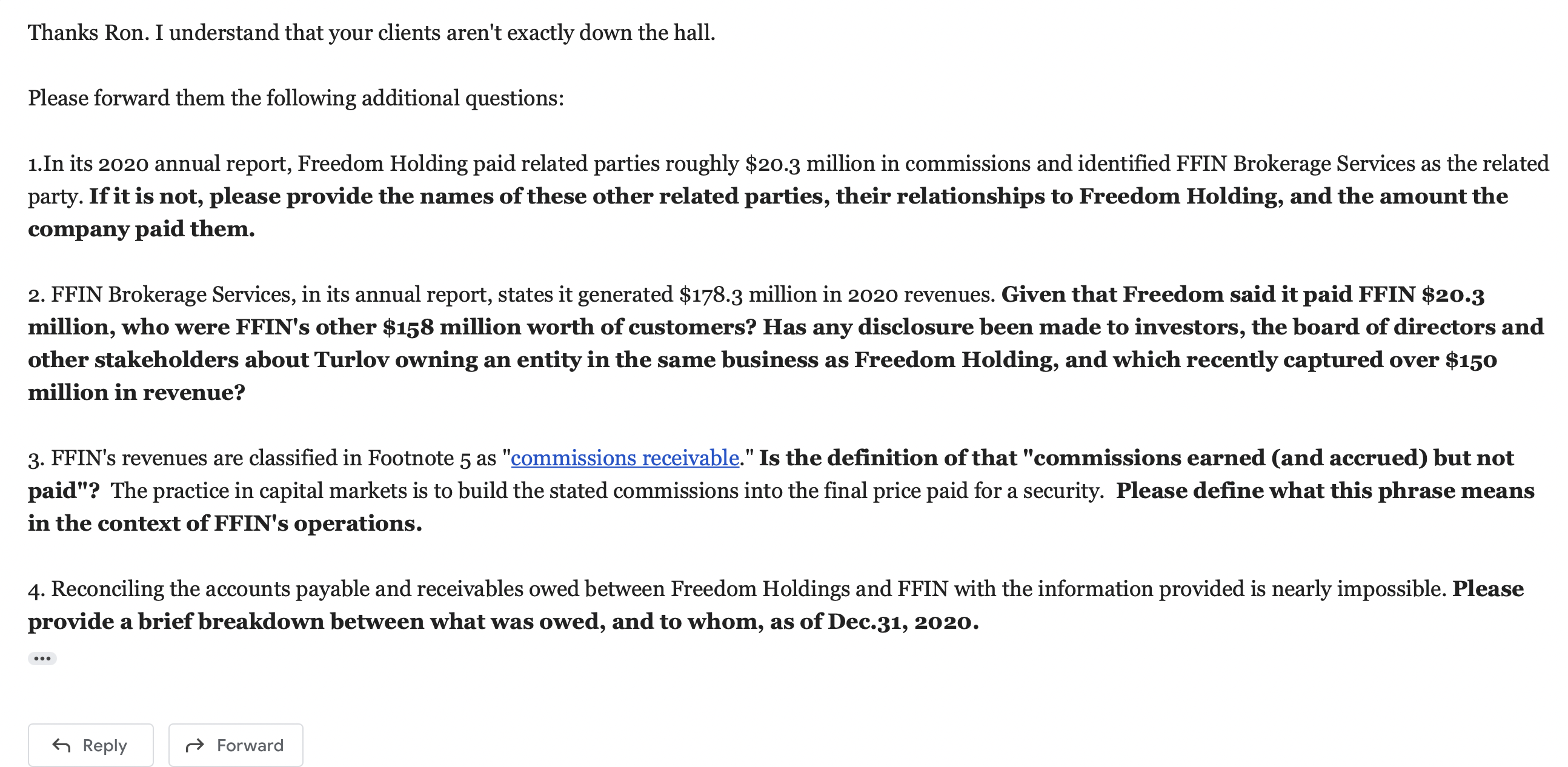

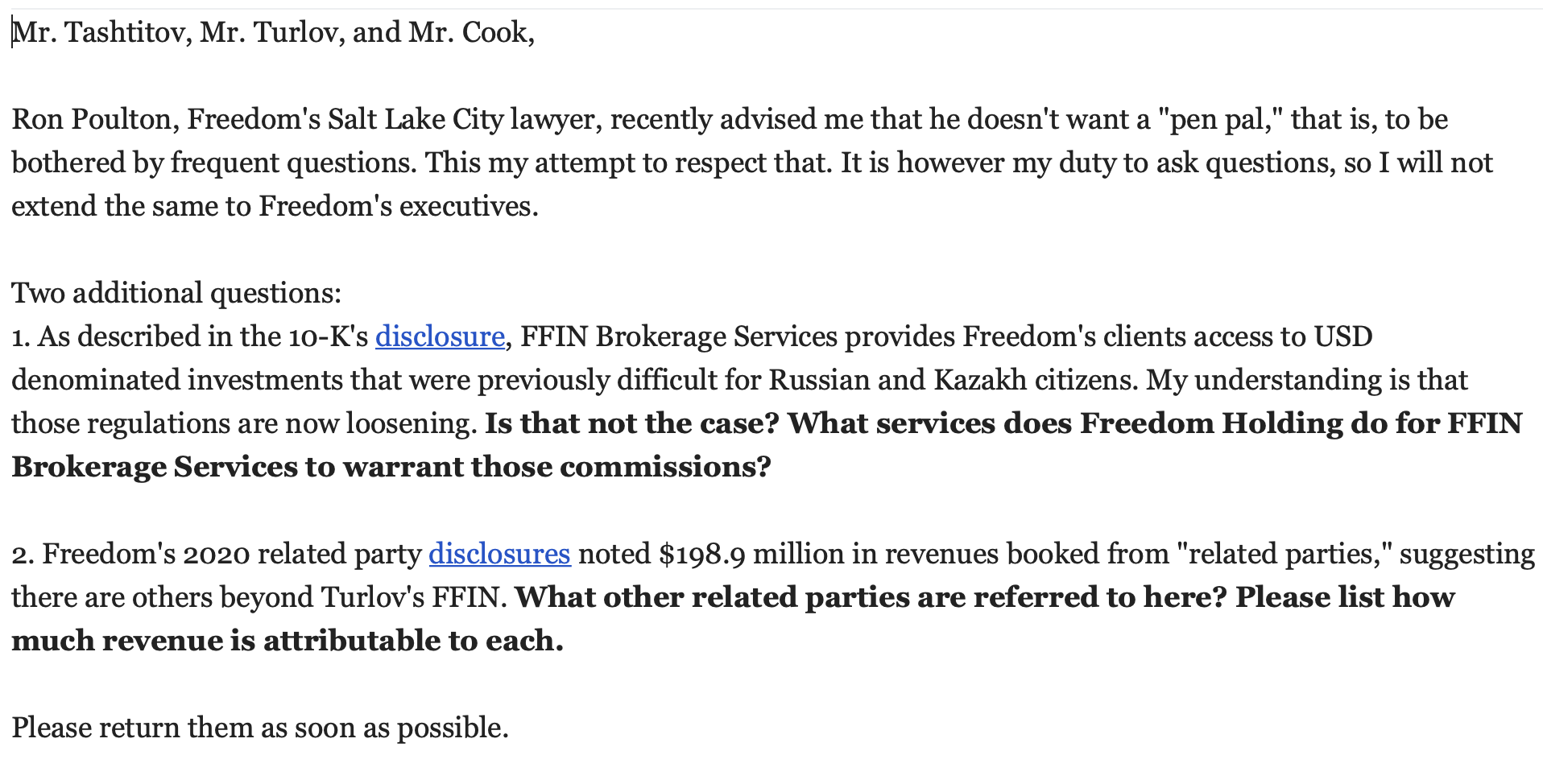

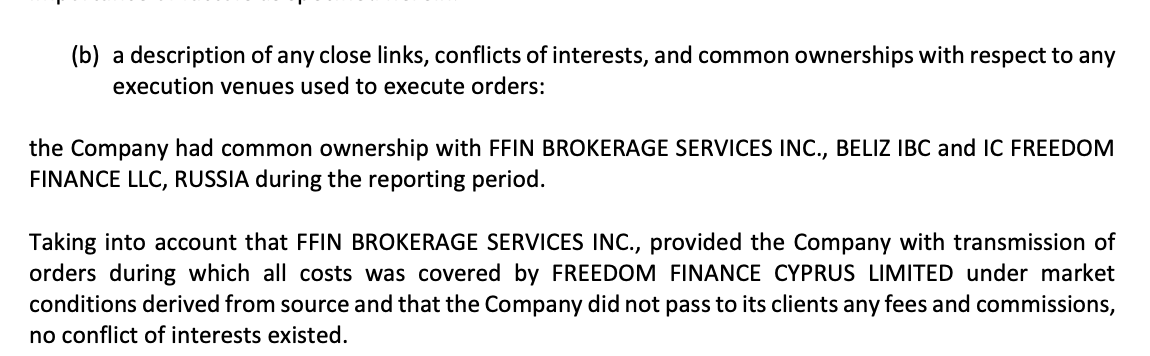

Among the arrangements is Freedom Holding’s close connection to FFIN Brokerage Services, a Belize-based securities trading firm owned by Timur Turlov. He also is Freedom Holding’s billionaire founder and majority shareholder.

Even the most seasoned investor has probably not witnessed related-party transactions of the scope of FFIN’s dealings with Freedom Holding.

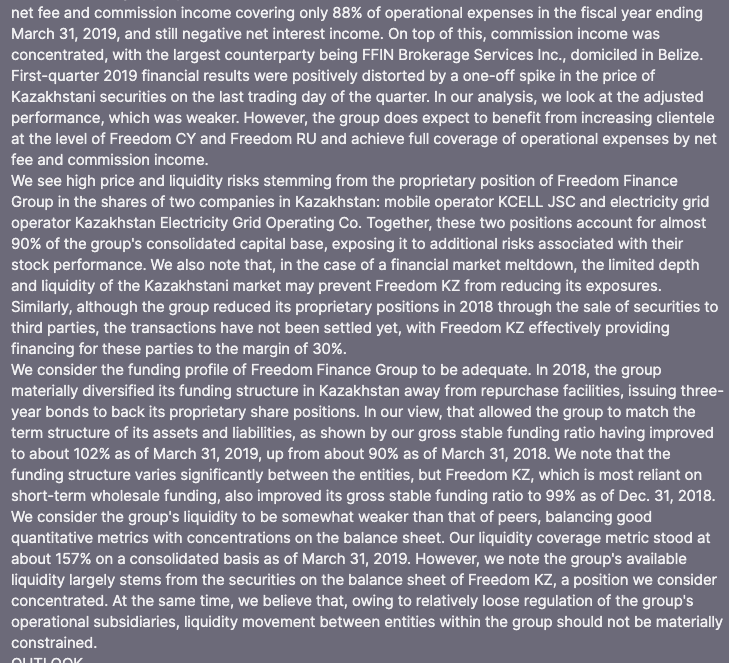

Last year more than 56 percent of Freedom Holding’s revenue came from FFIN commission payments, and in 2019 they represented over 65 percent. What Freedom Holding does to earn the commissions is not readily apparent, however. Yet the two companies are so intertwined – Freedom Holding’s senior managers use FFIN email accounts – it’s not clear the two companies are separate in any real sense.

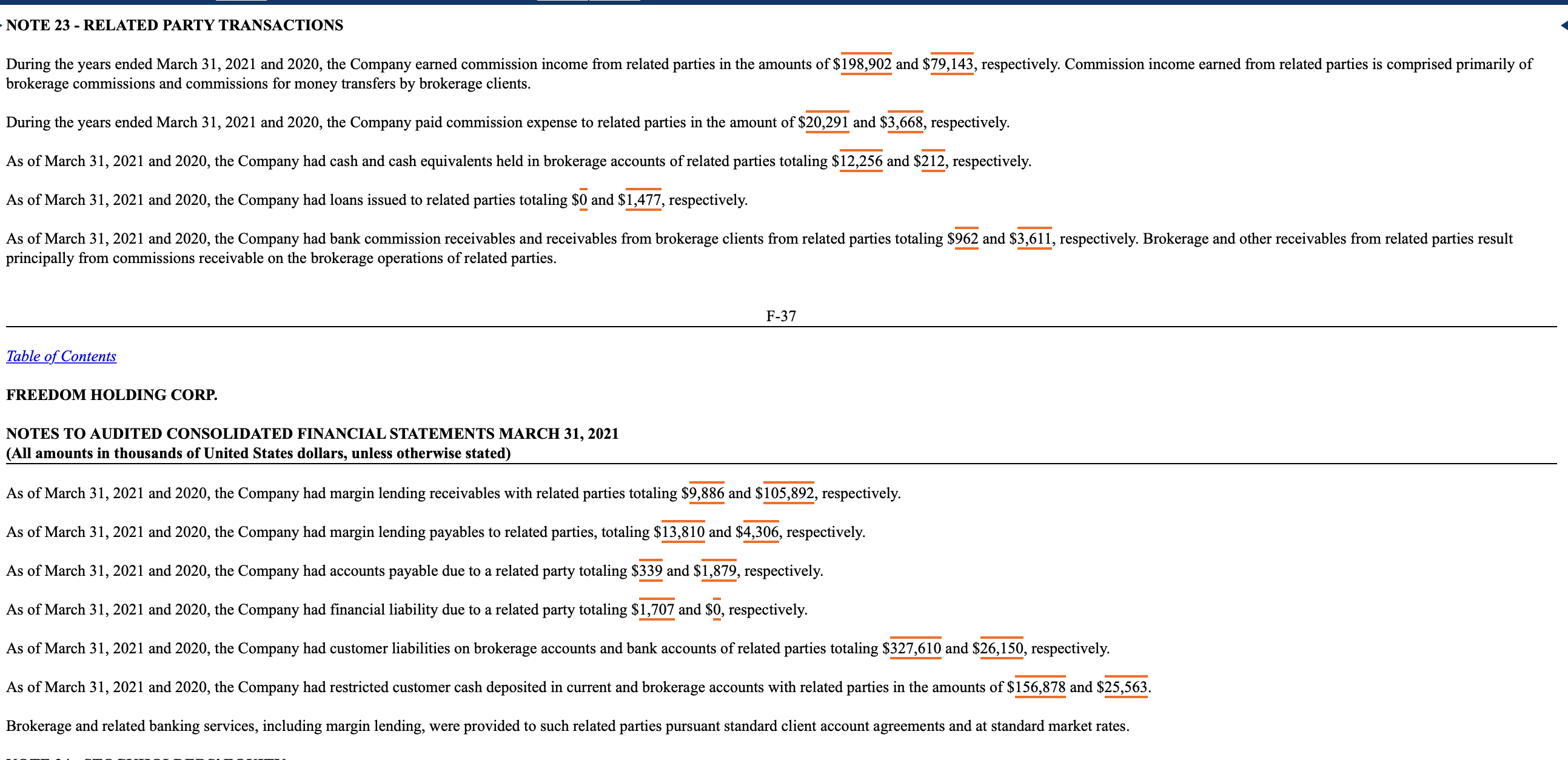

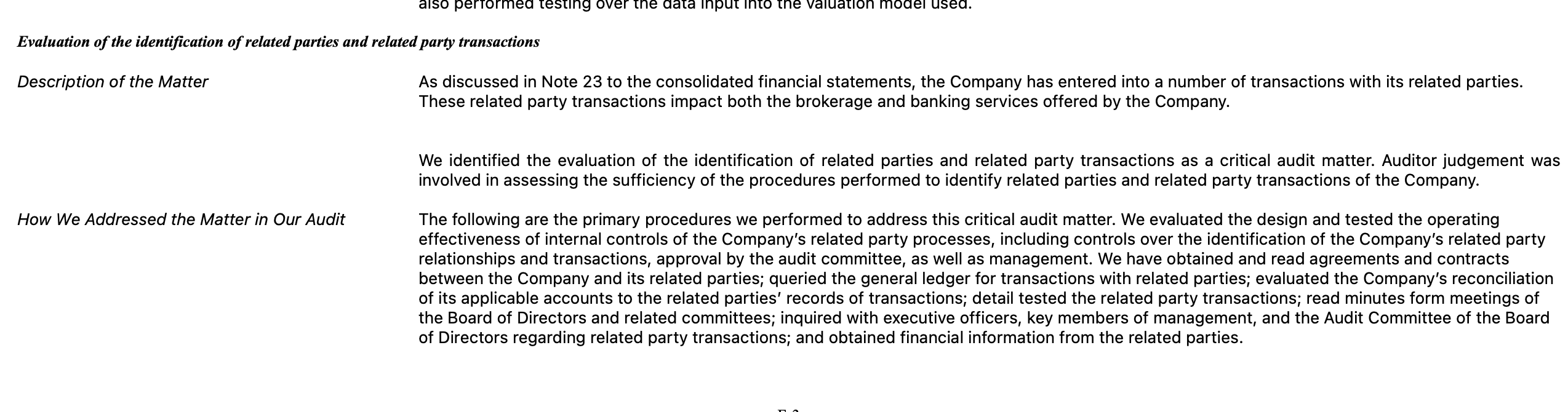

In June, Freedom Holding for the first time disclosed in its annual report its relationship with FFIN, categorizing this as a risk factor for investors to weigh before buying shares. Highlighted as a matter of particular interest: the portion of revenue that Freedom Holding received from Turlov’s company. In the annual report, Freedom Holding’s auditor, Salt Lake City’s WSRP LLC, acknowledged the FFIN connection as part of several “critical audit matters.” (Engaged by Freedom Holding to assess the accuracy of its accounting, WSRP did not weigh in on the propriety of Freedom Holding’s FFIN relationship.)

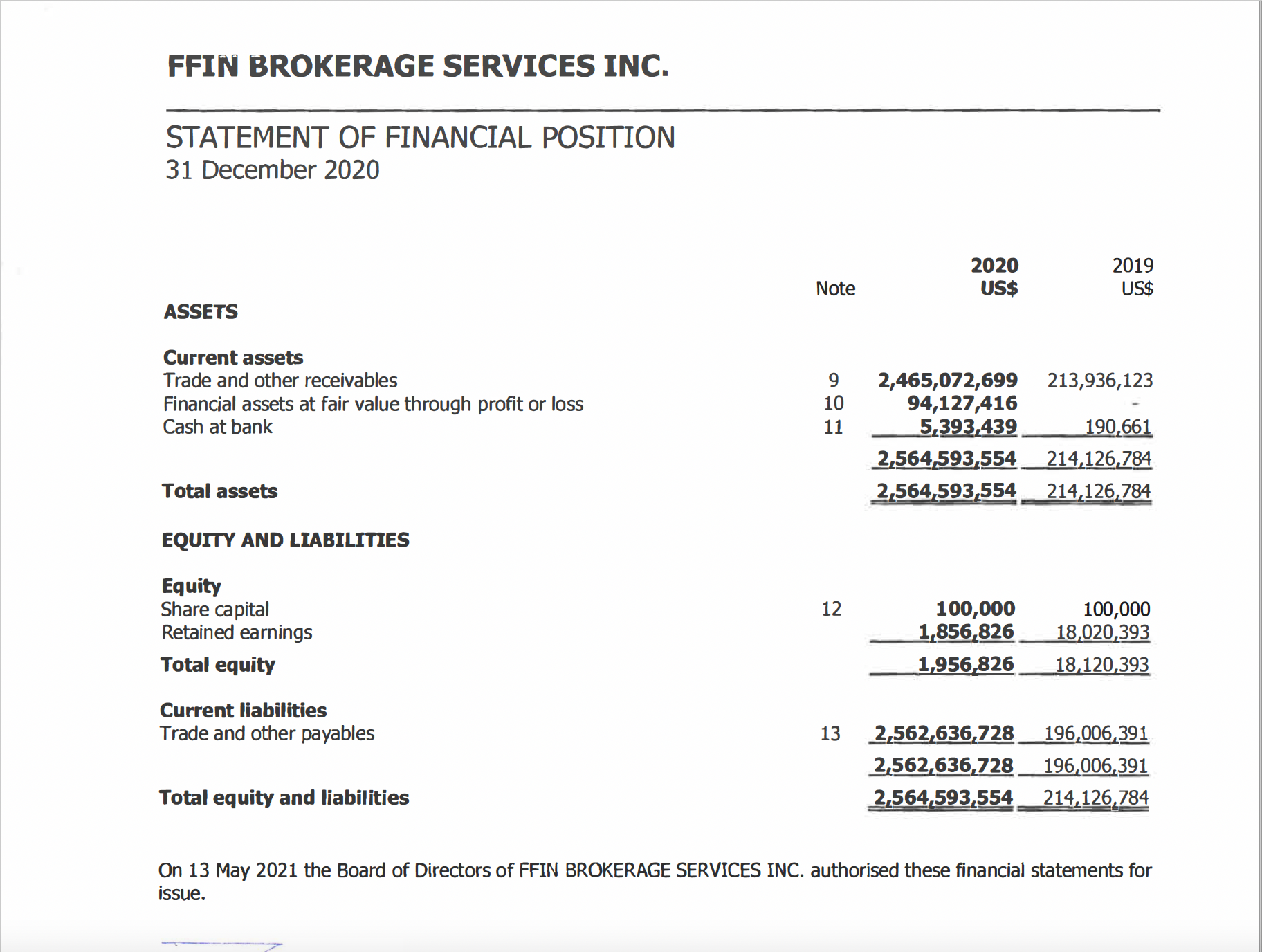

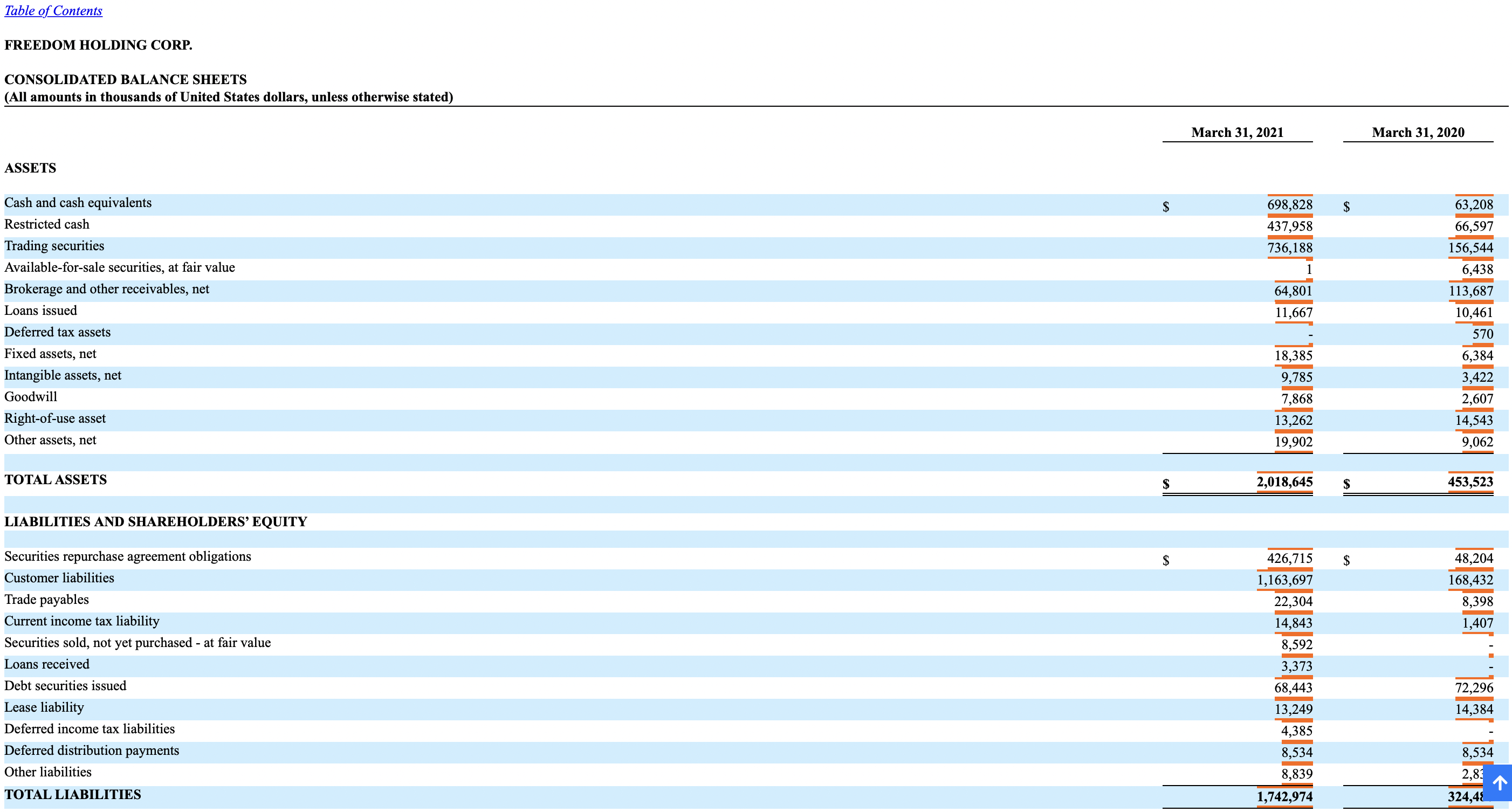

But FFIN’s own annual report, also released in June, ought to give Freedom Holding investors pause: In just a year, FFIN’s assets grew almost 1,100 percent, to more than $2.5 billion. That’s significantly larger than Freedom Holding’s $2 billion in assets.

