Freedom Holding Corp. has some explaining to do.

The financial services firm has quite improbably become one of the fastest growing companies on the planet. It lists its shares on the Nasdaq, is incorporated in Las Vegas, but for all intents and purposes runs its operations mostly in Kazakhstan.

As a December investigation by the Foundation for Financial Journalism showed, Freedom Holding’s ballooning profits have resulted from baffling and opaque business practices that its management is not keen to discuss.

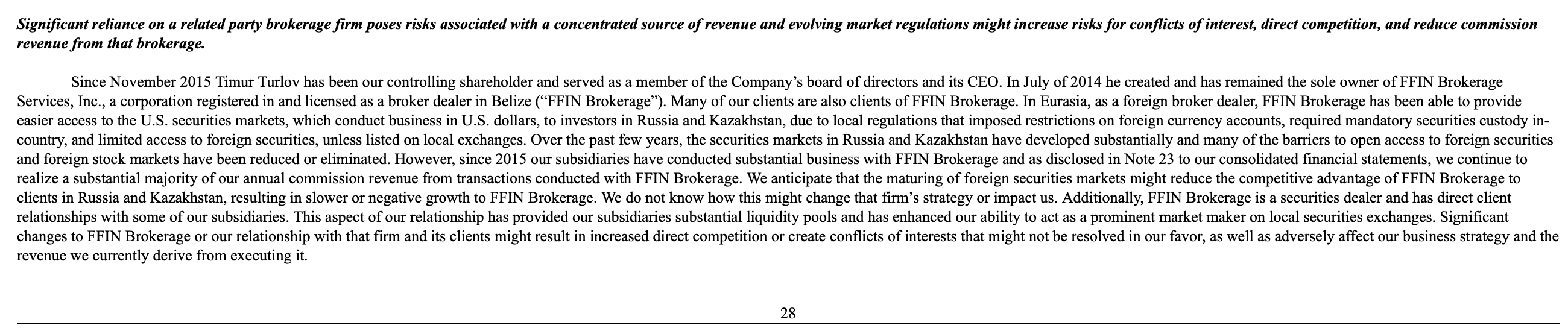

Among the arrangements is Freedom Holding’s close connection to FFIN Brokerage Services, a Belize-based securities trading firm owned by Timur Turlov. He also is Freedom Holding’s billionaire founder and majority shareholder.

{kind=link}

{kind=link}

Even the most seasoned investor has probably not witnessed related-party transactions of the scope of FFIN’s dealings with Freedom Holding.