Were FFIN ever to hit dire financial straits, Freedom Holding could be in real trouble.

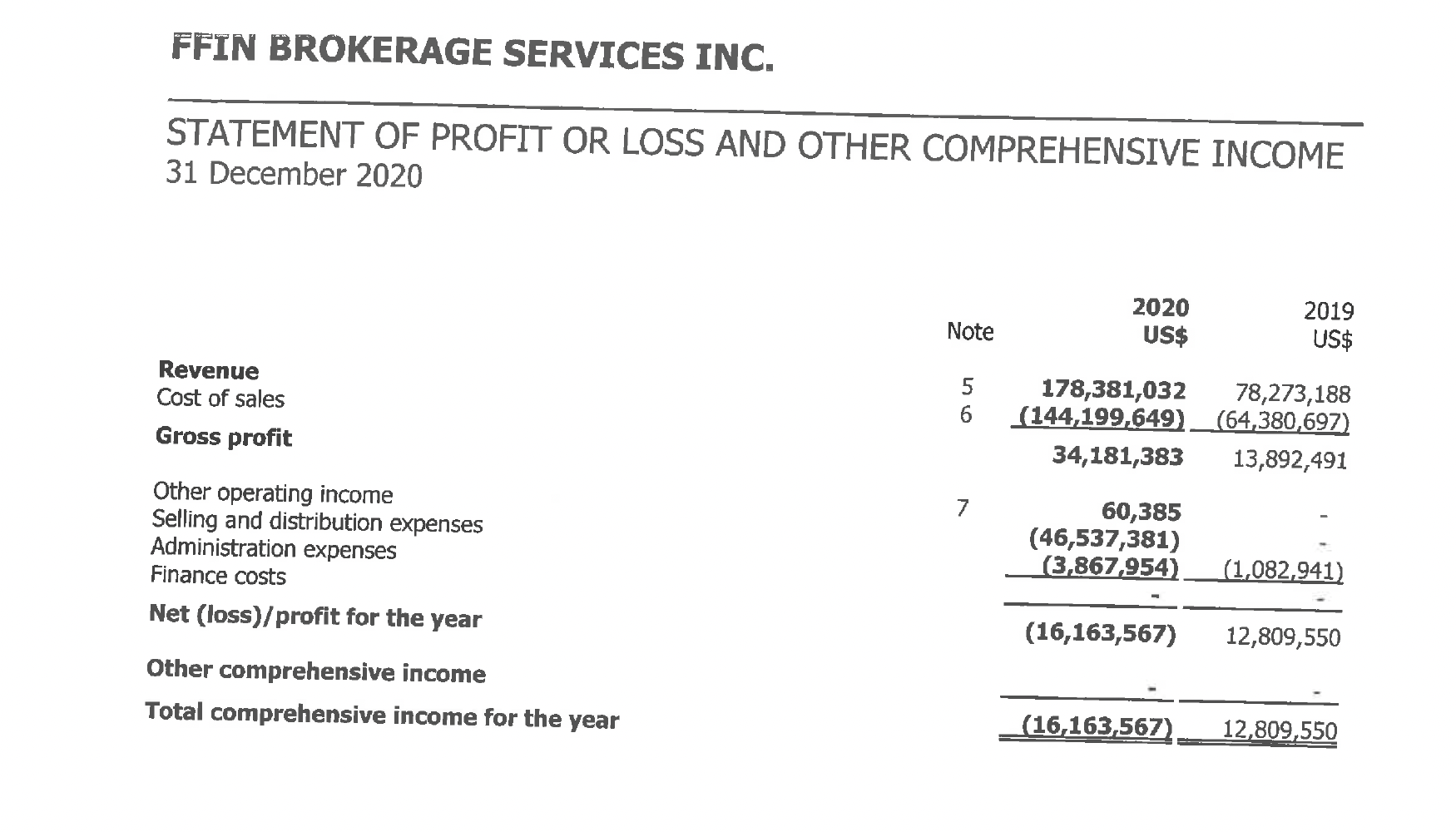

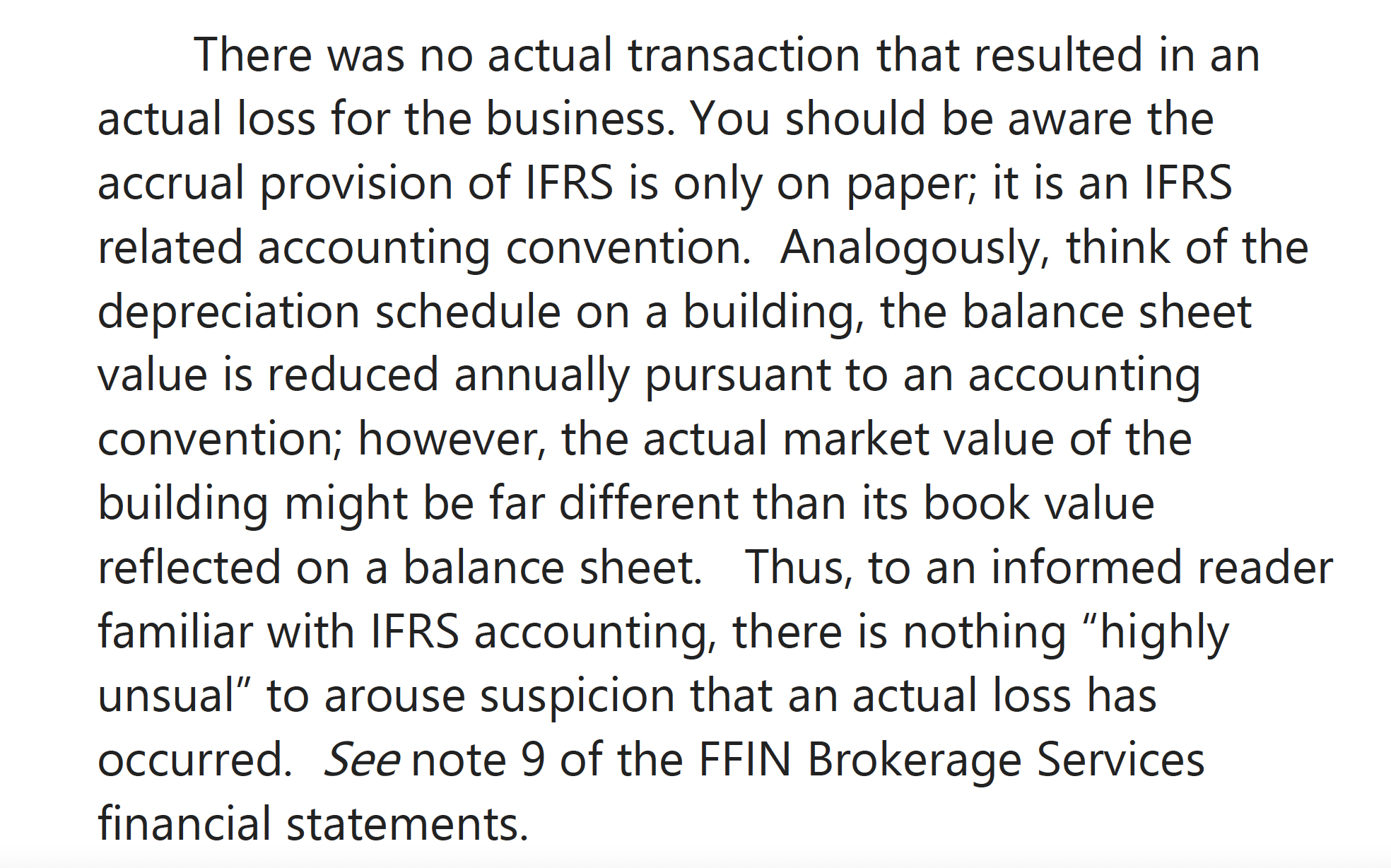

And FFIN’s profits have put substantial cash in Turlov’s pockets: $12.8 million in 2019 and more than $30 million last year. (Although FFIN recorded a $16 million loss last year, Freedom Holding’s outside legal advisor Ron Poulton of Salt Lake City explained that no actual loss occurred. The $46.53 million in impaired trade receivables recorded by FFIN were not losses resulting from clients failing to pay but an “accounting convention” to document a charge like a noncash expense such as depreciation, he said.)

Keeping terms of a relationship under wraps

While the specifics of FFIN and Freedom Holding’s arrangement have not been publicly disclosed, the basic contours are clear: FFIN acts as a broker for Freedom Holding, primarily executing trades in popular U.S. exchange-listed equities and initial public offerings.

Peddling IPOs is Freedom Holding’s most aggressively promoted line of business, and FFIN handles the firm’s IPO-related customer service issues. For its part, FFIN has a distinctive business practice: requiring clients to observe a 93-day lockup period for any IPO shares they purchase. Customers cannot sell or even transfer to an outside account the newly purchased shares for that three month period.

This is starkly at odds with the typical U.S. and European brokerage practice, whereby clients are free to trade their shares immediately after receiving an allocation. Any other brokerage that tried to impose this constraint would likely be assured of an immediate customer exodus and a wave of litigation.

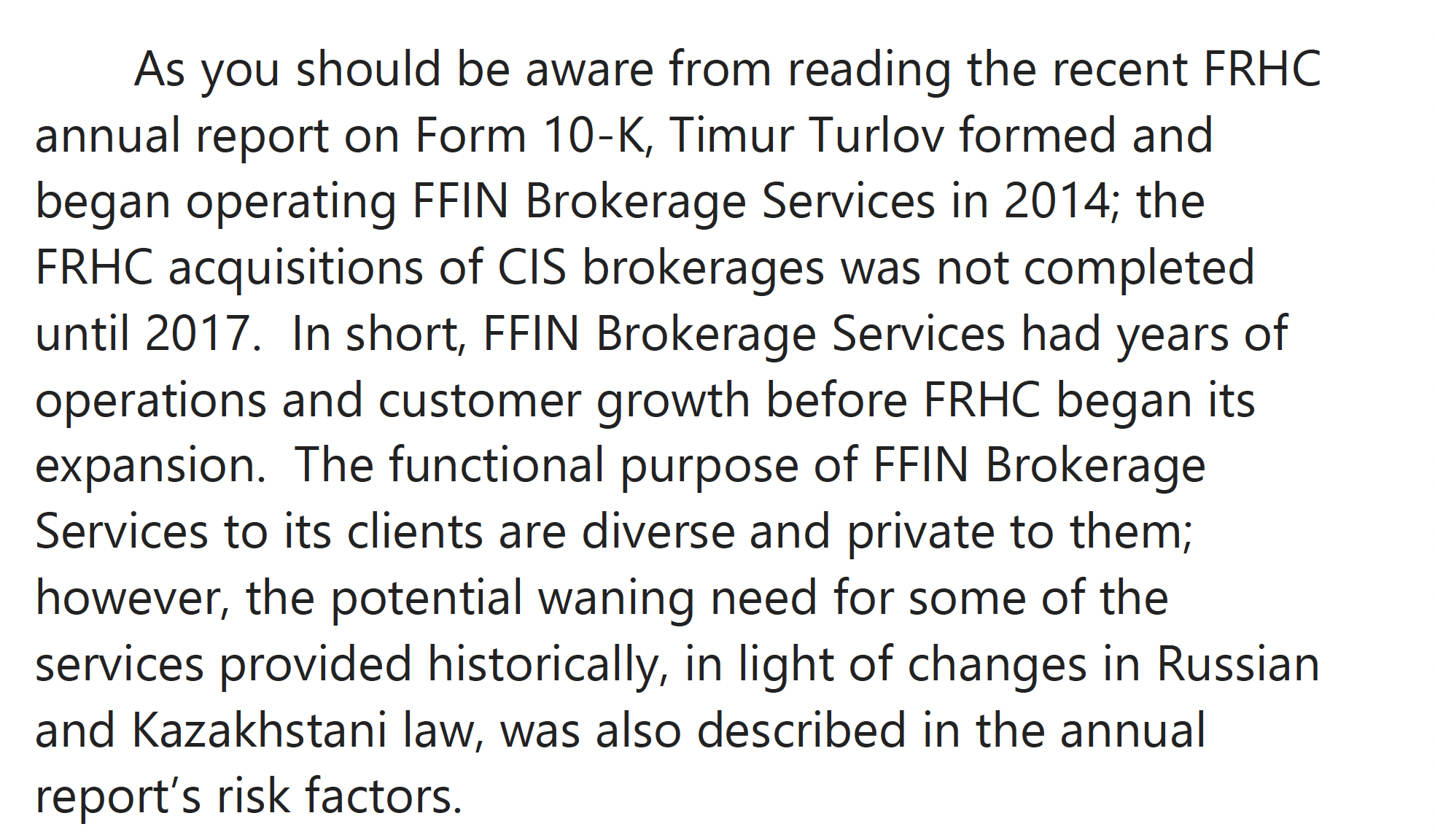

The Foundation for Financial Journalism asked Poulton several questions about the particulars of the Freedom Holding-FFIN relationship. (Poulton addressed one group of questions but refused to answer a second, more specific set.) He would speak only generally about FFIN, saying, “The functional purpose of FFIN Brokerage Services to its clients are diverse and private to them.”

Poulton also cited changes in Russian and Kazakh laws that might reduce Freedom Holding’s reliance on FFIN. Turlov set up FFIN in 2014 to offer Russian and Kazakh residents access to U.S. dollar-denominated investments, Poulton said. At the time, Russian regulators frowned on individuals owning British pound- and U.S. dollar-denominated investments. In 2018, however, the two countries started to ease such regulations.

The Foundation for Financial Journalism posed the same questions to Adam Cook, Freedom Holding’s corporate secretary; Askar Tashtitov, Freedom Holding’s president; and Turlov but did not receive a reply.

Generating huge profits via a small Cyprus unit

Notwithstanding the steady skyward march of Freedom Holding’s share price, its financial statements are surely catnip for short sellers and financial skeptics.

Embedded in the filings is the prominent role Freedom Holding’s Cyprus unit plays in the company’s growth. That subsidiary, which used to be the prime component of Freedom Finance Europe Limited, has been formally renamed Freedom Finance Europe Limited; the unit opened in 2017 and its main task is operating Freedom 24, an electronic trading system.

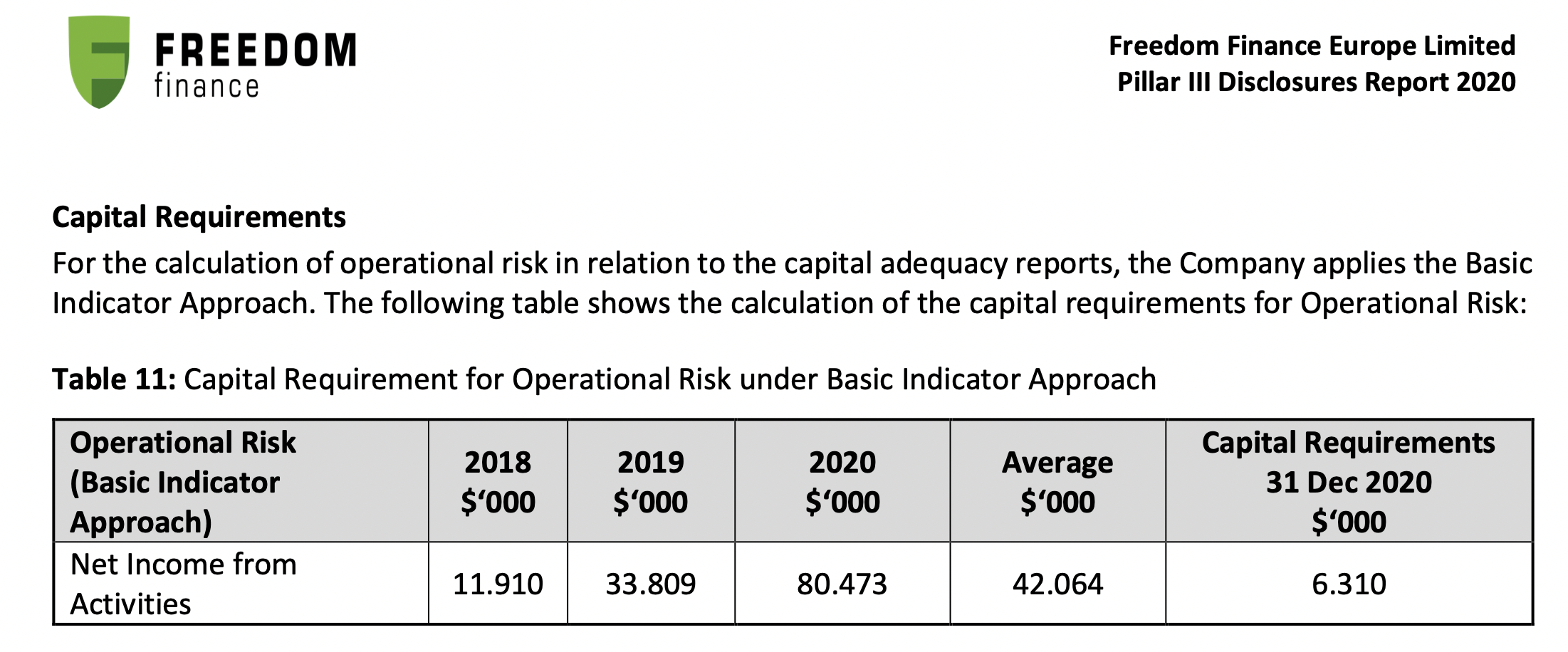

As described in the December article, the Cyprus subsidiary’s defining feature is achieving astronomical profit growth, unrivaled on Wall Street. Although in 2017 the Cyprus unit reported a $30,000 loss, by 2019 it had $33.8 million in earnings. In 2020, the subsidiary’s income rose to $80.4 million.

Freedom Holding’s earnings growth story is entirely a function of its Cyprus subsidiary. One way to track this is to compare the published financial results for both Freedom Holding and its Cyprus subsidiary from Jan. 1, 2020, through Dec. 31, 2020. (The Cyprus unit files a risk disclosure statement once a year that includes its annual net income, but corporate parent Freedom Holding releases its income quarterly and its fiscal year ends on March 31.)

For the nine months that ended Dec. 31, 2020, Freedom Holding reported $90.1 million in net income, with $80.4 million of this derived from the Cyprus subsidiary.

Thus, for nine months of Freedom Holding’s most recent fiscal year, the Cyprus unit contributed at least 56 percent of the parent company’s $142.9 million in net income.

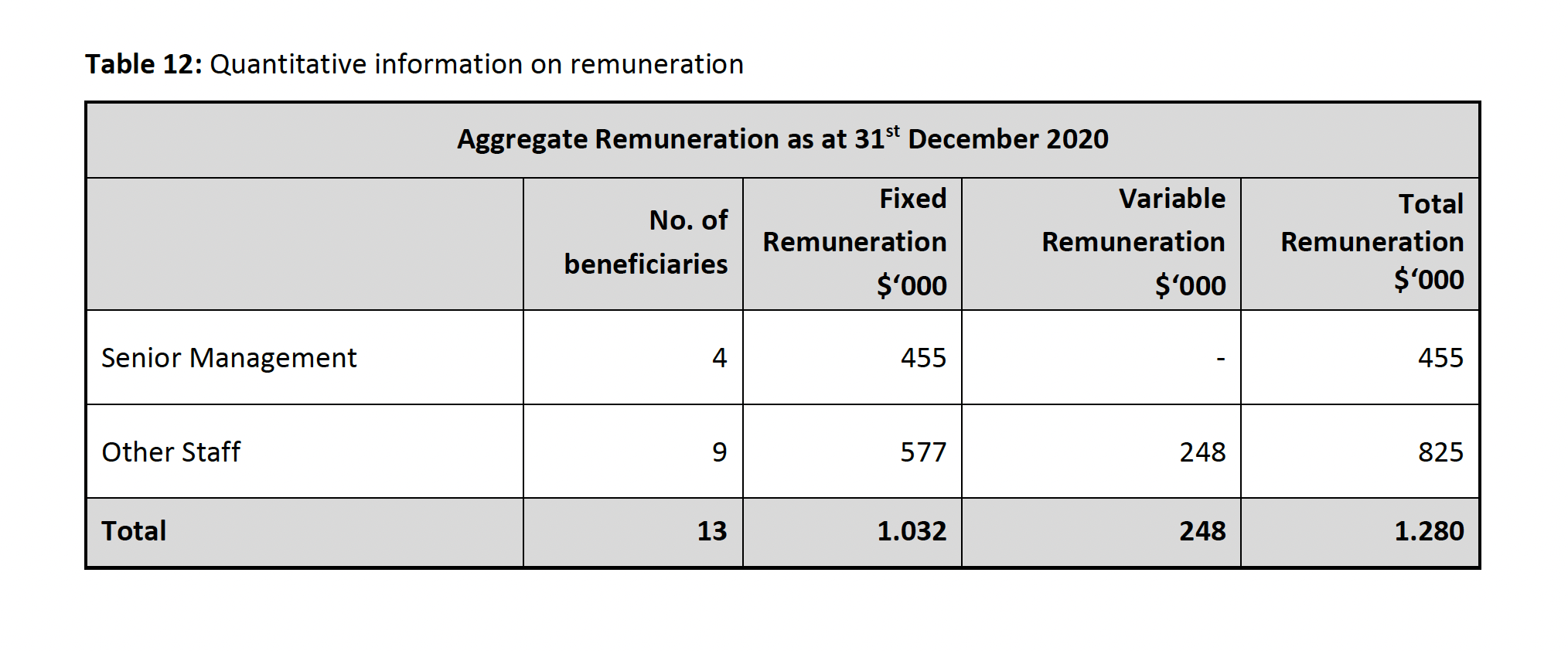

And according to a recent regulatory filing, the Cyprus subsidiary achieved those results with minimal resources. Making that sum of money took only 13 employees and $6.3 million in capital.

Taken at face value, the Cyprus unit’s gaudy performance likely catapults it to the top of the list of the most profitable trading desks in history. (The distant second: Michael Milken’s high-yield trading operation at Drexel Burnham Lambert, which in 1987 generated a purported $2 billion in revenue, with Milken pocketing an estimated $550 million.)

To an outside observer, the fact that the Cyprus unit could generate profits at this scale is baffling. After all, it is a no-frills online trading operation that facilitates individual investors’ stock trades. It definitely is not an elite proprietary trading division; compensation for its 13 employees last year totaled less than $1.3 million.

Carrying out trades in a circuitous fashion

Freedom Holding employs a remarkably circuitous order execution process for its customer’s trades. It is labyrinth to a degree that suggests that obtaining the best possible price for the client is a secondary concern.

A transaction might look something like this, according to conversations with current and former Freedom Holding clients, as well as a former company executive: A client of Freedom Holding who attempts to buy shares onlineis promptly directed outside its platform to FFIN, which then routes the order to Freedom Finance Europe in Cyprus. But final execution of the client’s order appears to require another handoff, either to a Freedom Holding subsidiary in Moscow or (frequently) to a firm with a troubling regulatory history, Lek Securities U.K. Limited in London.

One possible reason for this complexity? Fee layering, the practice of charging a client multiple fees on a single transaction.

Layering is a legal, albeit controversial, practice that has fallen out of favor in the U.S. money management industry, given the rise of lower-cost index and exchange-traded fund investing. But for Turlov and his colleagues, elongating a trade’s life cycle in order to collect two or three sets of fees might be tempting since their largely Russian and Kazakh client base might have scant experience with Wall Street practices or robust consumer advocacy.

A further puzzle: The Cyprus unit’s 2020 risk disclosure statement noted that last year FFIN executed 24 percent of the trades made by the unit, up from 9 percent in 2019. This is odd since neither FFIN nor the Cyprus subsidiary hold any U.S. brokerage licenses.

Doing business with companies of questionable repute

One of the nicer things about managing an expanding and profitable company is having options. For example, if a customer poses a reputation risk or is too demanding relative to his or her economic value, ending the relationship is generally a low-risk proposition.

Timur Turlov and his managers do not seem to hold this view, however, because they have regularly done business with people and companies whose extensive legal problems would cause most U.S.-based managers to stop in their tracks.

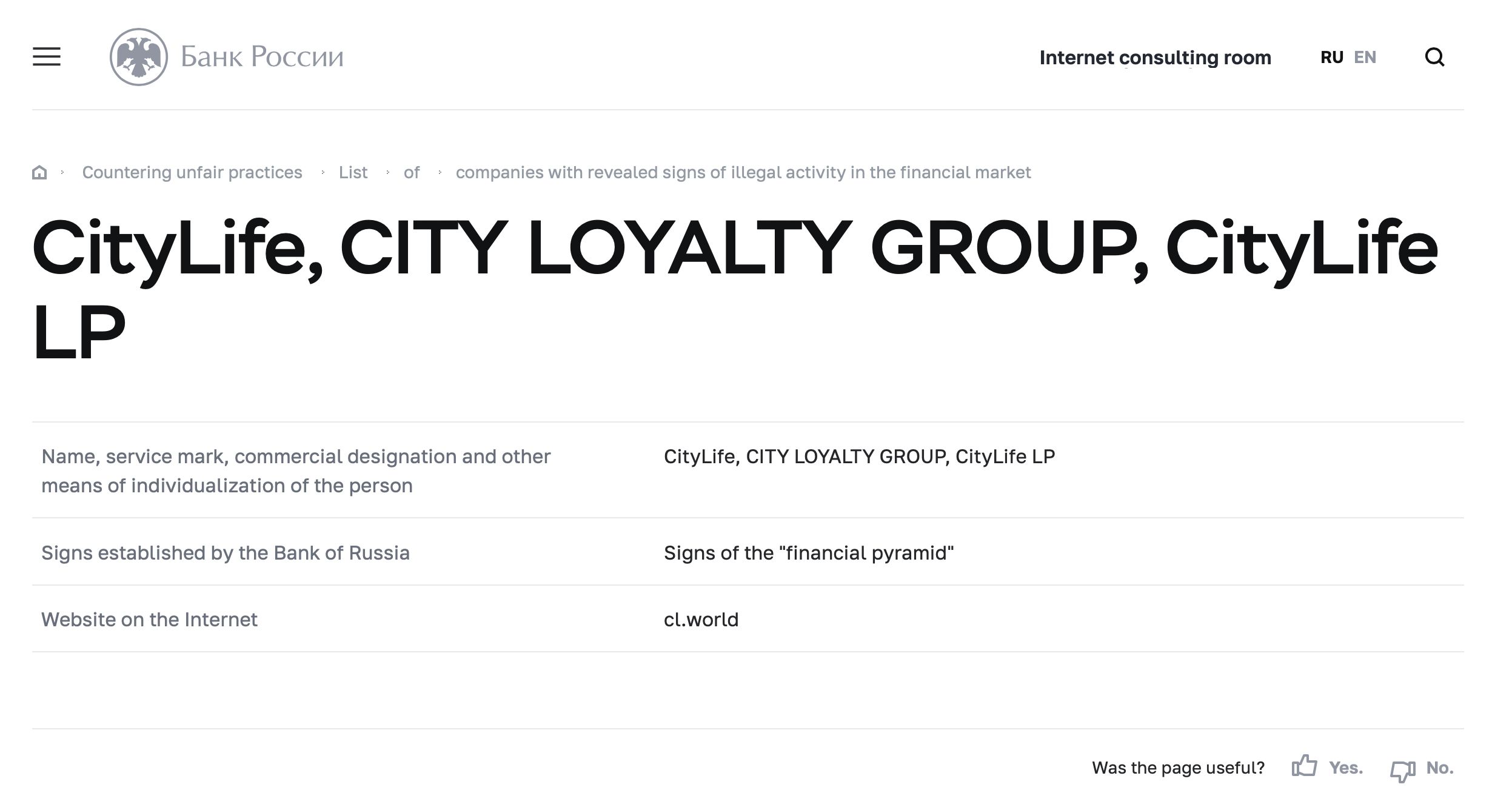

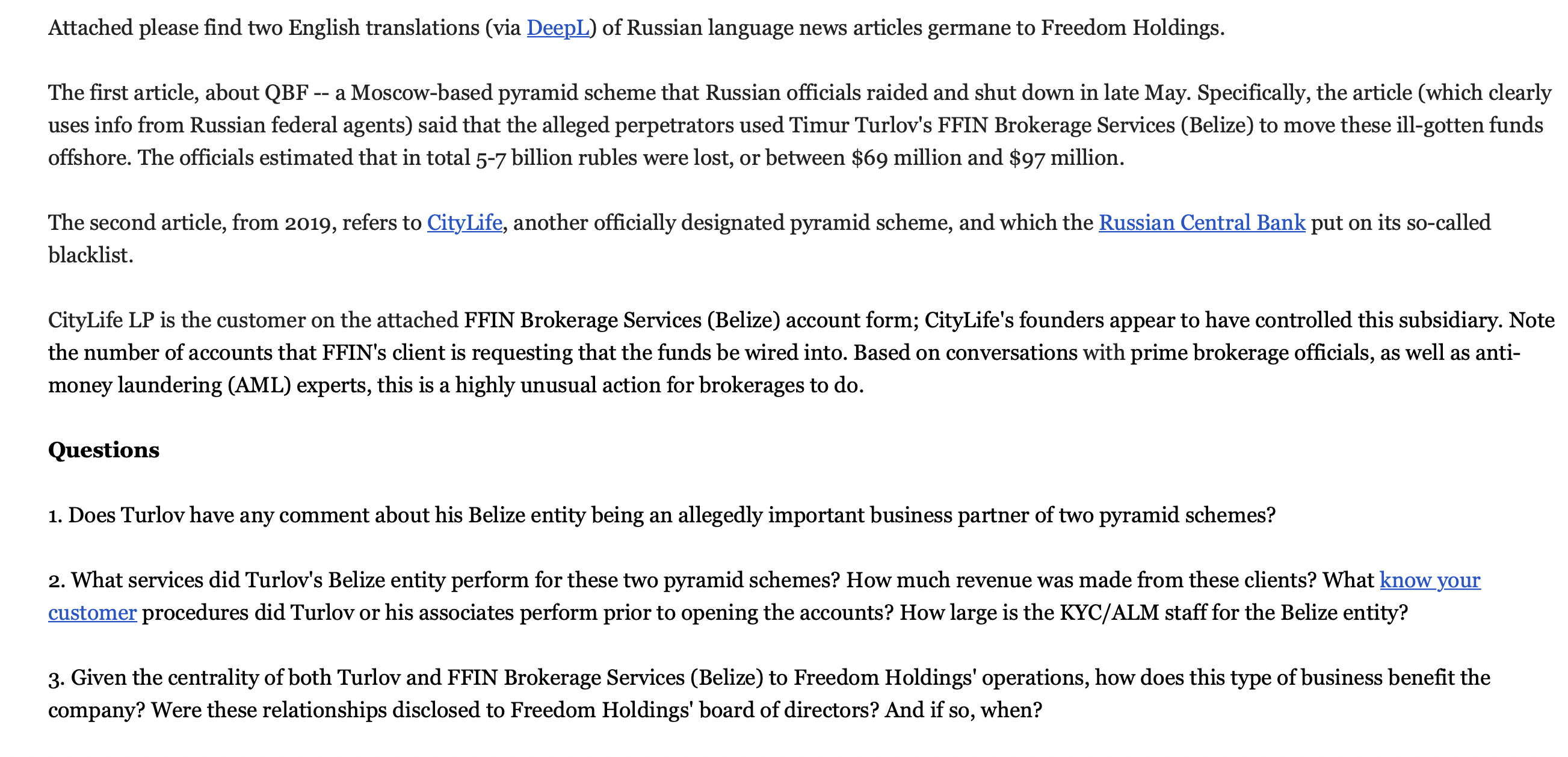

Consider FFIN’s business relationship with two Moscow-based companies: asset manager QBF LLC and network marketer CityLife.

Both QBF and CityLife have attracted the scrutiny of the Russian government: The Ministry of Internal Affairs raided QBF on May 31 and arrested two of its principals for purportedly conducting a Ponzi scheme. And on June 1, the Central Bank of Russia’s Unfair Trade Practices unit added CityLife to a list of companies with identified signs of illegal activity for allegedly showing signs of running a pyramid scheme.

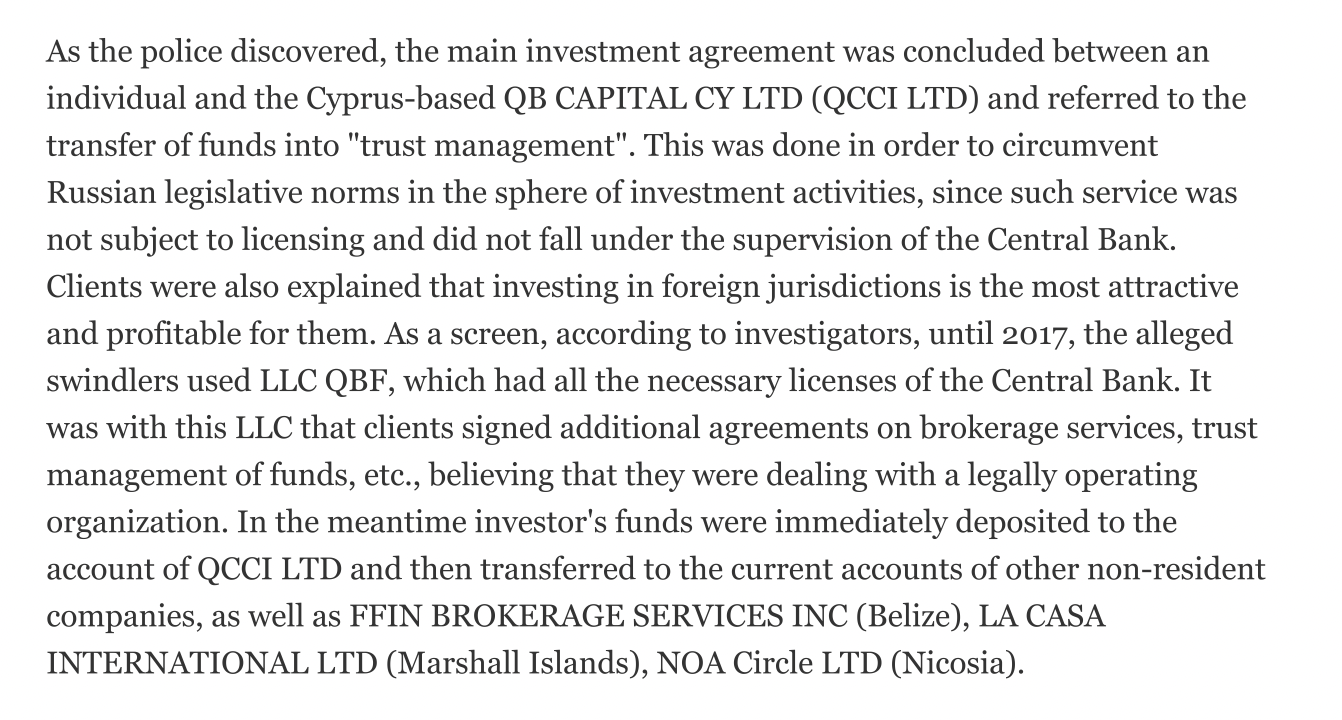

How does FFIN fit into all this? According to a translation of a Russian language press account of the Interior Ministry’s QBF raid, FFIN was one of several banks and brokerages the asset manager’s executives were said to have used to move investor cash out of Russia. (Neither Turlov nor Freedom Holding were named in the article.)

While using a Russian language search engine, the Foundation for Financial Journalism found a CityLife co-founder’s FFIN wire instructions designating 16 separate bank accounts that were to receive funds. It is not clear who posted such a sensitive document online, but the root link is from a CityLife website. One of the banks listed on the form is Freedom Holding’s Bank Freedom Finance LLC.

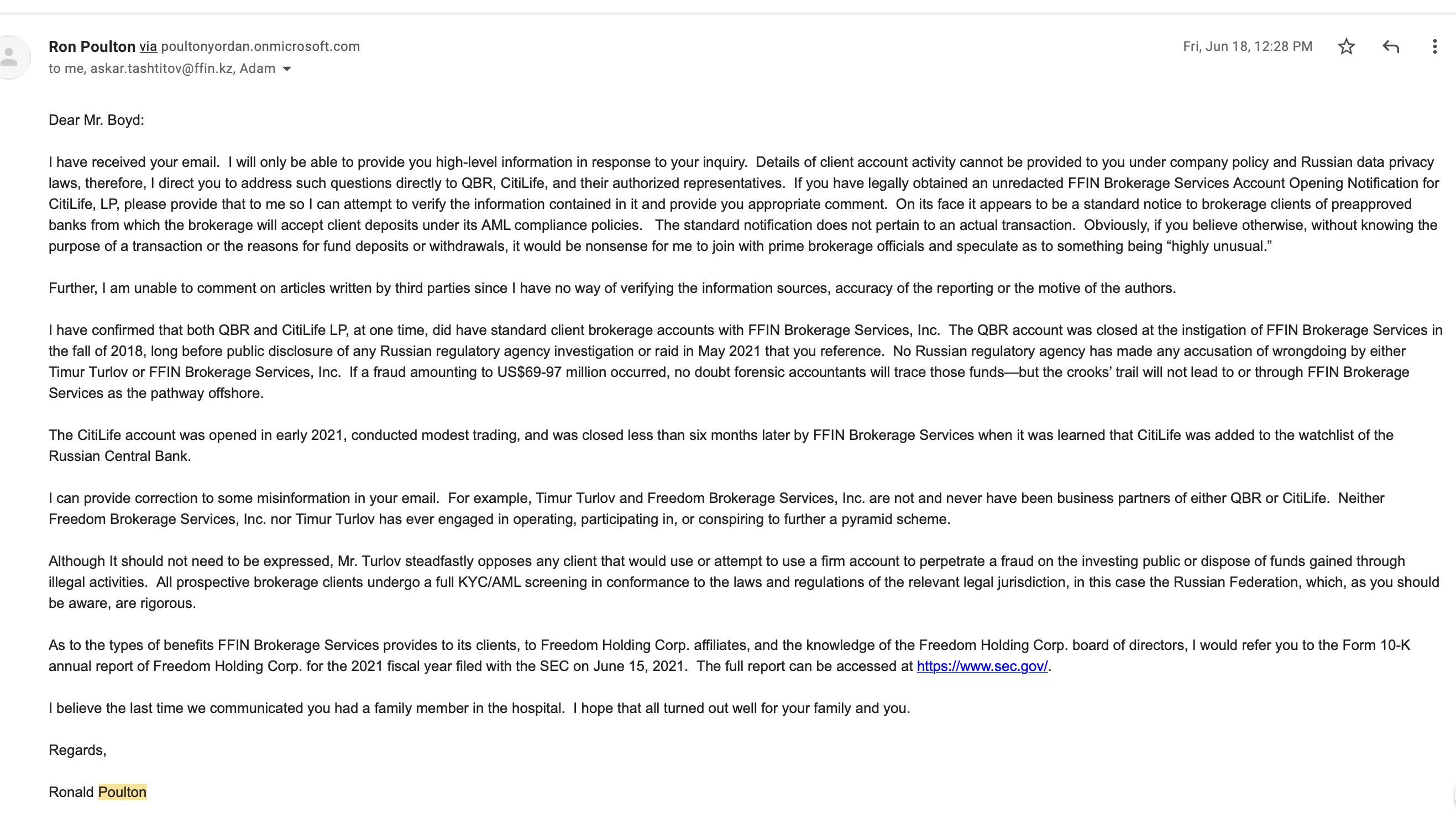

Questioned about FFIN’s relationship with QBF and CityLife, Poulton confirmed that the two firms “at one time did have standard client brokerage accounts with FFIN Brokerage Services.” He said that FFIN closed the QBF account “in the fall of 2018” but did not provide a reason.

Poulton added that the CityLife account was opened in early 2021 and “conducted modest trading” and when the Central Bank of Russia added it to its list of companies with identified signs of illegal activity, FFIN closed the account.

Update: This story was updated on Aug. 8, 2021, to clarify the relationship of the Cyprus unit to Freedom Holding’s Freedom Finance Europe; it used to be referred to as its subsidiary but now is simply called Freedom Finance Europe.

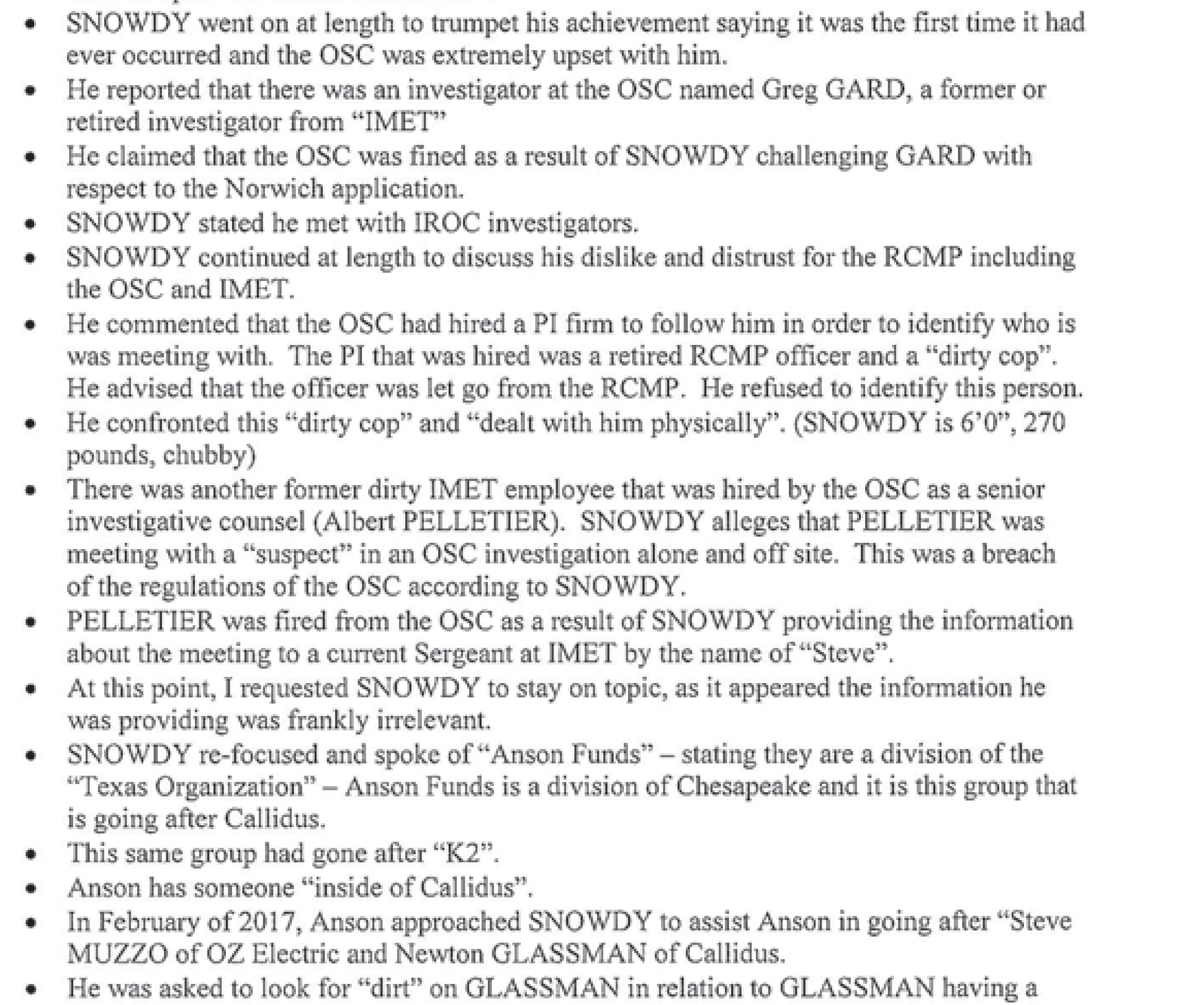

Derrick Snowdy is probably as close to a celebrity as Canada’s private investigator community has.

Starting in 2010, Snowdy burst into view as a prime mover in the political controversy colloquially known as “the busty hookers’ scandal.”

Snowdy proved to be a quick study at capturing an audience’s attention, ever ready to regale listeners with some of the inside stories from his investigations.

So when Catalyst Capital founder Newton Glassman brought a stemwinder of a defamation litigation in 2017 against a host of hedge fund managers and journalists, it was not surprising to see Snowdy involved.

(Foundation for Financial Journalism readers will recall our two 2018 investigations that looked into the quality of disclosures at Callidus Capital and Catalyst Capital, the two investment vehicles Glassman controlled. In July 2019 Catalyst amended the initial defamation claim to add Bruce Livesey, the article’s co-author, as a defendant.)

After all, given the numerous well-heeled defendants — and their lawyers, many sporting big litigation budgets — the prospects for an investigator with a knack for digging into corporate fraud seemed attractive.

There was just one thing.

A series of filings were unsealed late last week in Catalyst’s litigation revealed that Snowdy had indeed been hard at work on these types of issues for several years. (The filings were made by West Face Capital and the other defendants.)

But it had been for the other side.

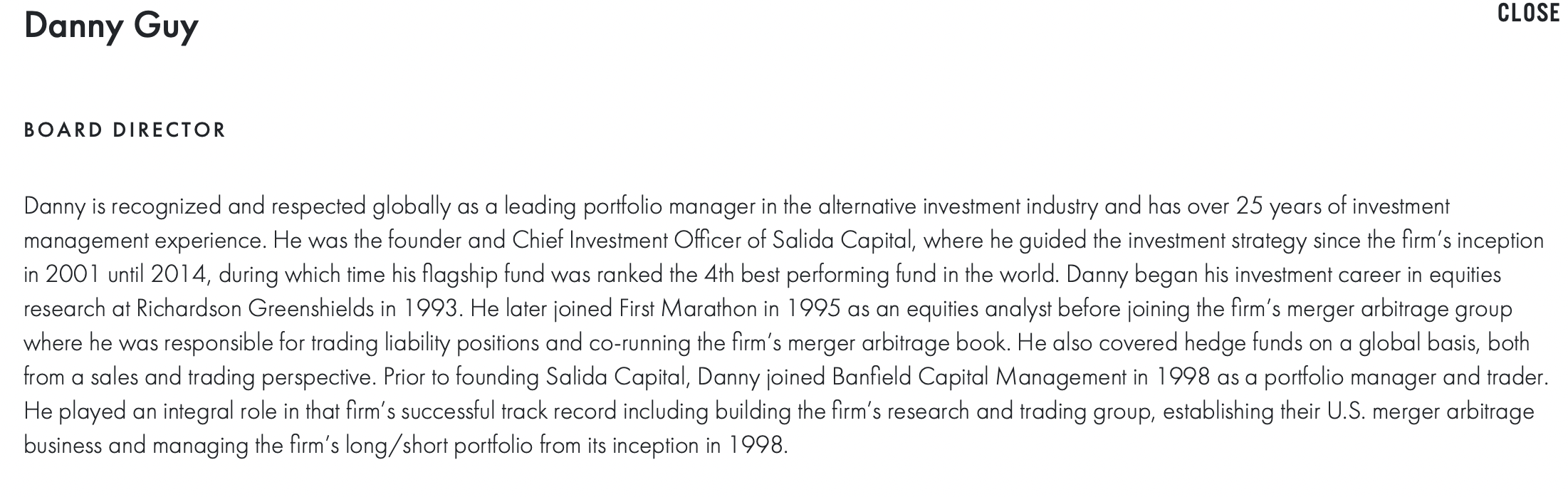

So who bankrolled Snowdy’s efforts? A single client: Danny Guy, a veteran Canadian money manager and the general partner of Harrington Global Opportunities Fund.

Meet Danny Guy

Little about the arc of Daniel Gerrison Guy’s career in finance would imply a disposition towards garish conspiracy theories.

After starting in brokerage research in 1993, Guy joined Banfield Investment Management, a then prominent Toronto risk arbitrage fund in the late 1990’s. In 2001, Guy led a buyout of the fund and renamed it Salida Capital. Becoming Salida’s chief investment officer, Guy changed the fund’s investment strategy to a more directional, commodities oriented focus with a heavy emphasis on private equity.

(Salida is Spanish for “exit,” a commonly used term in private equity that means an investment was successfully concluded via a fund either selling an asset at a higher price or to the public through an initial public offering.)

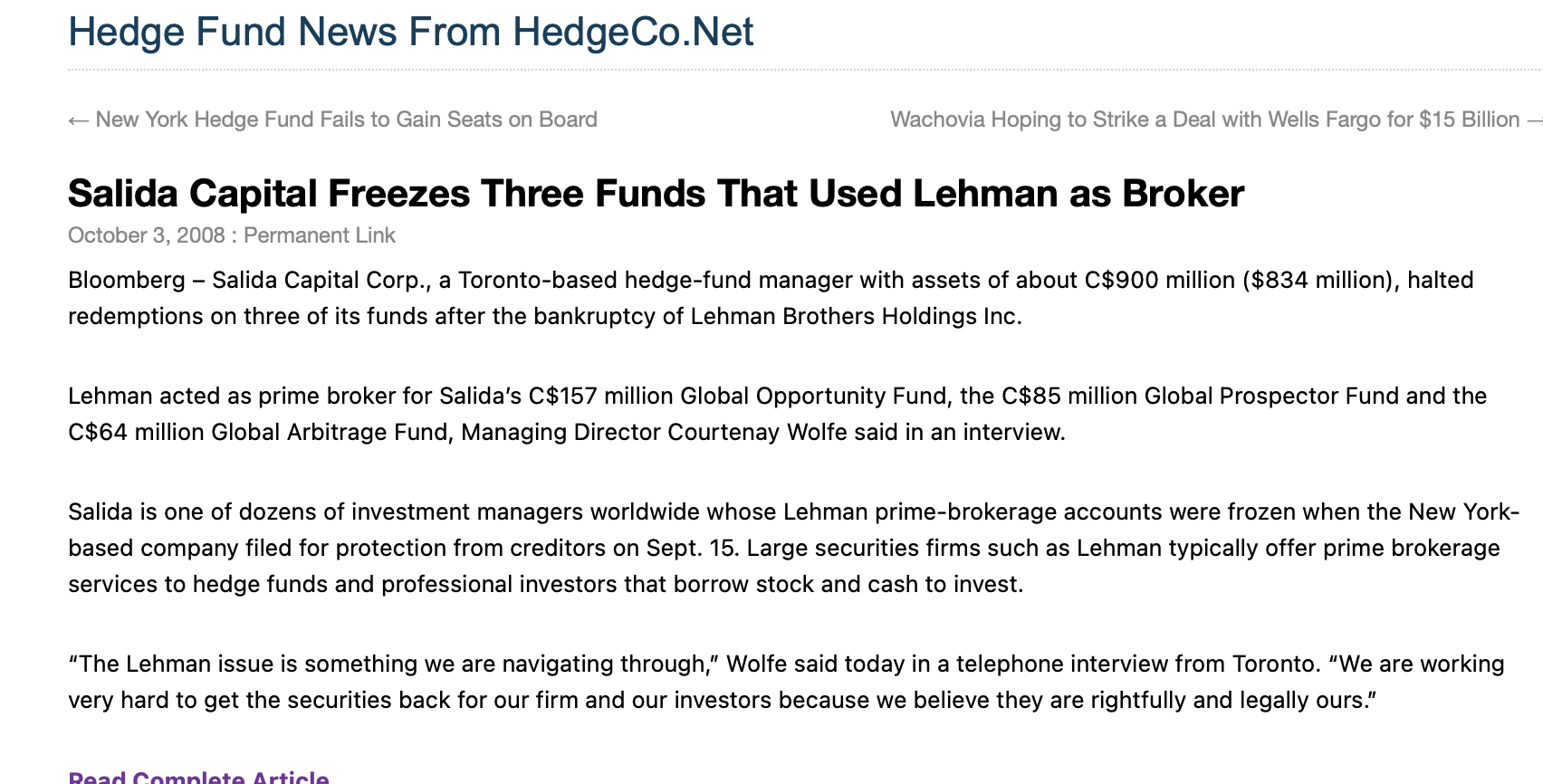

From 2002 through 2007, Salida posted very handsome returns, but in 2008, the one-two punch of the global financial crisis and the collapse of Lehman Brothers, the fund’s prime broker, led to disastrous losses. Though Salida’s performance in 2009 and 2010 was stellar, restoring the fund’s assets under management proved much more difficult, and in 2013 it began to shutter its portfolios.

In 2011 Guy moved to Bermuda, but it is unclear when the Luxembourg-domiciled Harrington Global was formally launched, or if it has limited partners. The fund does not appear to report to hedge fund industry databases.

Snowdy told the Foundation for Financial Journalism that his connection with Guy began when Salida Capital’s then CFO asked him to perform some due diligence on an investment Salida had made that the fund was concerned about.

“It was to look at a company called StarClub. I did some work and determined it was pretty much a fraud,” he said. (StarClub’s product was a software application that purported to help so-called social media influencers track the reach and impact of their endorsements.)

Snowdy continued that he delivered a report and forgot about it until November 2016 when Salida’s CFO called him and said, ” ‘It looks like you were really right on [StarClub] and asked me if I could I help them build a case for a lawsuit.’ ”

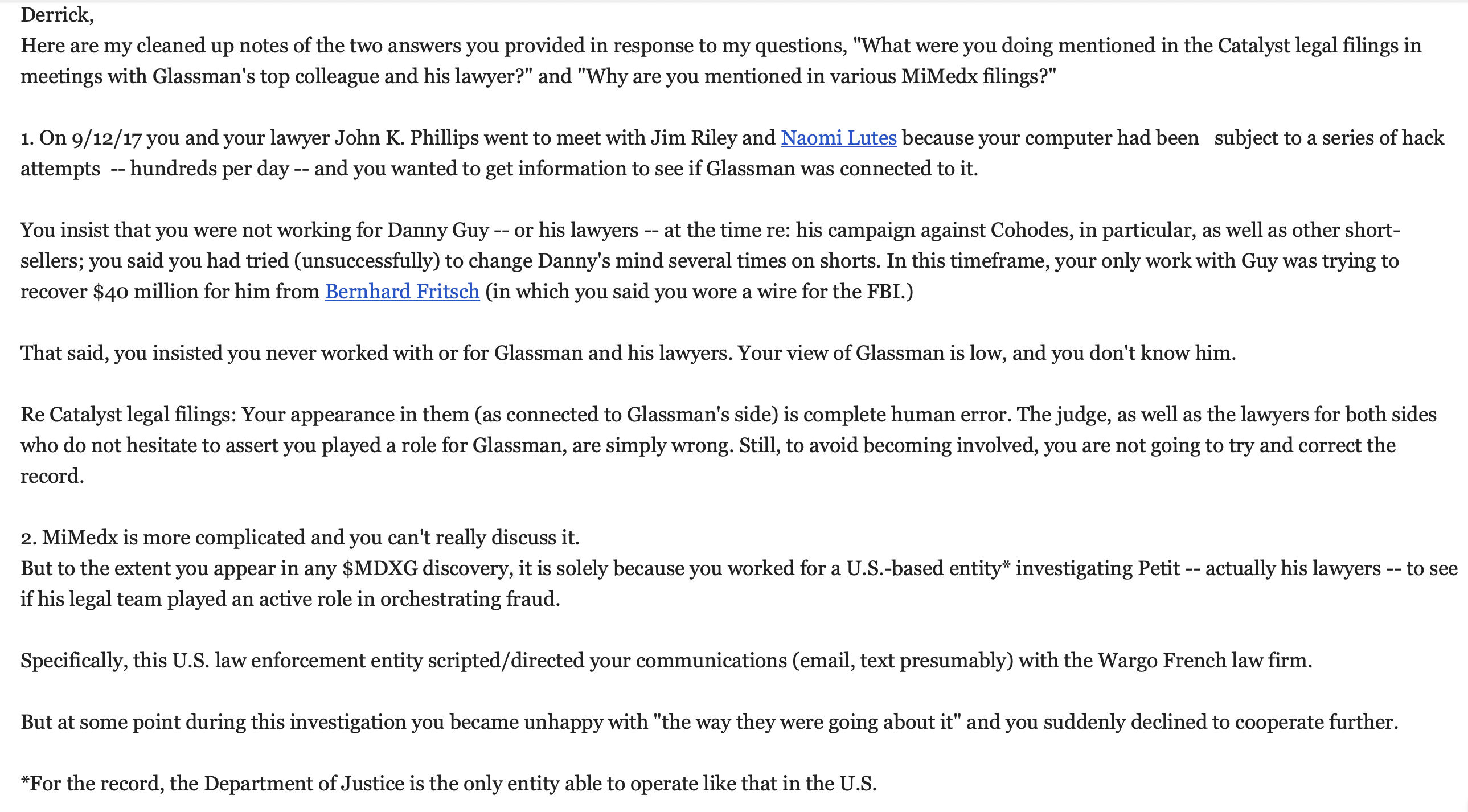

Snowdy said in the course of investigating StarClub in 2016 he wore a hidden recording device while posing as a potential investor during a meeting at Goldman Sachs’ headquarters, and he identified and obtained photos of a yacht that StarClub’s founder Bernhard Fritsch allegedly owned. The FBI knew about and approved everything he did, Snowdy said.

In August 2017 federal prosecutors in Los Angeles unsealed an indictment that charged Fritsch with a series of fraud-related counts. The case is scheduled to go to trial in January 2022.

According to the indictment, Guy invested more than $22.4 million of Salida and Harrington Global’s capital in StarClub.

The road to vengeance

Guy’s experience with a pharmaceutical concern called Concordia Healthcare is why he became consumed by the idea of exposing how short sellers operate.

Concordia was a once high-flying company in which Harrington Global had a 2.7 million share stake, at one point amounting to over 5.2 percent of its shares outstanding.

Concordia’s business model was similar to that of Valeant Pharmaceuticals International, in that it used aggressive borrowing to fund purchases of established drugs. The goal was to simultaneously raise drug prices while avoiding costly (and recurring) research and development expenses.

It was a model that worked for a little while.

Unfortunately for both Concordia and Guy, when presidential candidate Hillary Clinton sent out a 21 word tweet on September 21, 2015, everything changed.

Clinton’s retweet of a New York Times article about a series of astronomical price hikes in a drug called Daraprim brought the issue of drug prices front and center in the 2016 presidential race.

And much of that ensuing dialogue centered on how constant drug price increases were forcing brutal sacrifices and trade-offs for many American families.

A month later Valeant Pharmaceuticals came in for its own reckoning: On October 15 the Foundation for Financial Journalism exposed how the company’s Philidor subsidiary helped it keep certain drug prices artificially high, as well as evade pharmacy ownership regulations.

Concordia, with about $4 billion in debt and reliant on acquisitions to fund the revenue growth investors were demanding, was suddenly hamstrung in its ability to boost prices.

With a business model whose future had suddenly become an open question, Concordia’s share price soon began to slide. Moreover, it attracted numerous short sellers, including Marc Cohodes, an ex-hedge fund manager who uses his twitter account to offer unfiltered, often profane takes on companies he is short.

Starting in October 2015 Cohodes began building a short position in Concordia’s shares. In June 2016 company CEO Mark Thompson sued Cohodes for defamation; Cohodes happily fired back with lengthy letters to U.S. and Canadian regulators in July and August enumerating several ways he thought the company was misleading investors.

In August, six weeks after suing Cohodes, Thompson was subject to a humiliating margin call, and two months later he quietly resigned. He withdrew his suit against Cohodes soon after.

Cohodes, asked for comment about Concordia, said he was happy to have shorted it, “in the $70 range,” but declined to elaborate more on the experience, beyond noting tersely, “[Concordia] was a piece of shit.”

(A word of disclosure: In 2017 Cohodes made a donation of $344,593.20 to the Foundation for Financial Journalism. He is discussed further below.)

Guy approached Canadian securities regulators in 2016 to allege that short sellers were depressing Concordia’s share price through illegal trading tactics such as “spoofing” in order to trigger a wave of algorithmic selling. No regulatory action was taken.

Concordia sought protection from creditors in October 2017, and Harrington Global liquidated its Concordia position at an approximately $150 million loss. (After reorganization, the company is now known as Advanz Pharma Corp.)

Sustaining such brutal losses galvanized Guy’s thinking about Concordia’s demise: A cabal of short sellers spread disinformation about the company’s prospects while using illegal trading tactics to pressure its share price.

Central to proving this claim, Guy felt, was obtaining the identities of those responsible for perpetrating the “short-and-distort” campaign on Concordia. His attempts to get the information through hearings with regulators failed because of concerns over privacy.

To that end, Harrington Global petitioned for a Norwich Order — a motion delivered on a third-party in possession of material information — that would have compelled Canada’s brokerage regulator, the Investment Regulatory Organization of Canada, to disclose those names.

But Harrington Global’s request was denied in a 2018 Ontario Superior Court ruling.

In January Harrington Global sued a series of U.S. and Canadian banks in the U.S. District Court for the Southern District of New York. The claim primarily alleges that traders at large banks used illegal tactics that served to manipulate Concordia’s price downward.

Asked about Guy’s views on Concordia’s collapse, Snowdy assessment was blunt.

“I told Danny that [Concordia CEO] Mark Thompson was a lying sack of shit,” Snowdy said.

But, Snowdy continued, “Danny defended Mark Thompson. And then [Guy] would start screaming about naked short sales, Marc Cohodes’ role in all this, and that crap. I told him that [Cohodes] was right about Concordia.”

In a long, rambling letter to West Face’s lawyers in which Snowdy discusses his role in the Catalyst case, he said that his take on Concordia’s collapse antagonized Guy a great deal. On one occasion, when Snowdy was vacationing with his kids in the Bahamas, Guy accused him of being there to only to make secret financial arrangements — the implication being that Snowdy would only have said that because short sellers paid him off.

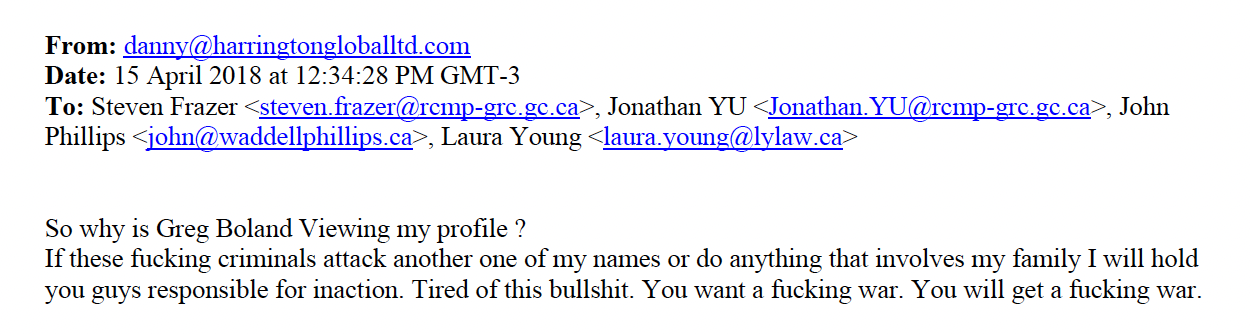

This darker turn in Guy’s worldview was on display in an April 2018 email to the Ontario Securities Commission. After Guy saw that Greg Boland, West Face Capital’s general partner, looked at his LinkedIn profile, Guy wrote an a threatening email to several OSC attorneys that promised “a fucking war” if short sellers targeted other companies he was invested in, or if anything happened to his family.

[Guy was not the only one being paranoid. In a phone interview, Snowdy related how in 2018, en route to a meeting with Nate Anderson — also a defendant in the Catalyst case — he detected two people following him. This led him to believe that perhaps Anderson’s office had been somehow compromised. Anderson said that in that period his office was at a WeWork, and he didn’t think that being infiltrated by private investigators was a very big risk.]

The Foundation for Financial Journalism repeatedly sought to interview Guy. His conditions — fly to Bermuda and interview him — proved unworkable. In a response to a text message about his opposition to short selling, Guy said, “I have no problem with shorting when it’s done right.”

Penetrating the wolfpack

There was nothing terribly complex about what Snowdy did.

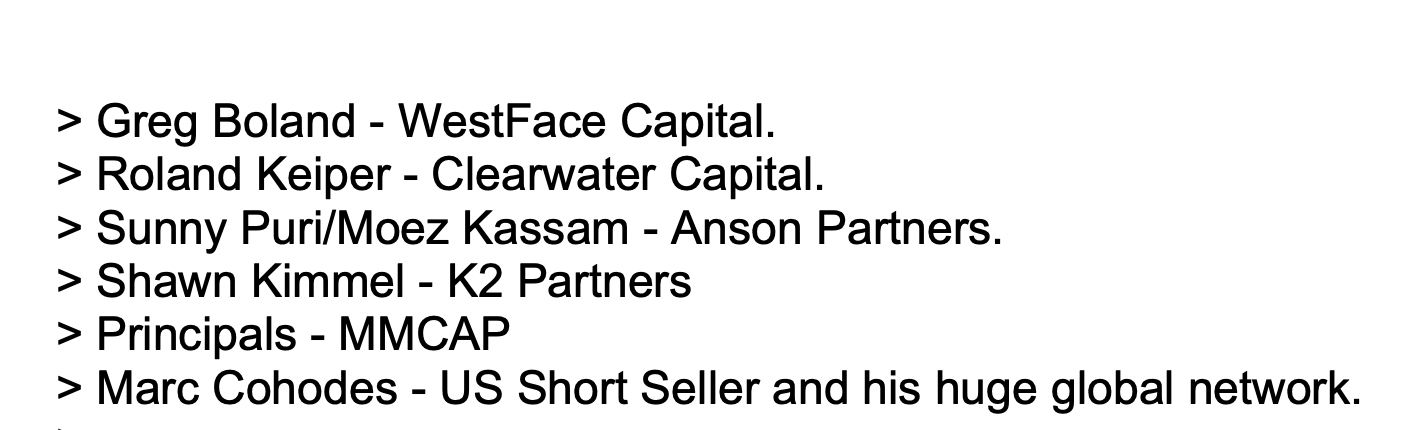

Starting in 2017, Snowdy began posing as a sympathetic, knowledgeable fraud-fighting ally to many of the reporters and short sellers named in the Catalyst claim. More importantly, Snowdy leveraged this nascent rapport to obtain introductions to other investors and forensic analysts who were researching and shorting publicly traded companies.

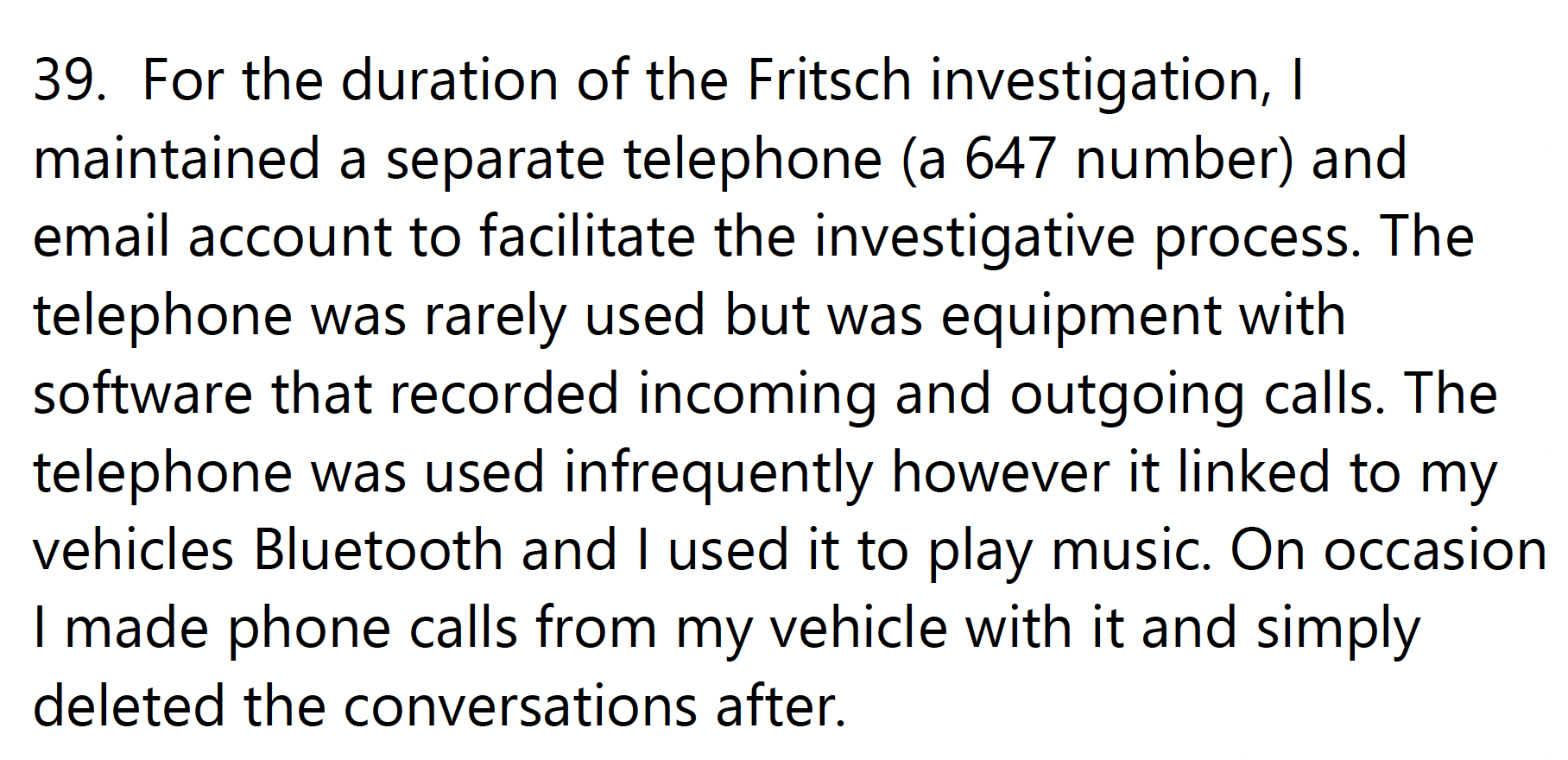

A big part of Snowdy’s operating methodology was taping phone calls, according to emails he sent; one of his two phone numbers was set to automatically record and was stored on his home computer. That may pose a prospectively large legal headache for him since he described recording California resident Marc Cohodes, and the state’s laws require both parties to consent to having a call recorded. (Cohodes strongly denied having given his consent for recording.)

The unsealed documents, however, do not specify what information he got from taping Cohodes. When asked about taping Cohodes and the absence of his consent, Snowdy did not reply.

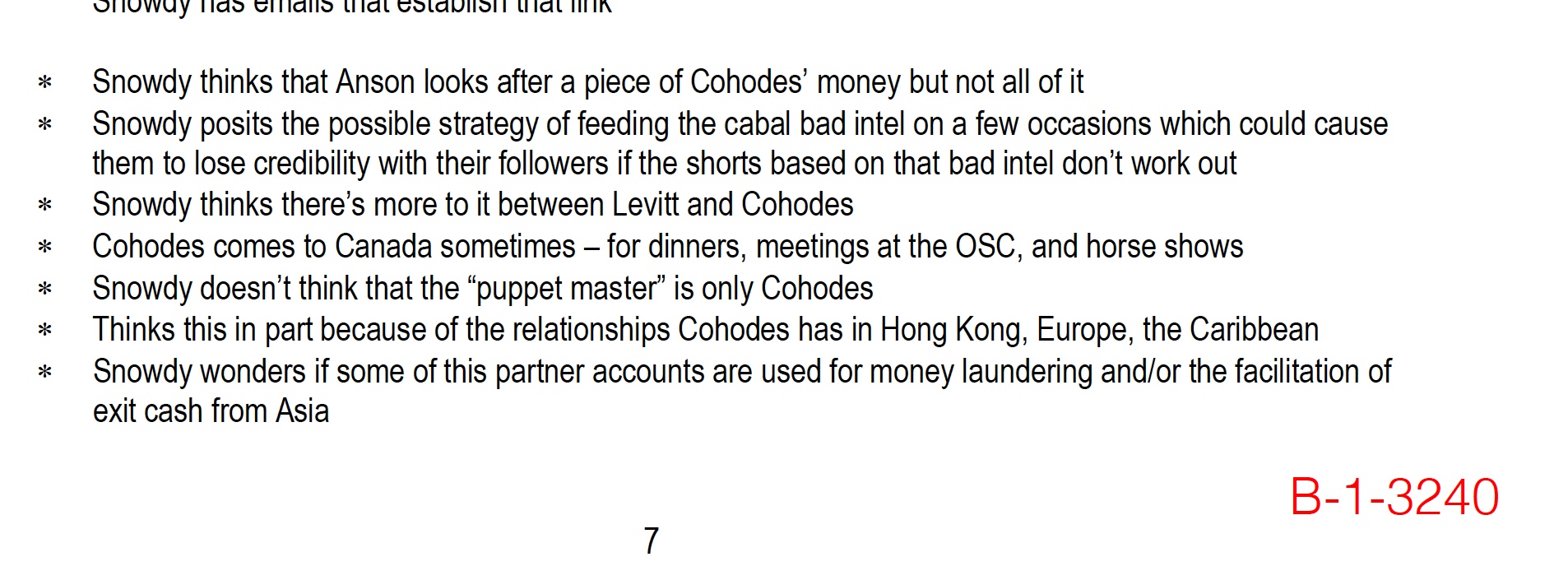

In a recently unsealed, multi-month WhatsApp message exchange between Guy and Glassman, Guy called this strategy “penetrating the wolfpack.” This echoes the theme Guy began enunciating with his angry email to the OSC: Short sellers are dangerous people.

Simultaneously, Snowdy was providing what he overheard — the gossip, the sources, targets and methods – to a small group of corporate executives who felt short sellers were unfairly (or illegally) attacking their companies.

The pay for doing these infiltrations was at least decent.

What Snowdy told people he uncovered, according to the court filings, looks very much like a version of a common short selling conspiracy trope. It usually follows along these lines: A loose network of short sellers — taking their cue from one individual leader — manipulate the press with misleading information, and then game the greedy or incompetent prime brokerage units at investment banks to allow them to flood the market with improperly borrowed stock. The result is a rapidly sinking share price for any company targeted.

Elements of this idea have been around for decades, but it was not until former Overstock.com CEO Patrick Byrne, during a 2005 presentation he called “The Miscreant’s Ball,” that these disparate complaints about reportorial malfeasance and short selling perfidy were housed in a unified theory.

Byrne claimed a Sith Lord — later revealed to be former Drexel Burnham Lambert executive Michael Milken — was then orchestrating (somehow) much of the dubious short selling activity to his benefit. He also argued that a large group of business journalists were merely transcriptionists for short sellers, and that the miscreants preferred to wage their campaigns in groups.

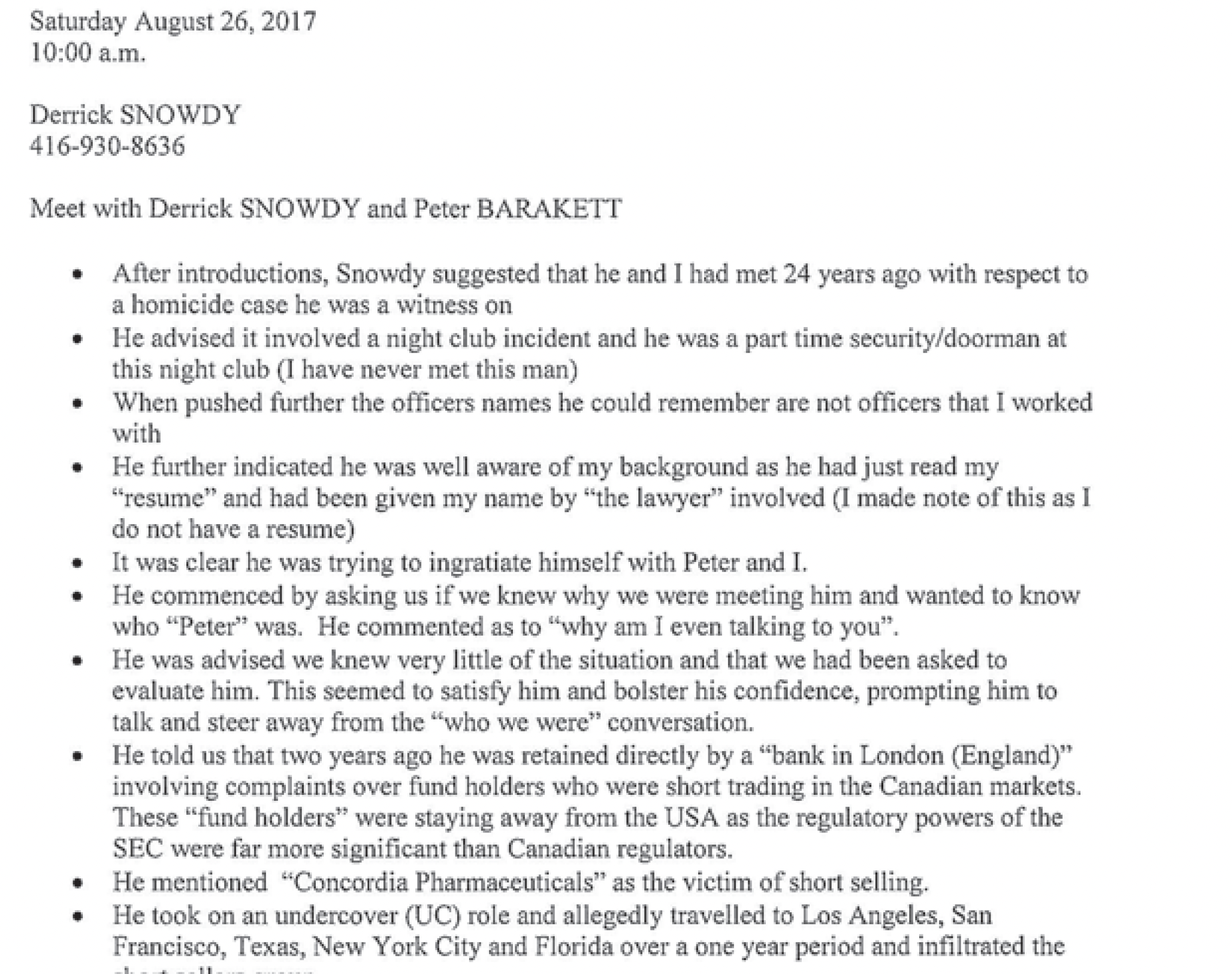

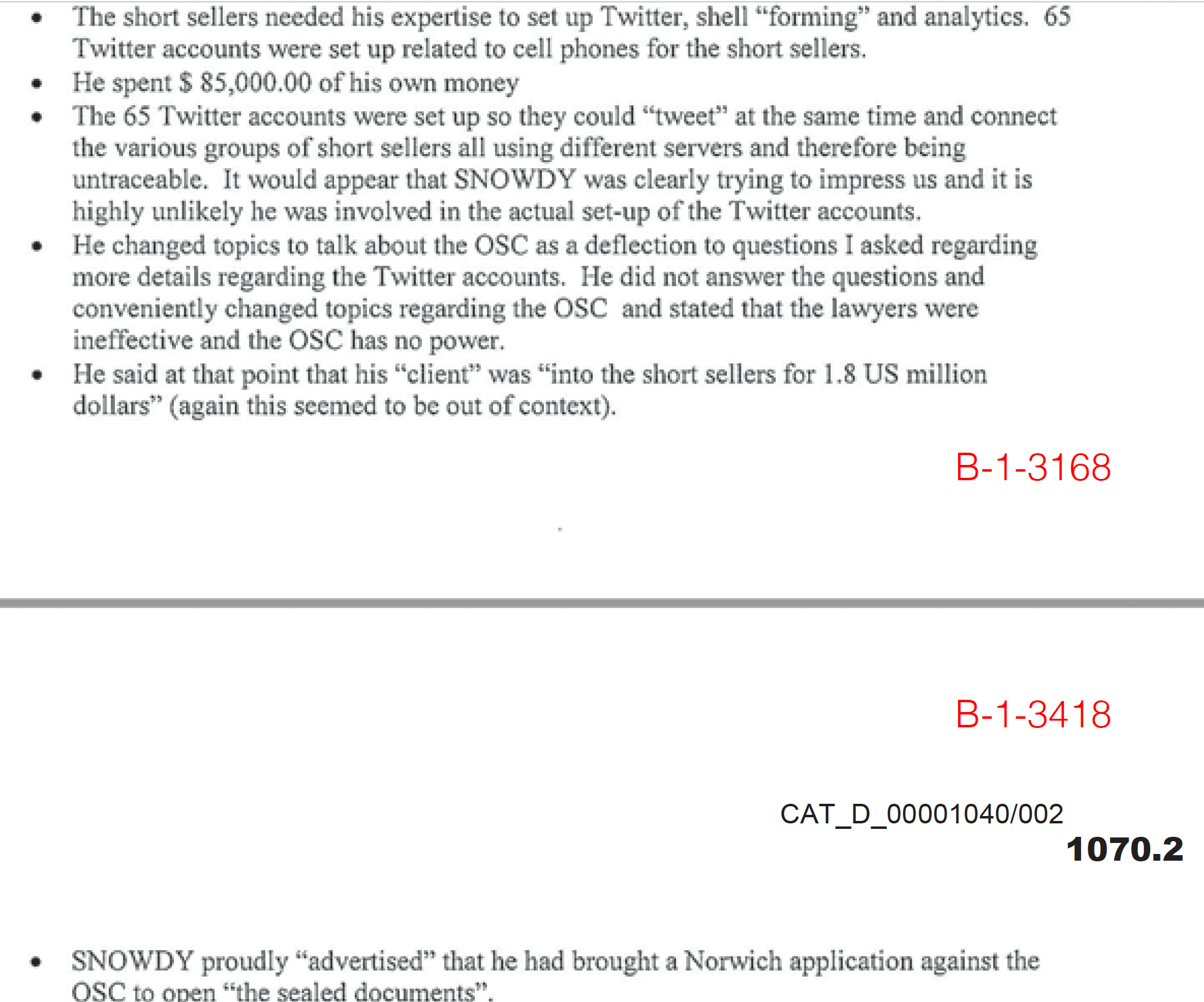

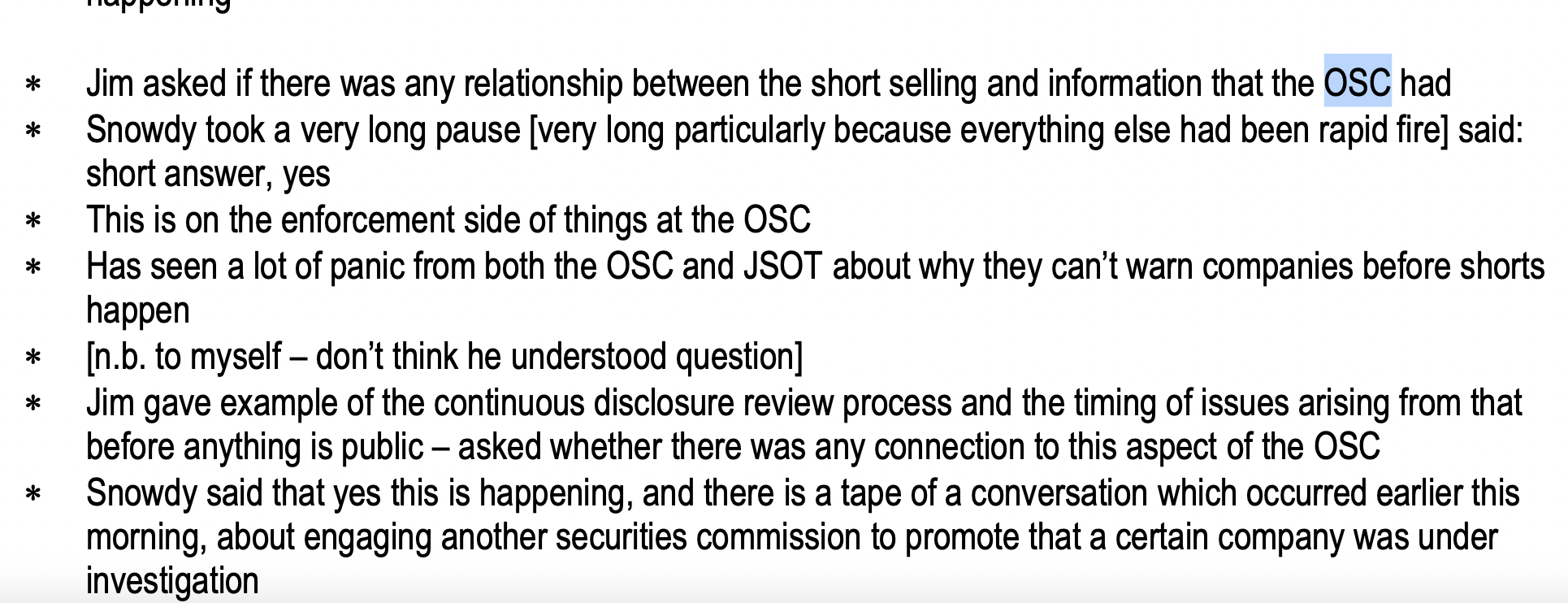

Snowdy, during a September 2017 meeting where he presented his findings to Jim Riley, former Catalyst COO and general counsel and others, leveled allegations that seemed to check many of the same boxes Byrne had complained about.

There are “puppet masters” that control the network and their connections to shadowy foreign capital, as well as a slew of seemingly nefarious linkages between everyone he named. And for good measure, Snowdy touched upon regulatory capture, a favorite theory of Byrne’s, when he appeared to suggest short sellers had somehow neutralized the Ontario Securities Commission.

For his part, Guy seems to agree with Deep Capture.

Guy sent Glassman a link, and told him that the article will “make your head spin.” (Snowdy, speaking about Guy’s support for Deep Capture in a meeting with Catalyst’s lawyers in September 2017, said that he felt that 25 percent of it was so untrue it calls into question the balance of the work.)

And it ought to be recalled that making these types of allegations can have consequences, especially in Canada, where libel and defamation laws favor the plaintiff.

In 2008, Overstock.com’s Byrne and his then colleague Mark Mitchell published “Deep Capture,” a conspiratorially virulent expansion upon Byrne’s “Miscreant’s Ball” thesis. Altaf Nazerali, an occasional small cap stock promoter depicted in Deep Capture as an international terror finance operative, sued for libel in British Columbia’s Supreme Court. After a lengthy and expensive trial, Byrne, Mitchell and the other defendants lost the case, and in a scathing judgment, were ordered to pay $1.2 million dollars in damages.

Wearing a wire

One company that appears to have placed great stock in Snowdy’s information is MiMedx Group, an Alpharetta, Georgia-based manufacturer of skin graft and wound care products.

MiMedx filed suit in October 2017 against a series of short sellers, claiming the company had been libeled and that its business prospects were interfered with. A month later, Parker “Pete” Petit, MiMedx’s outspoken founder and CEO, began making public remarks about short selling that were nearly identical to Guy’s.

Petit focused particular ire on Marc Cohodes, accusing him in an October 13, 2017, post on the company’s website of being the ringleader of a short seller “circus” and spreading misinformation. This was baffling in that, as Cohodes put it, “I had never heard of the company until that moment.” (Cohodes also won the fight against MiMedx’s management: On February 23, Petit was sentenced to one year in prison; the COO received the same sentence.)

To get more information on Cohodes and other short sellers, MiMedx’s outside law firm, Wargo French, hired Snowdy. (David Pernini, the firm’s Atlanta-based partner that directed Snowdy’s engagement, did not return a phone call seeking comment.)

Snowdy confirmed that he had worked in 2018 for MiMedx, but that it was not a standard engagement for him. He said that he was doing so within the context of “working undercover” for an unspecified federal agency.

“Any email or report I wrote for [Wargo French] was scripted” by this federal agency, said Snowdy.

Pressed on the identity of this purported agency over several weeks, Snowdy would only say this organization’s mission is, “criminal justice, with the power to arrest people.”

Asked how much MiMedx paid him to report on Marc Cohodes and other investors critical of the company, Snowdy said he didn’t get a dime. When Snowdy was asked why he would work for free, and if that triggered any suspicions at MiMedx, he declined to comment.

Incredibly, this story gets even more unusual, with Snowdy alluding to “settlement terms” in the U.S. and Canada that prevented him from discussing his MiMedx activities.

A call to the FBI seeking comment was not returned.

Vincent Hanna dials in

Guy initiated contact with Glassman on August 11, 2017, via email, and using the pseudonym “Vincent Hanna,” a character portrayed by Al Pacino in the 1995 movie “Heat.”

(In a strange aside, Snowdy, in his letter to West Face’s lawyers, recounted meeting a pair of individuals in a New York office lobby in early 2018 who introduced themselves as “Vincent Hanna” and “Neil McCauley,” the name of the movie’s Robert DeNiro character.)

While Guy used a pseudonym for an additional 12 days, he wasted little time in telling Glassman the names of short sellers he suspected were involved with Callidus Capital’s stock. Ironically, given Snowdy’s role, as well as Catalyst’s extensive use of Black Cube, Guy warned Glassman that private investigators were likely tailing him and that Russian hackers could be trying to disrupt his fund’s operations.

(There has been no suggestion Guy or Snowdy had anything to do with Black Cube’s operations; Snowdy, in remarks to the Foundation for Financial Journalism, said that he believed he was a target of Black Cube too.)

In notes from an August 23, 2017, conference call with Catalyst executives and lawyer’s, Guy — still using the “Vincent Hanna” moniker — continued to frame his objection to short selling along familiar lines: Arguing Concordia was “a dry run” for taking down the much larger Valeant Pharmaceuticals, making allegations of possible Russian and Hong Kong money laundering, speculating about organized crime money at work shorting stocks, and Marc Cohodes.

Glassman was not a fan of Snowdy

The unsealed documents show Catalyst executives and lawyers eagerly anticipating Snowdy’s research, and they afforded him three separate opportunities to present his findings.

But when Snowdy could not — or would not — produce the desired recordings and emails that Guy had assured them his investigator possessed, Glassman became a vehement critic.

Glassman, quoting his lawyer after one meeting with Snowdy, said he provided, “Two and a half hours of interesting but unusable bullshit — and two and a half minutes of food for thought.”

And Glassman appeared especially angry at Guy’s inability to force Snowdy to produce them since any of his work product would belong to Guy as the client.

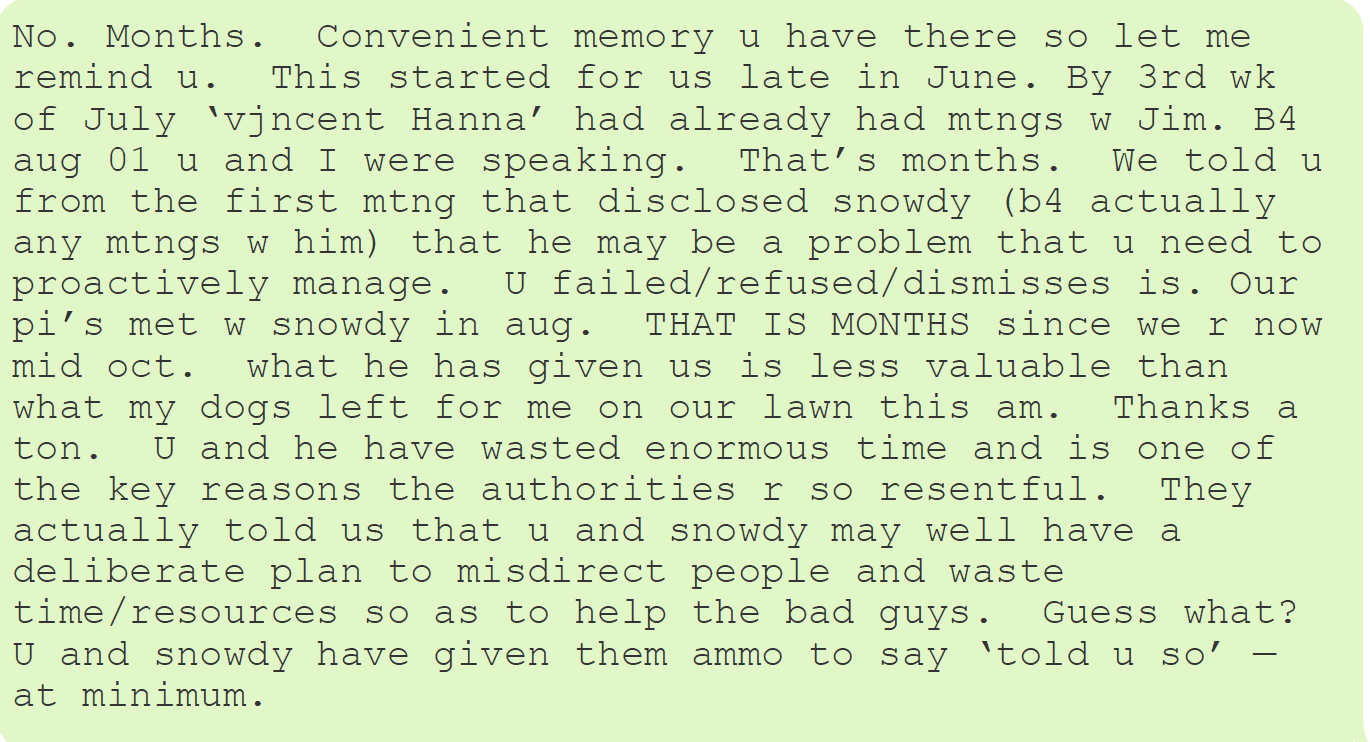

“Right now [Snowdy] is using u and hurting u badly. U clearly r too stupid or blind to see it,” wrote Glassman.

Snowdy’s evidence, “was less valuable than what my dog’s left for me on my lawn this [morning.]”

All those documents? None of them are real

For six weeks the Foundation for Financial Journalism has been in frequent contact with Snowdy about his work for Danny Guy. Questions begat more questions and Snowdy’s response has never wavered.

He insists that almost none of it happened.

In other words, Snowdy did not work on behalf of Danny Guy to infiltrate any networks, and has not spoken to Danny Guy since “sometime in 2016.”

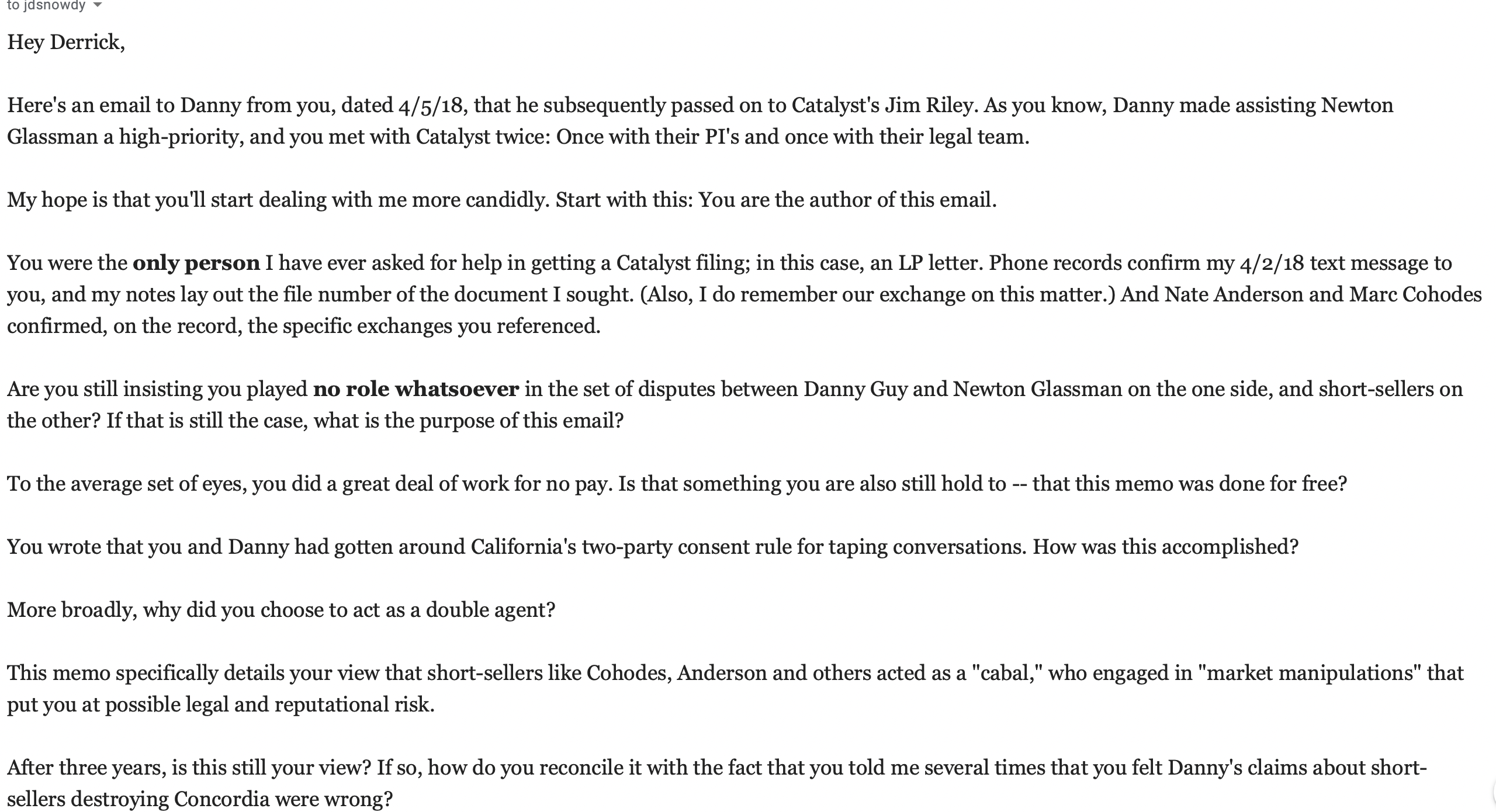

The Foundation for Financial Journalism showed Snowdy emails between himself and Guy discussing his assignment in April 2018, naming certain reporters and short sellers of interest to Guy and Catalyst.

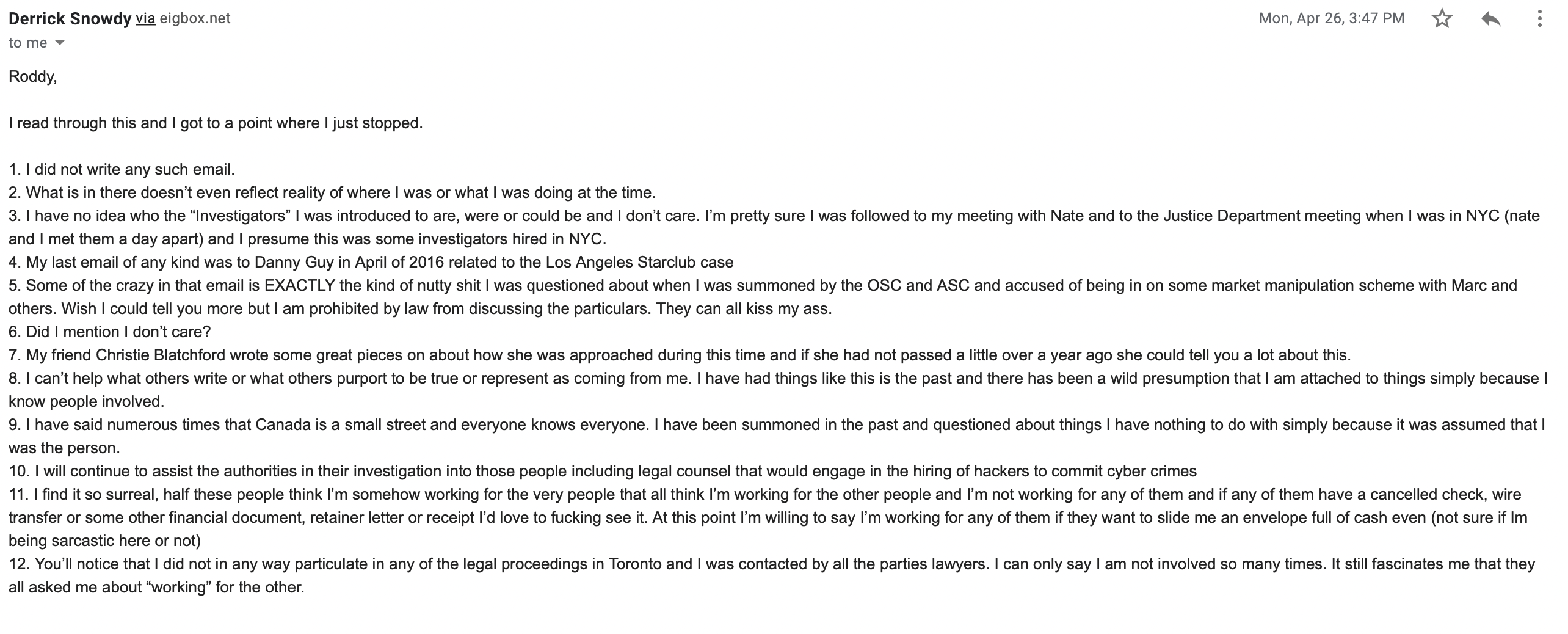

“Forgeries,” he speculated in a phone interview. “But I can’t really be sure. You would be amazed at the shit I’ve seen go down up here in terms of corruption.” (He was entirely indifferent to a reporter’s speculation that no one would believe a word of what he said.)

What about Snowdy’s prominence in numerous documents written by Glassman’s own lawyers, which a judge – as part of a broader 55 page ruling — ordered submitted into discovery? Snowdy told the Foundation for Financial Journalism that he did not care to speculate “who got what wrong, or why.”

Snowdy did admit being at the meetings with Catalyst’s Jim Riley and the firm’s outside lawyers, but said he primarily discussed whether Catalyst had a role in some hacking attempts he had discerned on his own smartphone and computers.

Not so strong on the facts

There is a chasm between what Snowdy reported to Guy, Catalyst’s lawyers and investigators, and what can be objectively verified.

Snowdy said that he had worked with Carson Block on his Sino-Forest short and was an attendee at a Christmas party he threw. Block, however, said Snowdy had nothing to do with Sino-Forest — which he shorted in 2011, and which filed for bankruptcy protection in 2012 — and that apart from one breakfast with him in 2015 in San Francisco, he has never met him again.

[In disclosure: In 2020 Carson Block donated $5,000 to the Foundation for Financial Journalism.]

“Over the years, maybe from 2016 to 2018, we used [Snowdy] to help us track down documents on a handful of Canadian marijuana companies [Muddy Waters Capital] was considering shorting. I’m confident that we didn’t pay him over $10,000,” said Block. “And it’s been awhile since the fund worked with him, I can tell you that.”

Snowdy claimed Cohodes asked him to short stocks along side him, that he was invited to stay at his house, and, as “a loyalty test,” that he had been left alone with his son Max, Cohodes’ 33-year-old son with cerebral palsy. Nothing close to that happened.

“My God what bullshit,” said Cohodes.

“None of that happened. The part with Max is maybe the most insulting,” he said.

More stuff that Cohodes said didn’t happen: Having offshore bank accounts — something he denies in full throat — and using Anson Funds (a Canadian money manager named in the litigation) to manage his money.

“I don’t need help from [Anson] to make money,” Cohodes said.

The truth of the matter, according to Cohodes, is that Snowdy came to his house once for lunch. When he traveled to Toronto for business on several occasions, Cohodes said Snowdy drove him around.

For all that, Cohodes said he had been dragged into this controversy despite never having shorted a share of Callidus’ stock.

A personal disclosure and a mea culpa

One thing Snowdy was at least partially correct on: The introduction to Cohodes, an obvious ticket into the broader short seller community — came from me.

So some first person disclosure is called for.

First off: How did I get introduced to Snowdy? Carson Block.

According to Block, in early 2015 Snowdy contacted him out of the blue and pitched him on a story on Canadian Rail. He passed on it but suggested to Snowdy I might find aspects of the story compelling from a journalism standpoint. Block and I spoke briefly about why he passed on the story at the time and have never again discussed the issue.

I shelved the story for months. Later in the year I re-examined the parts of it that I found interesting, and in 2016 I began to report it. As part of that I reached out to Snowdy — there had been no contact between us since the year before — and he agreed to put me in contact with a man he said was his client. The client had a large cache of Canadian Rail documents that emerged from a litigation he was then involved in.

His client wanted to interact in person so I flew to Toronto. Snowdy picked me up and drove me to his client. We had a few meals in transit, and on two of the four days I was in the area, Snowdy gave me a lift to his client, and he discussed with amusement a judge’s attempt to prevent him from speaking about Canadian Rail. The story Iwrote in December 2016 was almost entirely informed by my work in those documents.

It turns out Snowdy lied to me about his legal trouble in that case, having received a restraining order in 2014, according to the recently unsealed documents. (I recall looking for a mention of him in the court record and not finding any, but the ruling may have been sealed at the time or attached to a motion I overlooked.)

While driving with Snowdy, he repeatedly discussed his skepticism of Concordia and Home Capital Group, a then troubled mortgage issuerCohodeswas publicly critical of. Snowdy asked me for an introduction to Cohodes. I agreed, sent an email introducing them, and never thought of it again.

What emerged afterwards is personally and professionally horrifying: Cohodes took my word that Snowdy seemed like a regular, well intentioned guy; he proved to be the very opposite of that. Over the course of a few years Snowdy used Cohodes’s name to come into his own house, meet numerous investors and it is a fair bet that any number of the people Snowdy met through Cohodes were surveilled, recorded, and through no fault of their own, may yet have some legal headaches.

Worse, with a connection to Cohodes established, Snowdy eventually got work surveilling him from MiMedx, a company that took fighting short sellers to a new level. The campaign initiated by the company’s ex-CEO was so ugly that even baseless money laundering accusations became forgettable after he leveraged his political connections to a Senator who requested that the FBI visit Cohodes’ house and warn him about a threatening tweet.

And all from my brief email introduction. It is a mistake I deeply regret.

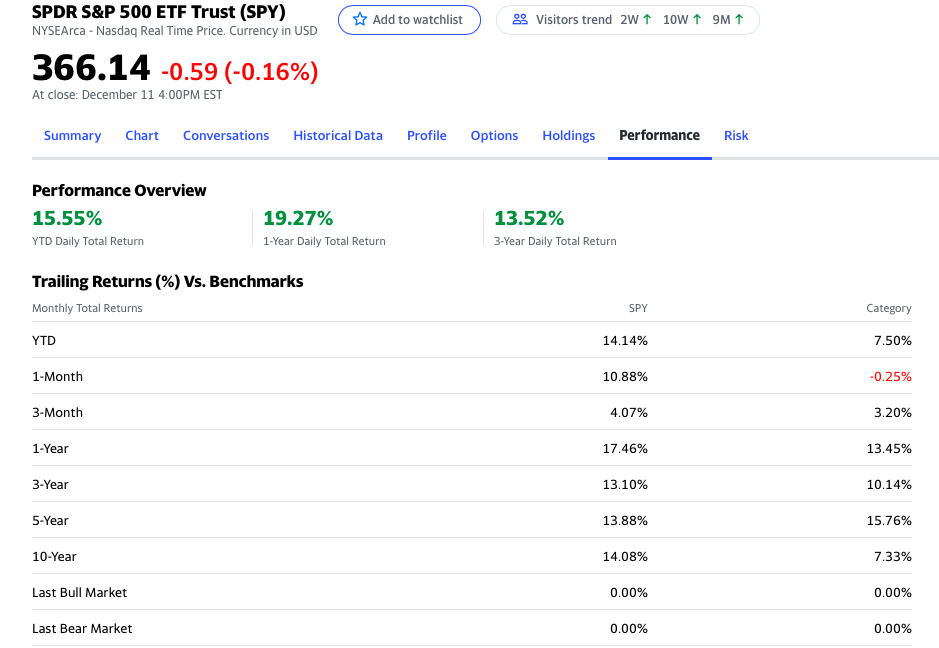

If one word could describe the U.S. stock market of 2020, it would be “improbable.” The S&P 500, for example, has risen about 14.14 percent this year despite a pandemic that is deadly to both people and corporate profits. Yet even after witnessing this year’s string of unprecedented developments, investors might be shocked to learn what lies behind the recent muscular share price growth of Freedom Holding Corp. This Las Vegas–incorporated bank and securities brokerage has its principal office in Almaty, Kazakhstan, and a major presence in other cities of the former Soviet Union.

In Freedom Holding’s most recent quarterly filing of Nov. 19, management attributed the company’s earnings success to customers undertaking a higher volume of trades as a result of “the unique market characteristics surrounding the COVID 19 pandemic.” In other words, quarantined or marooned investors are day trading to pass the time as disease spreads across the world. And thus Freedom Holding’s astronomical revenue growth has seemingly made it the fastest-growing financial services company on Earth.

So why aren’t the big brokerage operations of the U.S. and Western Europe replicating this model? A clue as to why they are not can be found in Freedom Holding’s Securities and Exchange Commission filings. The Foundation for Financial Journalism has found that Freedom Holding serves up gaudy growth figures with few disclosures or incongruous explanations at best — and accompanies them with an operations structure akin to that of a penny stock company.

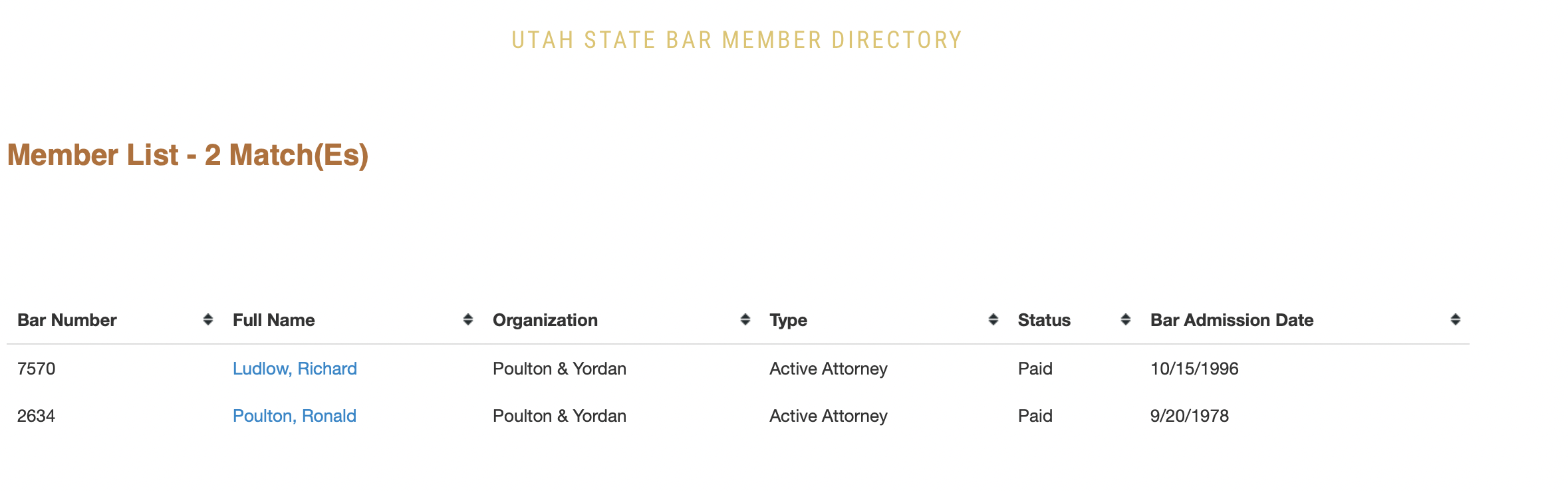

Despite the fact that Freedom Holding is incorporated in the States and its shares are traded on Nasdaq, nothing about its actual U.S. presence should give American investors any confidence. LinkedIn lists only one U.S.-based Freedom Holdings employee. And the company has situated its U.S. headquarters inside a Regus coworking space. The company’s auditor, Salt Lake City–based WSRP LLC, has just 16 partners and only four publicly traded clients, according to a Public Company Accounting Oversight Board filing. Similarly Freedom Holding’s outside legal adviser, the law firm Poulton & Yordan, has merely two licensed attorneys and no website. All the while, most of the company’s operations — taking place in its trading and retail brokerage division, Freedom Finance — are carried out thousands of miles away in numerous jurisdictions, mostly in Russia, Ukraine and Kazakhstan, but also Europe, and quite actively in Cyprus.

Although Freedom Holding’s SEC filings do not reveal how it is making its great fortune, its subsidiaries’ audited financial statements do. These filings reveal that the company’s Cyprus unit is staggeringly profitable, having earned more than $33 million last year following a $30,000 loss in 2017.

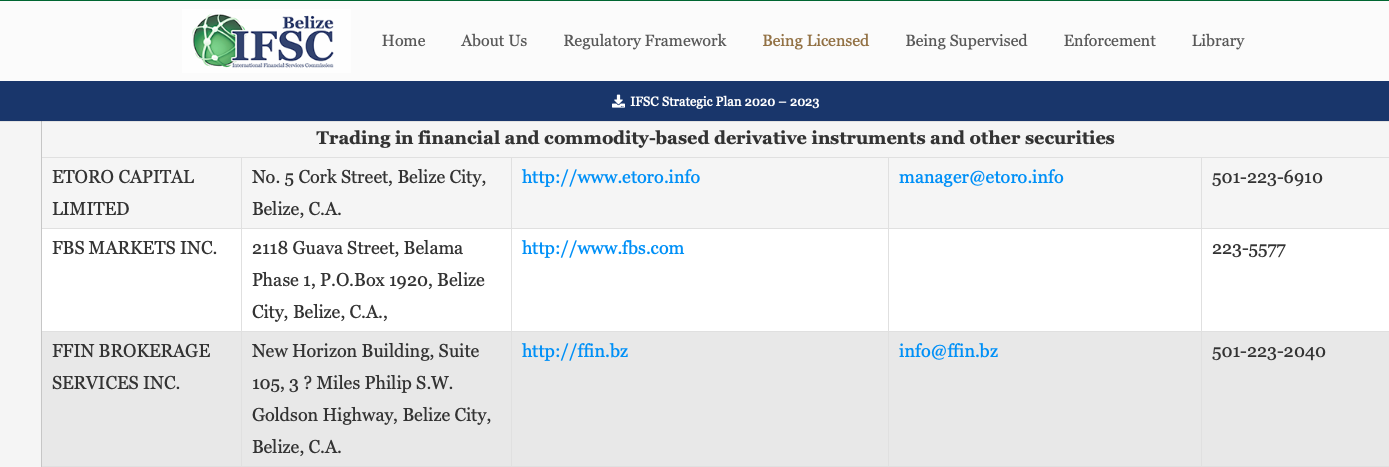

Additionally, Freedom Holding has a highly unusual relationship with a company based in Belize that’s owned by Timur Turlov, Freedom Holding’s founder and CEO. While little is disclosed about it in Freedom Holding’s SEC filings, this Belize entity, FFIN Brokerage Services, appears to have access to the funds of Freedom Holding’s clients for as long as 93 days, a major deviation from typical brokerage industry practices across the globe.

Reporting earnings that might be too good to be true

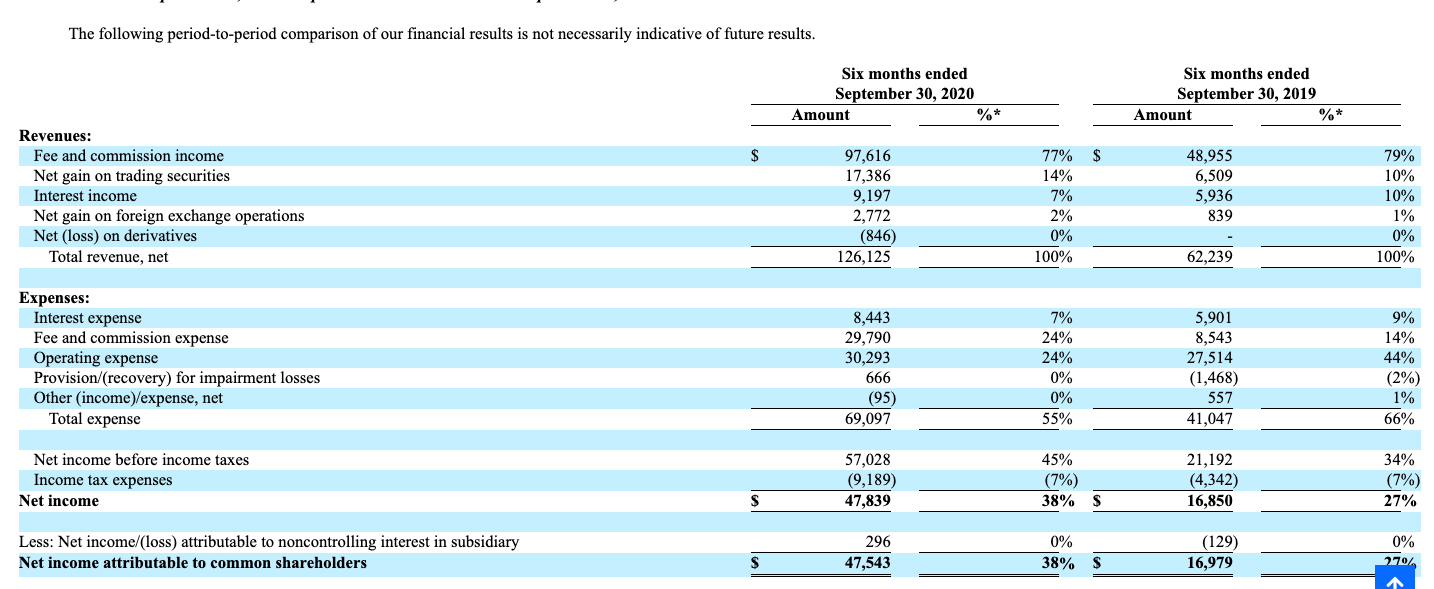

Analysts reading Freedom Holding’s most recent quarterly filing will be hard pressed to explain its earnings growth. In the first six months of its financial year that ends on March 30, the company had its net income rise to $47.83 million, nearly triple what it reported for the same period a year ago — and more than double the $22.1 million it earned in all of fiscal 2019.

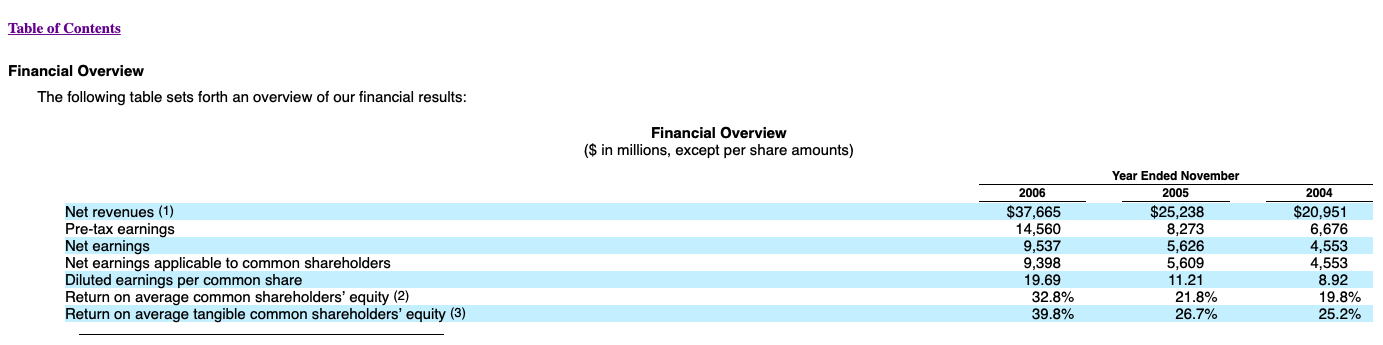

How unique is Freedom Holding’s almost 38 percent net profit margin? Goldman Sachs — long Wall Street’s most profitable company — managed only a 25.3 percent net profit margin in 2006, during the manic run-up to the global financial crisis.

Freedom Holding’s filings suggest that its managers have apparently solved an enduring mystery of the business world: figuring out how to turbocharge revenue growth without triggering a concurrent spike in expenses or risk.

Growing a business typically requires managers to invest in new hires, technology or plant improvements in the hopes that each $1 spent will net $1.50 before taxes in three to four years. But Freedom Holding’s income statements imply that its management can spend 75 cents to realize a return of $3 in just a few months, all without having to sell stock or take on a mountain of debt.

The universe of companies that claim to do this is limited to Freedom Holding. Even profitability and capital efficiency superstars like Google and Berkshire Hathaway cannot approach that performance.

Another factor that sets Freedom Holding apart is its apparent efficiency and productivity. A business in an aggressive expansion mode typically registers a depressed revenue-per-employee figure as it assumes front-loaded costs (adding head count, paying for technology updates) that do not immediately result in new revenue.

Not so for Freedom Holding, though. In fiscal 2019, it generated $81,649 in revenue for each of its 1,343 full- and part-time employees; in 2018 that figure was $65,105 for every one of its 1,141 employees. Adding only 202 employees in fiscal 2019 led the company to triple its net income.

Promising grand returns on IPO shares

Marketing materials in English on the European version of Freedom Finance’s website present a simple proposition: Tap Freedom Finance to invest in U.S.-listed initial public offerings for a golden ticket to profits. (The website’s Russian text translates into this English prose with Google Translate.)

To whet investors’ appetites, a brochure posted on Freedom Finance’s website declares that since 2012, a set of 107 seemingly randomly picked U.S.-listed companies have reaped returns of 129 percent on average following their IPO.

And a YouTube promotional video for Freedom Holding’s Freedom Finance Europe claims that it secures 50 percent returns on IPOs (after a “three-month lockup” period ends).

Putting aside whether grandiose claims are true or not, Freedom Finance holds no U.S. securities industry registrations or licenses and cannot underwrite U.S.-listed IPOs or participate in the activities of syndicate selling groups. It must rely on other brokerage firms to execute trades on U.S. exchanges for its clients. (In Kazakhstan, Freedom Finance does, however, underwrite IPOs, according to a June 2017 Reuters article.)

Yet Freedom Holding’s clients are buying shares of companies’ initial public offerings – in large quantities.

Routing transactions to a Turlov outfit in Belize

The way these trades are apparently being accomplished is through a complicated maneuver: Freedom Holding’s clients send money to FFIN Brokerage Services Inc., a Belize City–based broker-dealer whose website promises “direct access to the U.S. market.” Yet FFIN Brokerage Services is not a subsidiary of Freedom Holding. Instead Freedom Holding CEO Turlov owns it, as clearly laid out in Freedom Holding’s July 2018 proxy statement.

Turlov’s ownership of FFIN Brokerage Services seems to be a detail that Freedom Holding is not keen to frequently share. True, the fine print of a 2017 prospectus also alluded to this fact, as did a 2019 Cyprus regulatory disclosure. And, yes, a June 2019 S&P ratings note once described FFIN Brokerage Services as Freedom Holding’s “largest counterparty.” But other Freedom Holding documents, especially its SEC quarterly and annual filings that more investors would regularly encounter, do not mention FFIN Brokerage Services or Turlov’s ownership of it.

And FFIN Brokerage Services is likely involved with Freedom Holding’s hefty number of related-party transactions. Numerous Freedom Holding’s brochures and contracts instruct clients to send their funds to FFIN Brokerage Services. A Freedom Holding marketing document in May 2017 apparently referred to FFIN Brokerage Services as having “conducted a series of [IPO] deals this year,” per a translation offered by Google Translate.

Yet, apart from FFIN Brokerage Services’ holding a license to trade foreign currencies in Belize, the company lacks regulatory approvals to execute trades in any other countries. Despite this, a disclosure by Freedom Holding’s Cyprus subsidiary about its top brokers cited FFIN Brokerage Services as handling as much as 9.12 percent of its equity orders in 2019. And Freedom Holding’s 2017 prospectus referred to FFIN Brokerage Services as “a placement agent” for its share offering.

Perhaps the strangest aspect to FFIN Brokerage Services’ involvement is that Freedom Holding’s clients must abide by an unusual 93-day lockup provision, per a FFIN Brokerage Services document. (At other U.S. brokerage companies, a client order for buying or selling public securities, even as part of an IPO, can be canceled at any point until the order is transacted — without any lockups or restrictions.)

Nothing in Freedom Holding’s documents — in English or Russian — explains how clients might benefit from the 93-day lockup of their capital. This arrangement, however, could give FFIN Brokerage Services access to plenty of cash for three months, with the sole obligation of delivering the newly issued shares at the end of the period.

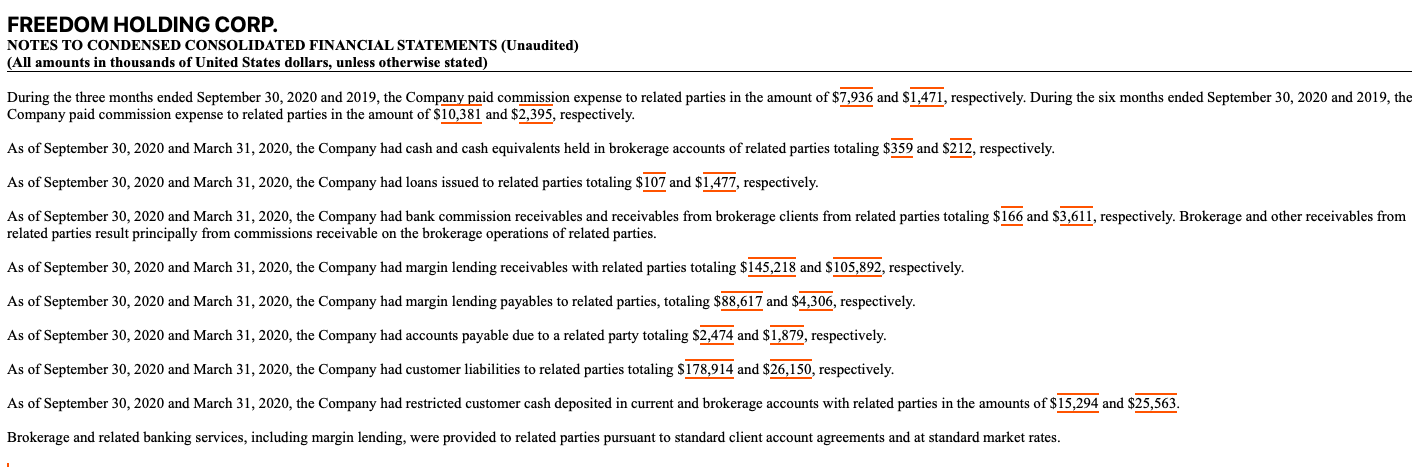

Blurring the lines

In its 2019 annual report, Freedom Holding disclosed 12 different types of related-party transactions with Turlov-owned entities. And during the six months that ended Sept. 30, the value of commissions that Freedom Holding earned from its business with Turlov entities amounted to 57 percent of its $126.12 million in sales — or almost $72 million.

Because Turlov’s related-party dealings with Freedom Holding are so extensive, one can ask if this company has a strong future doing any business unconnected to Turlov.

And cash is going out the door to Turlov-linked affiliates as well: Through Sept. 30, more than one-third of Freedom Holding’s commission payments, or $10.38 million, went to entities owned by Turlov.

While related-party transactions are legal, savvy investors often closely scrutinize them to ensure that executives are not misusing shareholder assets for private gain. To that end, the SEC requires public companies to disclose such relationships in their annual proxy statements. And when public companies have not been forthcoming in describing their role in handling a CEO’s or a board member’s private investments, the SEC has been aggressive in filing claims against such companies and their executives.

Michelle Leder, the founder of Footnoted, described Freedom Holding’s related-party dealings as “more than a bit dizzying.” Her subscription service analyzes public company filings for evidence of potential transactions or misleading data.

“I almost felt like I needed a flowchart to figure [the related-party transactions] all out — lots of money going back and forth between different entities with Turlov being the common link,” Leder said.

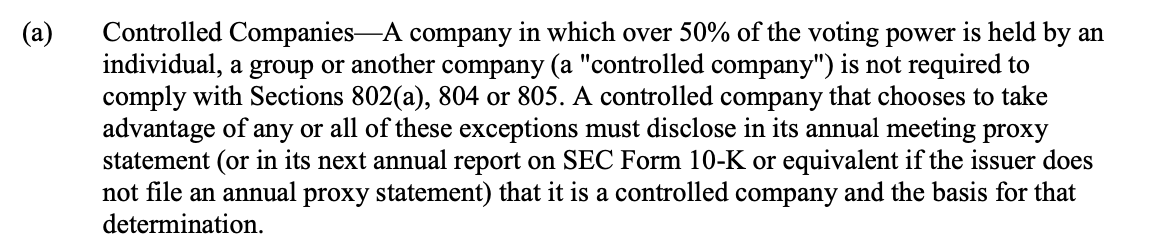

One possible explanation offered by Leder for the high volume of self-dealing is that the board of directors of Freedom Holding can’t operate as a counterweight to Turlov since it is a controlled company, according to New York Stock Exchangeguidelines. More than 50 percent of its shares are held by one person or entity and thus it’s exempt from SEC requirements for having independent directors.

Raking in capital in Cyprus

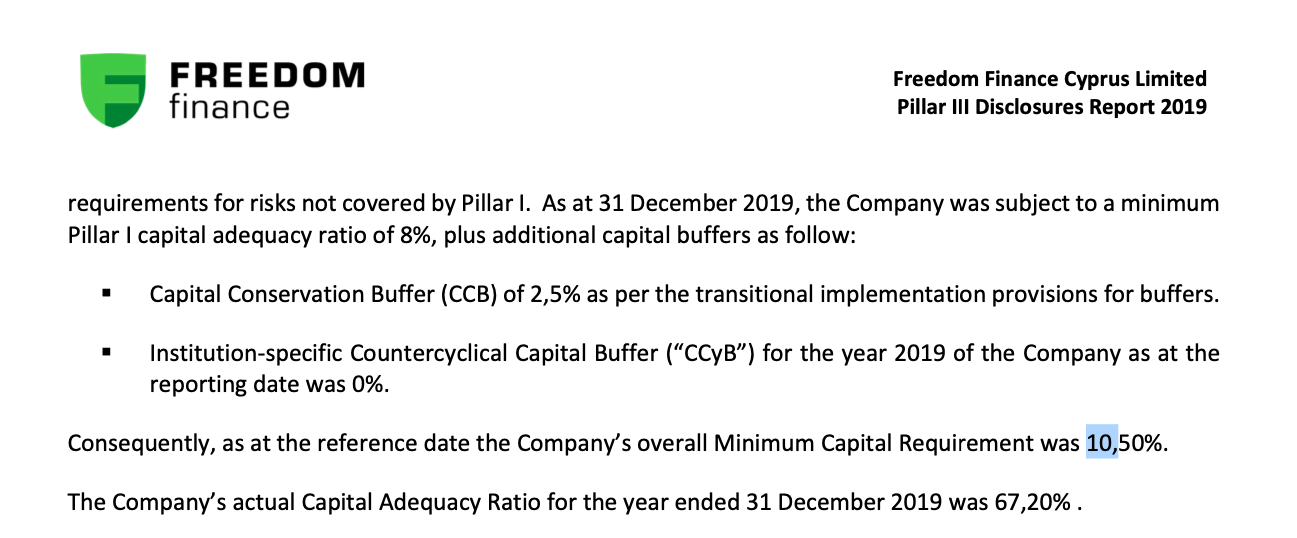

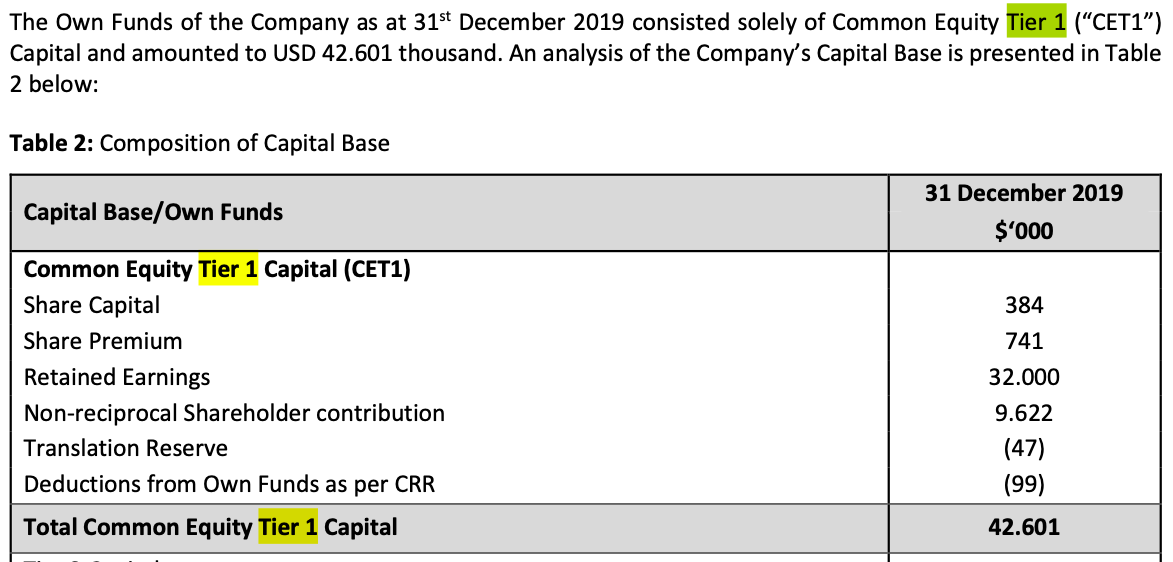

Deeply buried in a regulatory filing of Freedom Holding’s Cyprus subsidiary is a curious detail: The subsidiary, Freedom Finance Cyprus Limited, does not need much capital to generate a lot of revenue.

Put on the green eyeshade briefly: European Union regulations require that financial institutions set aside 10.5 percent of their tier 1 capital (or the sum of their retained earnings and established reserves) as insurance against unexpected losses. Freedom Holding’s European operations, which consist primarily of its Cyprus subsidiary, reported $42.6 million in tier 1 capital at the end of last year. Thus, as of the end of December, the amount of capital that the company’s European operations (known as Freedom Finance Europe) needed to hold in reserve was a little more than $4.47 million. As a result, the Cyrus subsidiary ended up with $38.13 million in ready capital in its coffers.

To be sure, holding additional cash in reserve for various contingencies is prudent for a company. And given stock markets’ volatility, extra liquidity could mean the difference between life and death for a financial services company like Freedom Holding.

The Cyprus subsidiary’s regulatory filings also reveal a rather remarkable profitability. For fiscal 2019, the subsidiary earned $33.80 million, more than fiscal 2018’s $11.9 million and a considerable improvement over its $30,000 loss in fiscal 2017. As the chart below shows, Freedom Finance Cyprus Limited’s total 2019 income was far greater than the combined incomes of Freedom Holding’s other subsidiaries.

Sources: audited income statements

Straining for cash in other parts of the organization

Yet while a pile of cash sits at its Cyprus subsidiary, Freedom Holding is showing signs of being desperate for cash in virtually all other corners of its organization. Freedom Finance Europe is offering money market interest rates that are four to six times higher than what U.S. institutions are promising. Banks usually attract depositors for their money market funds by paying a few extra basis points in interest — but not multiples of what a rival does. U.S. regulators often scrutinize banks whose money market interest rates are outliers within the marketplace on the view that management may want to quickly inject cash to conceal previous losses. In fact, the parent company’s main division, Freedom Finance, is paying its brokers a 15 percent commission if their clients deposit 1,000 euros in cash, according to an “agent agreement” posted on its website.

Furthermore, the way Freedom Holding funds its operations is not congruent with the typical practices of a company that can readily access $38 million in cash. The company’s banking and brokerage subsidiaries in Russia and Kazakhstan, operating under the Freedom Finance umbrella, are funding themselves through sales of short-term bonds with high interest rates — ones even as steep as 12 percent. Unless they have no other option, most corporate management teams would try to use available resources to reduce a drag on earnings from interest expense.

Exactly what is Freedom Holding doing in Cyprus to make that kind of money? The Cyprus subsidiary’s primary operation is offering Freedom24, an online trading platform it touts as “an online stocks store.” Until earlier this year, Freedom 24 used fraudulent credit card processor Wirecard for payments. Cyprus is also where Freedom Holding has based its nascent Freedom Finance Europe division that’s aimed at capturing business from day traders and individual investors in the Western European market.

Even though the customers targeted are individuals who are new to trading or investing, Freedom24 and Freedom Finance Europe are bare bones offerings in comparison with the mobile applications offered by, say, InteractiveBrokers or TD Ameritrade.

Partnering with a troubled company to execute trades

Furthermore, Freedom Finance Cyprus Limited is enlisting a brokerage that recently landed in regulatory hot water to carry out its trades: New York–based brokerage firm Lek Securities. The SEC alleged in 2017 that Lek Securities had improperly traded options for Ukrainian clients.

(In October 2019, Lek Securities’ co-founder Samuel Lek agreed to pay a $420,000 penalty and admitted to the SEC that he had broken federal securities laws. Lek Securities paid $1.52 million in penalties and disgorgement and also acknowledged a series of violations. FINRA, in conjunction with other U.S. exchanges, gave Lek a lifetime ban from the securities industry and fined Lek Securities an additional $900,000 for its supervisory failures.)

And Freedom Finance’s tight relationship with Lek Securities goes back years. SEC correspondence shows that in 2015 Lek Securities sought to act as a prime broker for a planned Freedom Finance brokerage in the U.S. named FFIN Securities Inc., for which it would process and match up its trades, as well as serve as a custodian for its securities. (Freedom Finance dropped the project the following year.)

In addition, with Freedom Finance unable to execute its own trades on U.S. exchanges, London-based Lek Securities U.K. Limited last year handled 90 percent of Freedom Finance Cyprus Limited’s equity orders, after doing 99.5 percent of them in 2018.

Betting it all

Curious as to how such a sprawling operation, with units from Belize to Cyprus and from Almaty to Vegas, emerged? In 2008, while a 20-year-old university student, the Russian-born Turlov launched Freedom Finance in Moscow, and it catered primarily to Russian day traders. Turlov bought a small money management firm in 2013.

In November 2015, Turlov merged Freedom Finance’s assets with those of Salt Lake City–based BMB Munai Inc., a dormant oil and gas exploration company that had (unsuccessfully) sought to export oil from properties in Kazakhstan. BMB Munia had for a while listed its shares for public trading in the United States. Turlov renamed the newly merged company Freedom Holding Corporation and incorporated it in Las Vegas. In October 2019, Nasdaq listed it on the Nasdaq Capital Market tier of early-stage companies. And just this past August, the company’s Kazakh brokerage unit, Freedom Finance JSC, purchased Bank Kassa Nova JSC in Kazakhstan. This joined the Moscow-based retail bank (FFIN Bank) that Freedom Holding had bought in 2017.

In a September profile of Turlov, Bloomberg News noted that the financial services assets he had begun cobbling together in 2008 now amount to one of Russia’s 10 largest brokerage firms. A Bloomberg article from October 2017 is more illuminating: Turlov is revealed to have a riverboat gambler’s risk management practices.

Kazakhstan-based Freedom Finance JSC borrowed money using short-term repurchase agreements, pledging its (large) positions in the stocks of a handful of local companies as collateral. The Kazakh brokerage then used that money to expand its market-making activities (such as posting the prices it offers to buy and sell stocks) on the Kazakhstan Stock Exchange.

This was an incredibly risky strategy. Emerging market equities are frequently thinly traded and volatile. Had the price of Freedom Finance’s pledged stock declined, the firm’s repurchase-agreement counterparties could have either immediately demanded additional cash as collateral or seized (and sold) the pledged shares, threatening the company’s solvency.

Yet as a chart of the Kazakhstan Stock Exchange index shows, Turlov’s gambit worked: Freedom Finance, the exchange’s busiest trader, profited handsomely when the stocks it made markets for gradually increased in value. Freedom Holding’s fiscal 2017 10-K annual report shows a securities trading gain of $23 million, to $33.74 million, from $10.8 million in the prior fiscal year.

– – – – – – – –

In the weeks prior to publication of this article, the Foundation for Financial Journalism sought comments from Freedom Holding. After Adam Cook, the company’s corporate secretary, declined to make Turlov available for a telephone interview, email questions were sent on Nov. 12 and again on Nov. 13. On Nov. 25, Ron Poulton declined to address them, citing the availability of information in its SEC filings and the company’s website.

Achieving success on Wall Street requires a wide mixture of skills: mastering technical subjects, such as math, economics and finance; earning and keeping the respect of others (and vice versa); and displaying good judgment. Yet apart from passing the Series 7 exam, an elementary test of securities industry rules and concepts, few other credentials are needed before a person can trade government bonds or advise on a big merger.

A clean U5 form, issued by Wall Street’s banks and brokerages, cannot be obtained, however, by undergoing schooling or passing tests.

The U5, or FINRA’s Uniform Termination Notice for Security Industry Registration, is a document that any banking or brokerage firm that a member of FINRA files when an employee departs, for whatever reason. FINRA, also called the Financial Industry Regulatory Authority, is Wall Street’s self-regulatory organization.

Don’t be fooled by the dull title, though; the U5 is one of the most important documents on Wall Street. And negotiations to discuss them can easily become a battleground where employers and employees fight over whether an upcoming exit will be classified as a resignation or a firing — and if problematic behavior is revealed.

On the U5 form, the employer must provide the reason for termination as “voluntary,” “permitted to resign” or “discharged” (or “deceased or “other”). If the employee has been “discharged” or “permitted to resign,” the employer is supposed to fill in a “termination explanation” box with a reason. Banks or brokerages must also indicate if the exiting employee is currently subject to (or was when terminated) an investigation by a foreign or domestic governmental body or a self-regulating organization, or is undergoing an internal review related to issues of fraud, the wrongful taking of property or a violation of industry standards of conduct. Criminal felony charges (such as some cases of sexual harassment) and some misdemeanor infractions are also to be recorded.

Blaine Bortnick, a lawyer who specializes in Wall Street employment practices, said the U5 is a powerful lever for banks and brokerages to wield: Compliance officers at a prospective employer can stop the hiring of anyone with only a slight infraction — if the matter is ever recorded on a U5. “Compliance always can put the kibosh on a hire if they don’t like the U5 regardless of what the business does,” he said. “They’ve got that power these days.”

Thus, a “marked up” U5 can end a Wall Street career for most people, according to Bortnick, and bank executives have almost military-like power over their employees as a result. Indeed, in New York (where many financial companies are headquartered), the state’s supreme court has ruled that an employer’s filing of a U5 is privileged from court proceedings; an employee cannot sue a firm for defamation based on a U5.

Certainly if employers were more honest on U5 forms about the precise reasons for employees’ departures, others companies could much more easily determine if a prospective hire had been terminated for cause, such as violating a federal regulation or law, or if the departure had been involuntary but connected to a strategic shift or cost cutting. If FINRA enforced a more rigorous standard of disclosure, this might prompt some employers to make different hiring decisions. To be sure, any such change in U5 disclosure practices would also raise substantive questions about employee due process and privacy. Further reforms might address if firms are arranging hasty, informal verbal negotiations to let problematic executives leave with a “voluntary” departure (when no termination reason must be noted on the U5) before these employers conduct their own internal review or refer a case to law enforcement.

In the wake of the #MeToo movement’s fostering of a rapid cultural shift in attitudes and employment practices, a trader or banker whose U5 shows allegations of sexual harassment or the breaching of a code of conduct might have greatly diminished job prospects.

Wall Street’s history is full of examples of banks that repeatedly ignored the gross misconduct of certain individuals because they generated a lot of revenue. But an honest U5 disclosure regime might pose reputational and legal risk for FINRA member firms.

Even though one FINRA rule seems to forbid sexual harassment and abuse, a bad actor is not prevented from landing a new job at a different firm if his (or her) previous employer fails to be forthcoming on a U5 form. Rule 5240 states, “No member or person associated with a member shall . . . engage, directly, or indirectly, in any conduct that threatens, harasses, coerces, intimidates or otherwise attempts improperly to influence another member, a person associated with a member, or any other person.”

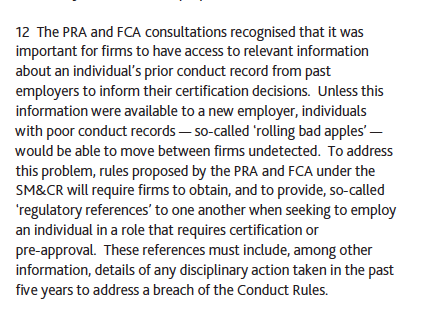

Regulators in the United Kingdom have taken an approach to this issue that might be instructive for their U.S. colleagues. U.K. officials observed that individuals who left one firm for another with little disclosure about prior conduct problems caused a good deal of mayhem; these regulators even coined a phrase for this practice: “rolling bad apples.”

In a review ordered by the Bank of England and Chancellor of the Exchequer following the global financial crisis of 2009 and the Libor-fixing scandal, regulators said banks and brokerages needed to have much more detailed information about potential “rolling bad apples.” Officials laid out their recommendations in a June 2015 Fair and Effective Markets Review. The Financial Conduct Authority now requires firms to provide or obtain a “regulatory reference” on all new managerial and executive hires, including a detailed account of any disciplinary actions taken within the past five years.

In June 2018 when Todd Richter left Barclays Capital in New York City, his new employer, Guggenheim Securities, wasted little time before issuing a press release that trumpeted the hiring of a new senior managing director for its health care investment-banking group.

Richter’s hiring was worth crowing about, since he had worked at the biggest firms on Wall Street — and at the highest levels.

Before Richter’s stint at Barclays, where he served as a vice chairman of global health care investment banking, he had been a managing director at Merrill Lynch. Prior to that he held the same title at Banc of America Securities. He spent much of his career at Morgan Stanley, where he headed health care equity research. And for 14 years Institutional Investor magazine picked him for its prestigious All-America Research Team.

During his years at Barclays, from 2015 to 2018, Richter was a so-called rainmaker who worked on some of Wall Street’s biggest deals. For instance, when Mars Inc. bought VCA for $9.1 billion in 2017, Richter’s 35-year friendship with VCA’s founder Robert Antin netted Barclays a $40.9 million advisory fee.

So why did Richter, who is now 62, leave Barclays in the middle of the following year?

What Juliet Cousins described to a reporter about her summer internship at Barclays in 2017 might hold the answer. (Her name is a pseudonym used here to protect the woman from retaliation and harassment.)

Cousins first met Richter in October 2016 when he interviewed her, then a college junior, for Barclays’ investment banking internship program for the following summer.

Interviewed at length by the Foundation for Financial Journalism in March 2019 and again this past July, Cousins described inappropriate workplace behavior by Richter including his making unwanted physical contact and comments about her appearance — as well as his initiating more overt sexual overtures and touching after her internship ended.

‘Why aren’t you cheating?’

Cousins shared what she thought were Richter’s odd questions – biased even – during her job interview: For example, Richter asked her, “Why aren’t you cheating?” Cousins asked what he meant (wondering if this was a trick question), and he replied, “You know there are ‘women’s programs’ [at Barclays] so why are you in the general recruiting [pool]?” Cousins said she interpreted this comment as a reference to something like the bank’s Women’s Initiative Network, which is designed to increase the bank’s percentage of women hires.

A Barclays spokeswoman did not return a call seeking comment about Richter’s views about recruiting women to the bank.

After Cousins tried to clarify Richter’s unusual question, she recalled, Richter followed up with “You seem too weak to be doing investment banking. Why do you want to do this?” She spent 20 minutes calmly trying to convince Richter of her merits.

A few weeks later Richter called her to say she had the job and that he wanted her to work in his health care banking unit. Out of relief and happiness at getting a foot in Wall Street’s door, she shelved her concerns about the interview, she recalled.

When he was asked in June 2019 about that job interview, Richter said only that he was one of six or seven people who had interviewed Cousins.

A kiss upon arrival

In her March 2019 interview, Cousins also described what she considered to be an inappropriate interaction on her first day of work, when she stopped by Richter’s office: In front of some of her new colleagues, Richter kissed her on the cheek and told her that she looked beautiful. She thought this was an odd way for an investment banking managing director to greet a college student in the presence of other staff. “I think I knew he was single,” Cousins said. “And I just thought he was gay because why else would he do that?”

Richter, through a spokesman, late last month said that this incident did not happenand that the first he had heard of it was through a reporter and not Barclays human resources department.

Their brief encounters throughout that summer were in the same vein, she remembered: “He would walk by me in the hallway and would always compliment my outfit.” Another time, in an elevator bank, Richter told her that her “hair looked good pulled back.”

Richter was also adamant last month that he had not provided these compliments, saying, “I never remarked on her looks.”

But her summer at Barclays did not go as Cousins had hoped, she told the Foundation for Financial Journalism. She was not assigned to work in the health care banking group as Richter had suggested would happen. Instead, Cousins said she believed she had been shoehorned into another banking group (with its own group of summer interns) where she felt unwanted and unwelcome, adding that as a result she grew increasingly concerned about her prospects for a full-time job offer from Barclays.

About a week before the summer internship ended, Cousins went to see Richter for advice, and while he did not bolster her hopes for receiving a full-time job offer, he told her to stay in touch, she recalled. “Well whatever happens, here’s my cellphone number,” Cousins remembered Richter telling her. “Text me. We’ll get drinks.”

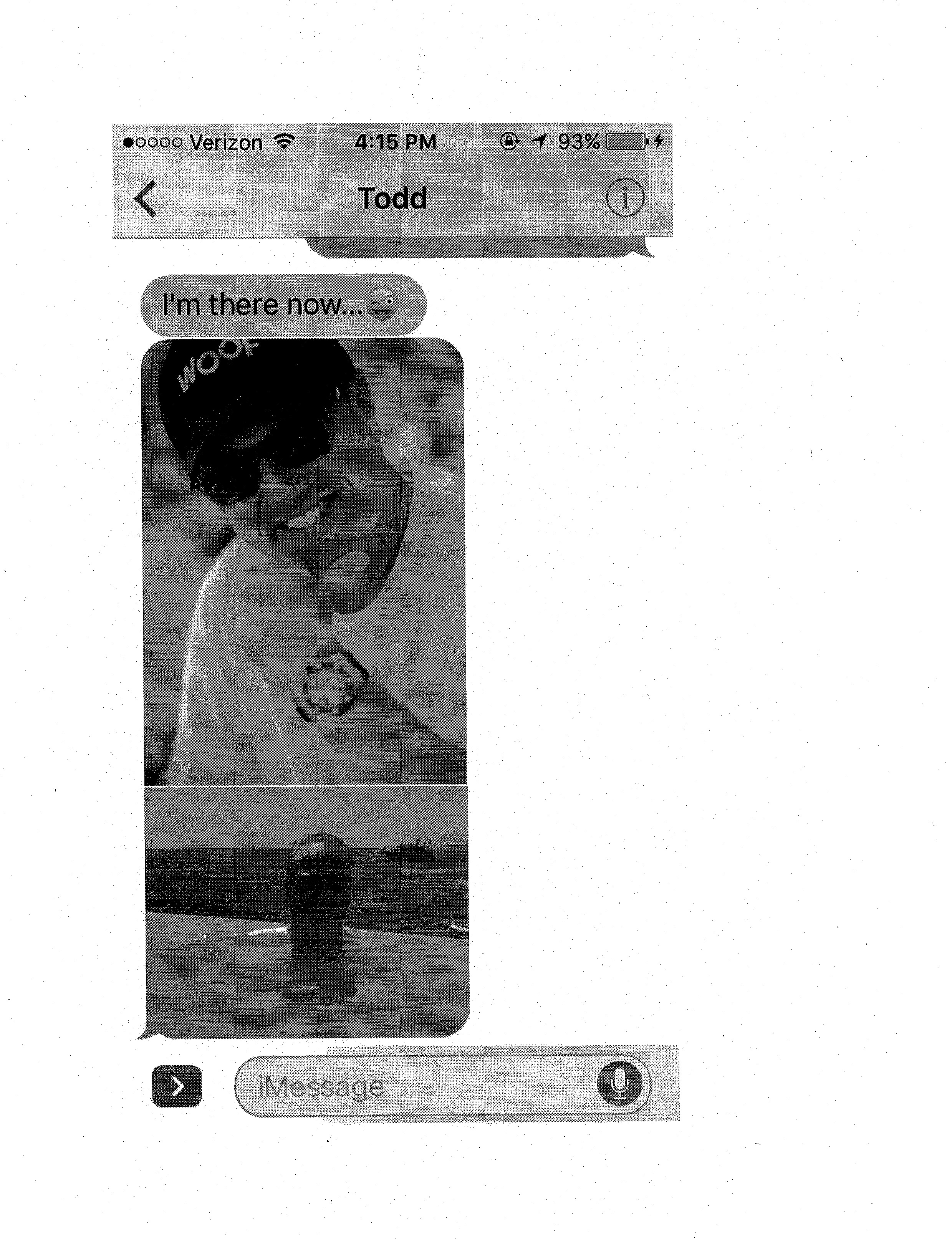

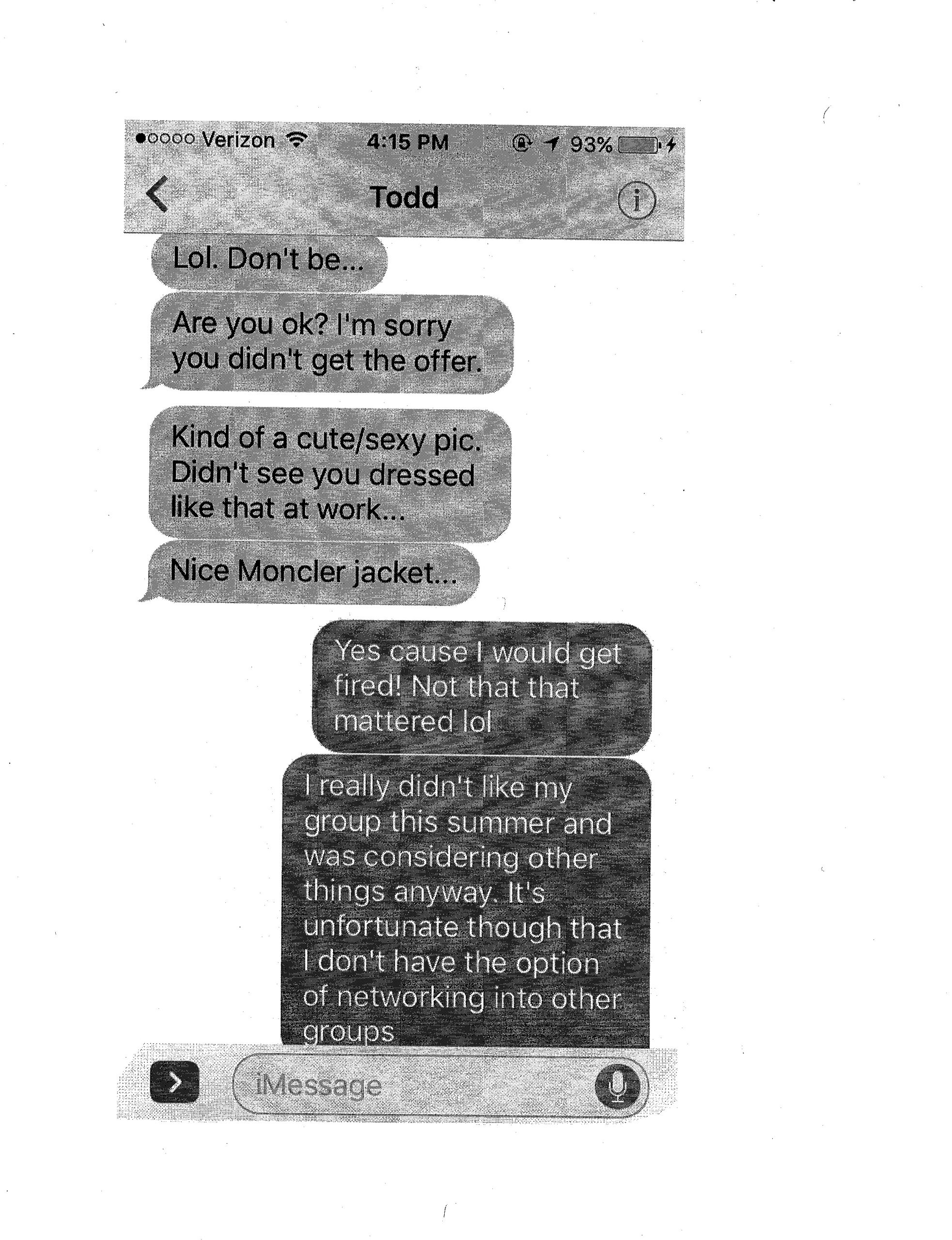

Two weeks or so after her internship ended, with no job offer from Barclays in hand, Cousins felt “really desperate,” she said, about her Wall Street employment prospects “and willing to take help from anyone.” She texted Richter during a vacation in Scotland to arrange a future meeting for job advice. Richter texted back that he also was on vacation and shared two photos with his image, claiming he was swimming on the French Riviera. He was wearing a Rolex. She commented on the watch and sent him a selfie. He noted that she was wearing an expensive Moncler parka and looked “cute/sexy,” adding, “Didn’t see you dressed at work like that.”

Shortly after the two exchanged these messages, Barclays informed Cousins that the firm did not intend to extend her a full-time offer, she said.

An elaborate dinner for a former intern

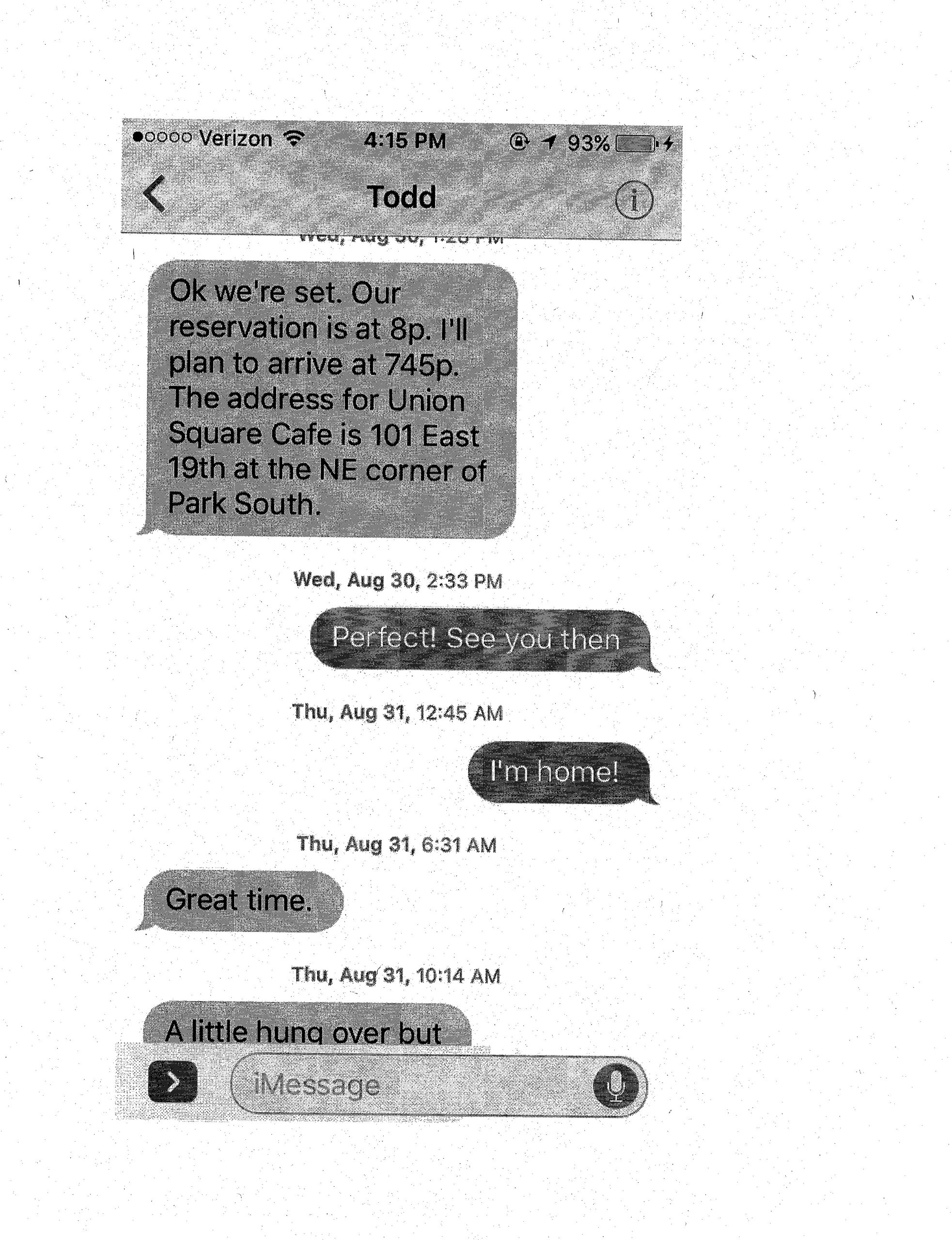

Cousins also described how later that summer the two shared drinks and dinner at a fancy Manhattan restaurant where Richter’s behavior veered into a new, overtly sexually suggestive direction that she said she did not want or encourage. Rather, when Richter asked Cousins to dine with him at Danny Meyer’s tony Union Square Cafe, she hoped he would view their meeting as “a mentor dinner” and understand that she, then only 21, wanted to enlist his connections to land a full-time job after graduation, she said.

Their Aug. 30, 2017, dinner started out innocently enough, with talk about Cousins’ family and friends, but quickly turned strange as the booze began to flow, she recalled. As Richter threw back vodka highballs, he pressed waitstaff to refill her wineglass “before I was even finished,” she said.

Richter emphasized her good fortune at having the opportunity to gain his advice, Cousins remembered. “You’re so special,” he told her. “No other intern [at Barclays] would be able to have dinner with a man like me,” adding that he had wanted to get to know her better over the summer but had held off because “it would have been inappropriate.” And he mentioned that “everyone in his [health care banking unit] had noticed how much he admired her.” Moments later Richter told her he had known during her initial interview that he had wanted to date her, and then he quickly shifted the conversation to her personal life, Cousins said. He called her “beautiful,” she recalled, and wanted to know why she did not have a boyfriend. He then asked her how many people she had slept with.

Richter, however, said late last month he never asked her about the number of men she had slept with.

Cousins remembered the questions from a much older man about her personal life had made her feel “incredibly uncomfortable” and that she gave him “a vague answer.”

In a June 2019 phone interview, Richter offered a radically different account of that dinner and the dynamic between the two of them: Richter initially offered to meet Cousins in his office, but she declined because she felt awkward about encountering former Barclays colleagues after not receiving a full-time job offer. “When we had dinner,” Richter recalled, Cousins “was not employed at [Barclays], and the whole purpose of the dinner was for me to kind of help her and give her advice.”

Richter did not remember excessive drinking at the dinner, saying only that he and Cousins had “split a bottle of wine.” Asked if they had discussed her personal life, he replied that he did not remember anything like that. “At no point did I ever think that I made her feel uncomfortable,” Richter said in the 2019 interview.

Just prior to this article’s publication, Richter was pressed again on Cousins’ allegations. While during his July 2019 phone conversation he had heavily relied on “I do not recall,” his responses in July 2020 were much clearer, flatly rejecting much of her account of his behavior, both during her internship and their dinner afterward.

‘We’re hitting another bar’

But Cousins recalled that she had found it challenging to rebuff Richter’s unwanted advances as the evening progressed. At the end of the dinner, Richter ordered an Uber. “We’re hitting another bar,” he told her. She felt confused, thinking that somehow the dinner meeting was turning into a date, but decided that being in a crowded bar with him would be safe. “He kept emphasizing how powerful he was,” she said. “So I agreed to go to the bar because it seemed like such a big opportunity to be spending time with someone so high up at the bank.”

On their way out of Union Square Cafe, however, Richter “started to touch my butt,” she recalled, adding that she ignored it and entered the Uber with him. They went to a bar at the base of the Residences at 400 Fifth Avenue, where he owned a penthouse condominium. “As we walked up the stairs to the bar, he touched my butt again,” she said. “I didn’t say anything because I was uncomfortable and scared.”

At the bar, Richter ordered two glasses of vodka for them, she recalled. When they sat down, Richter started “staring into my eyes and telling me how beautiful I looked,” Cousins said.

Asked by an interviewer why she did not bolt, Cousins replied, “I don’t know,” adding in retrospect, “I think I should have.”

Cousins also described a further incident that turned into an outright sexual invitation: She was contemplating whether to leave the bar at 400 Fifth Avenue when someone at Union Square Cafe called Richter’s cellphone to say her bag was still there. Richter suggested that they first go up to his penthouse apartment to get Henry, his dog, so they could walk together back to the restaurant. It was a ruse, she said in hindsight, designed to move her upstairs to have sex with him.

In Richter’s apartment things got tense, according to Cousins’ recollection: “He’s trying to cuddle with me,” she said. “And I just keep pacing back and forth to avoid him touching me. Then he stands up and puts his arms around me.” Added Cousins: “He was looking into my eyes saying, ‘What are you thinking?’ I said, ‘I want my bag.’ He called the restaurant and said that his girlfriend forgot her bag and we are coming to get it.”

Cousins recalled an uncomfortable Uber ride back to the restaurant: Richter kept saying she was “perfect” for him. After she retrieved her bag from the café, she told the driver to head to Grand Central, where she could take a train home. According to Cousins, Richter instead said he wanted her to stay with him. “It’s too late to take the train,” he told her. “I’d feel much more comfortable if you slept in my guest bedroom and I’ll make you coffee in the morning.” Following her reply of “Absolutely not, Grand Central!” he leaned in and kissed her, she said. She tried to dodge the kiss but could not. “And then I ran away to Grand Central,” she added.

During his 2019 interview, Richter said he did not recall any of the more explicit details of the evening shared by Cousins with the Foundation for Financial Journalism and insisted that he did not try to pressure her to have sex with him, as she alleged. “I don’t cross lines,” he said. “I would never do anything to cross a line. To touch someone — never! It’s just not my nature.”

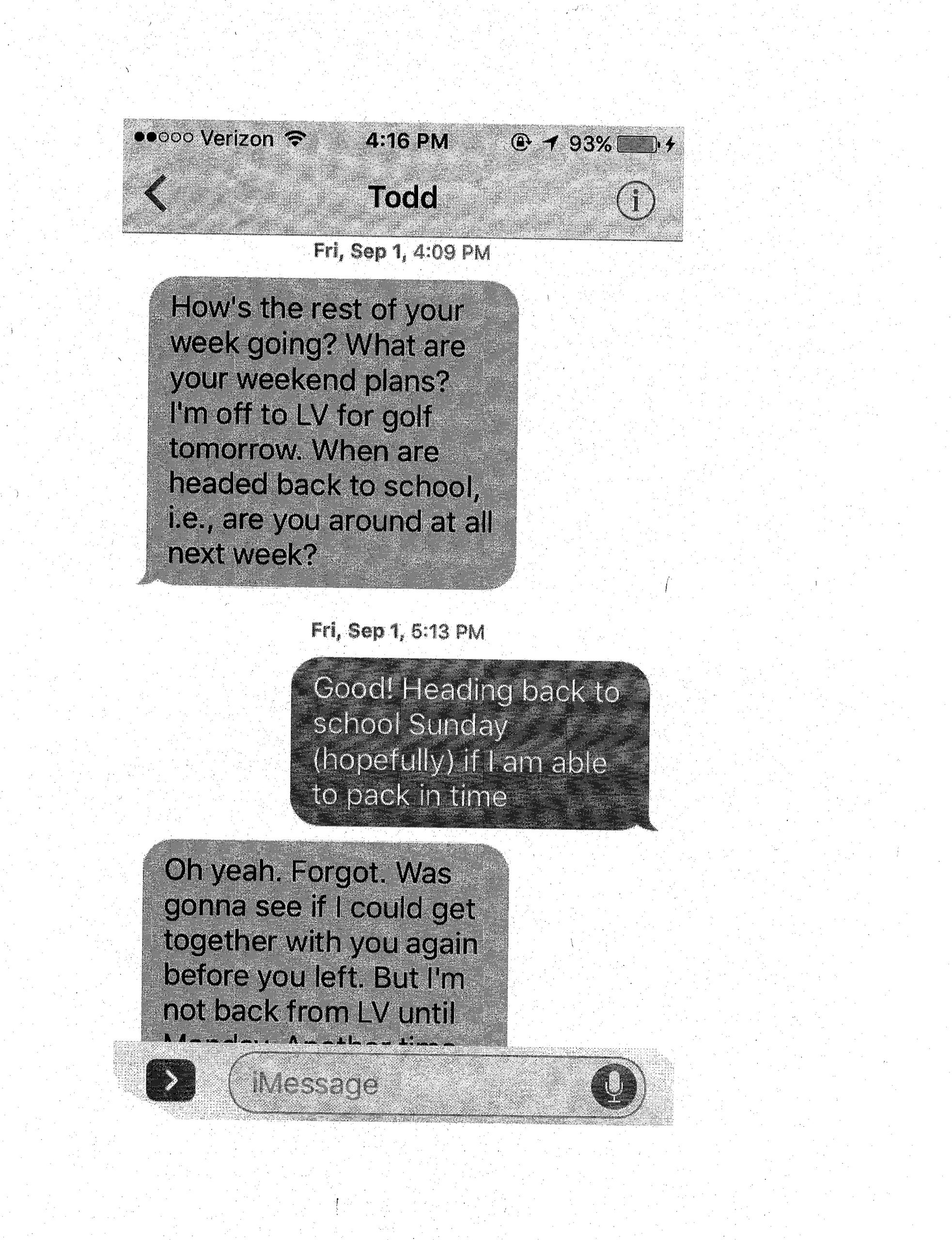

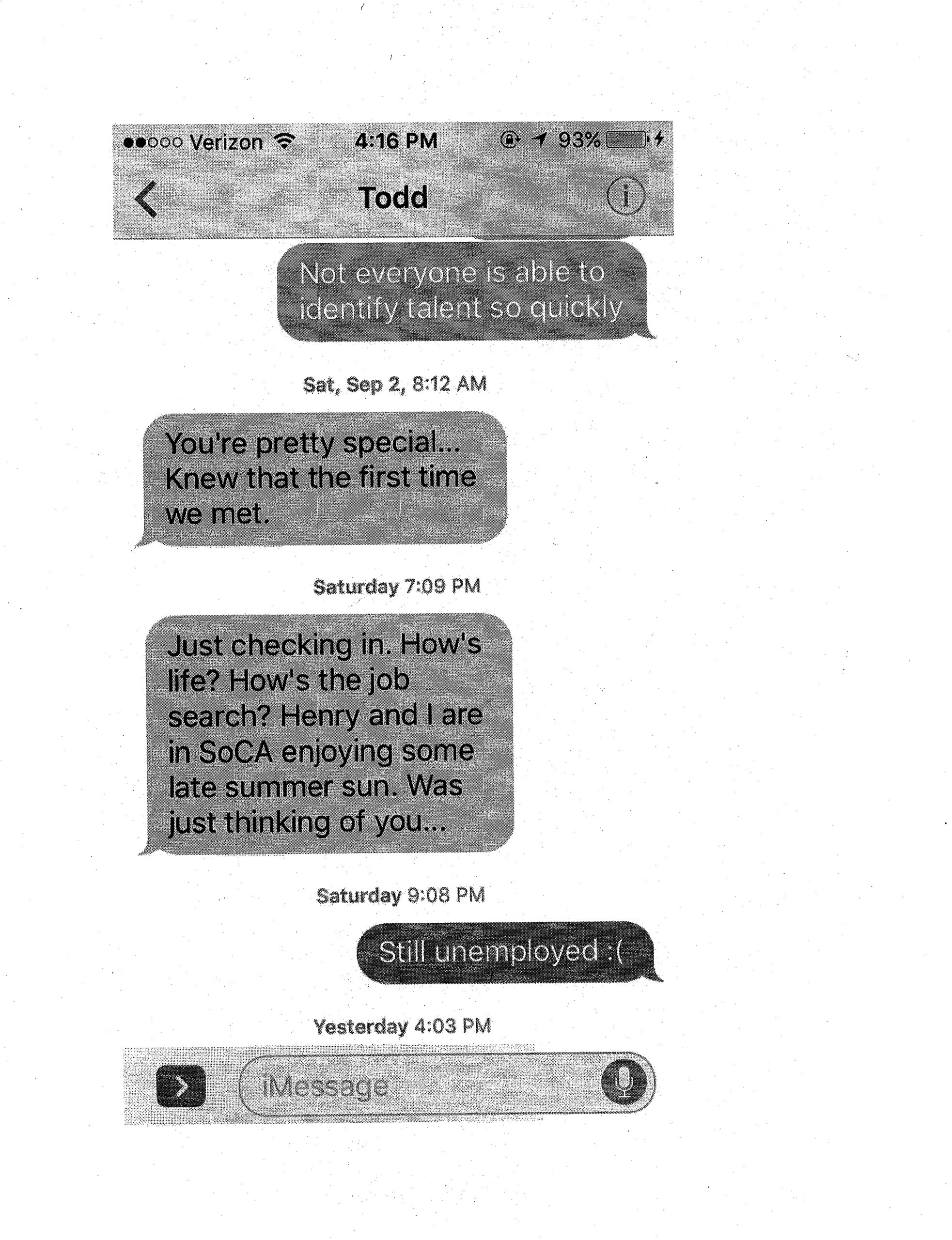

Nevertheless, Richter continued to chase Cousins after that late summer evening, she recalled during her interview. He texted her at 6:31 a.m. the next morning, “Great time,” adding that he was hungover and working from home. He asked about her weekend plans and said he wanted to get together again when he returned from Las Vegas. She wrote back that she still needed to find a job, thinking he might help. “You’re pretty special,” Richter replied. “Knew that the first time we met.”

In early October, Richter texted her again. “Just checking in,” he wrote, according to an archive of their text exchange. “How’s life? How’s the job search? Henry and I are in SoCA enjoying some late summer sun,” he wrote. “Was just thinking about you.”

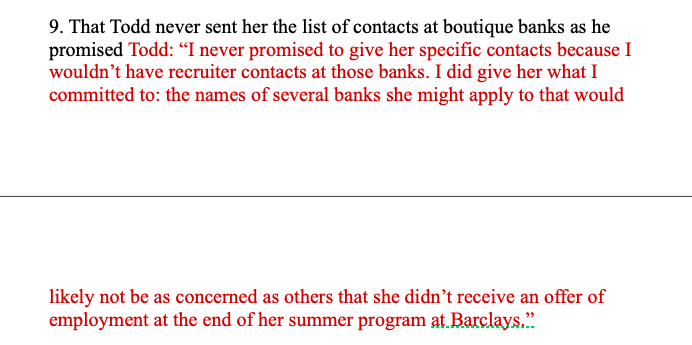

That was their last communication, according to Cousins. And even though Richter had once promised to give her a list of friends and acquaintances at other Wall Street firms, he never did, she noted.

(Richter said last month he did not know the names of recruiters at other firms, so he could not have provided them. But he had kept his word, he insisted, giving her the names of several banks that he felt would not be concerned with her lack of a full-time Barclays offer.)

Later in the fall of 2017, The New York Times and The New Yorker published groundbreaking stories about systemic sexual harassment of women in the workplace; both outlets detailed lengthy allegations against Hollywood mogul Harvey Weinstein. Other exposés carried allegations of sexual assaults by powerful men including Charlie Rose, Les Moonves and Matt Lauer. Although incidents of sexual harassment and assault have been prevalent on Wall Street for decades, the financial industry has yet to have a public reckoning over them: Wall Street’s ample profits, coupled with an unofficial code of silence, make it easy to cover up such unsavory incidents with cash settlements and ironclad nondisclosure agreements.

Cousins was determined to not let that happen with Richter, she recalled.

Weighing the decision to tell her story

In December 2017, after Cousins secured a job offer in a different industry, she reported what Richter had done to Barclays’ human resources department.