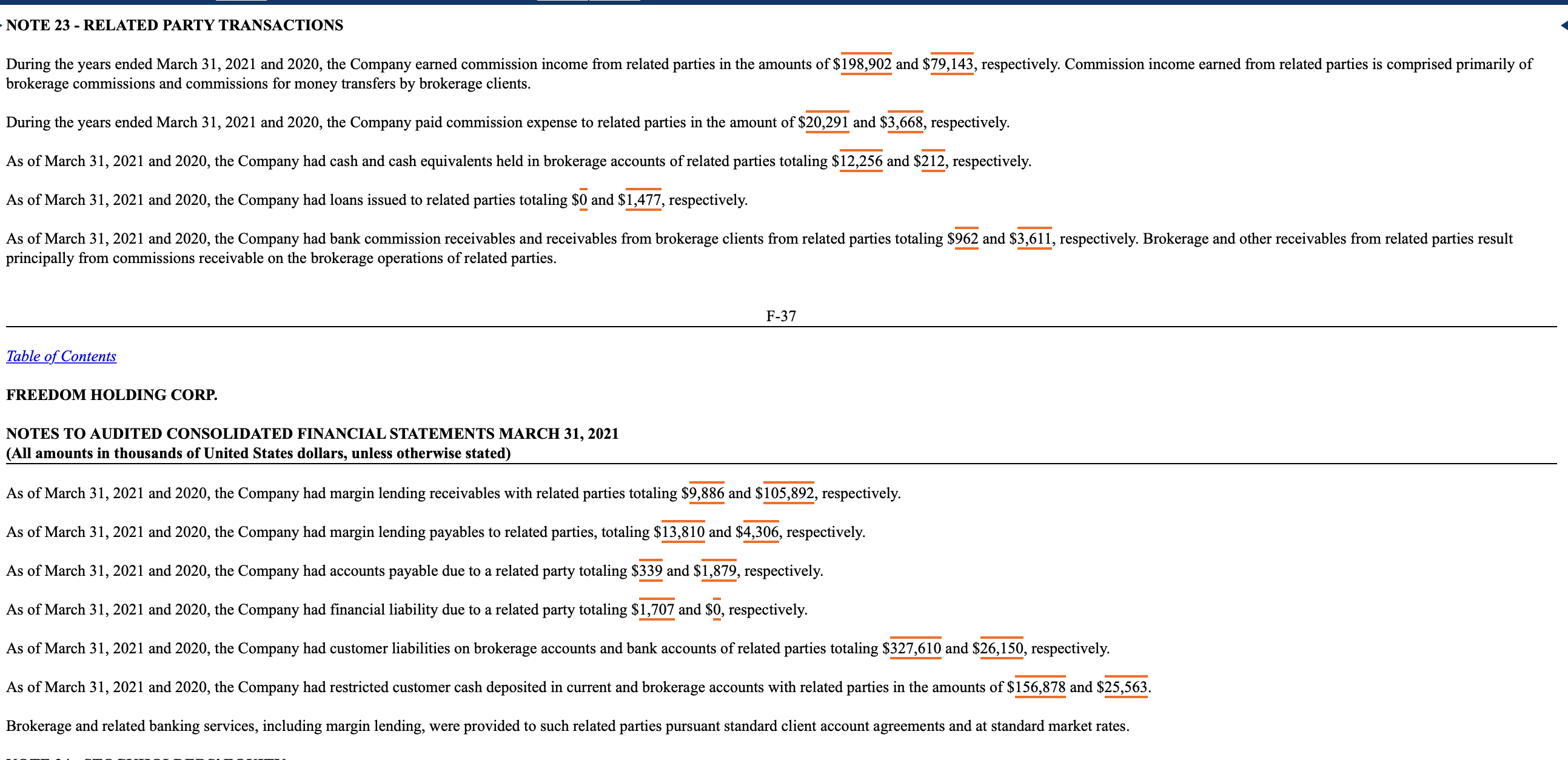

Last year more than 56 percent of Freedom Holding’s revenue came from FFIN commission payments, and in 2019 they represented over 65 percent. What Freedom Holding does to earn the commissions is not readily apparent, however. Yet the two companies are so intertwined – Freedom Holding’s senior managers use FFIN email accounts – it’s not clear the two companies are separate in any real sense.

{kind=link}

{kind=link}

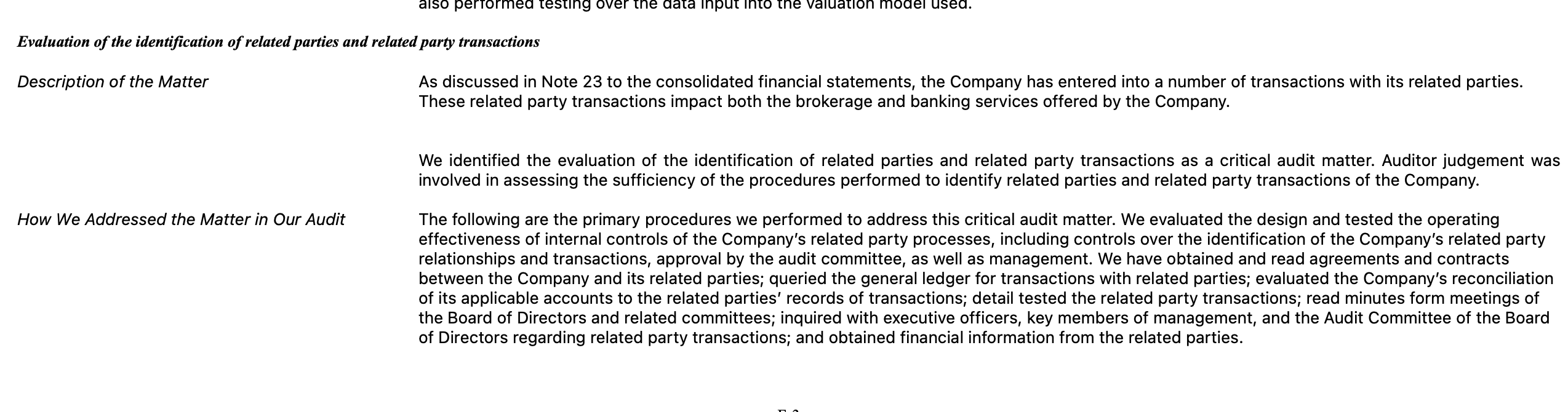

In June, Freedom Holding for the first time disclosed in its annual report its relationship with FFIN, categorizing this as a risk factor for investors to weigh before buying shares. Highlighted as a matter of particular interest: the portion of revenue that Freedom Holding received from Turlov’s company. In the annual report, Freedom Holding’s auditor, Salt Lake City’s WSRP LLC, acknowledged the FFIN connection as part of several “critical audit matters.” (Engaged by Freedom Holding to assess the accuracy of its accounting, WSRP did not weigh in on the propriety of Freedom Holding’s FFIN relationship.)

{kind=link}

{kind=link}

{kind=link}

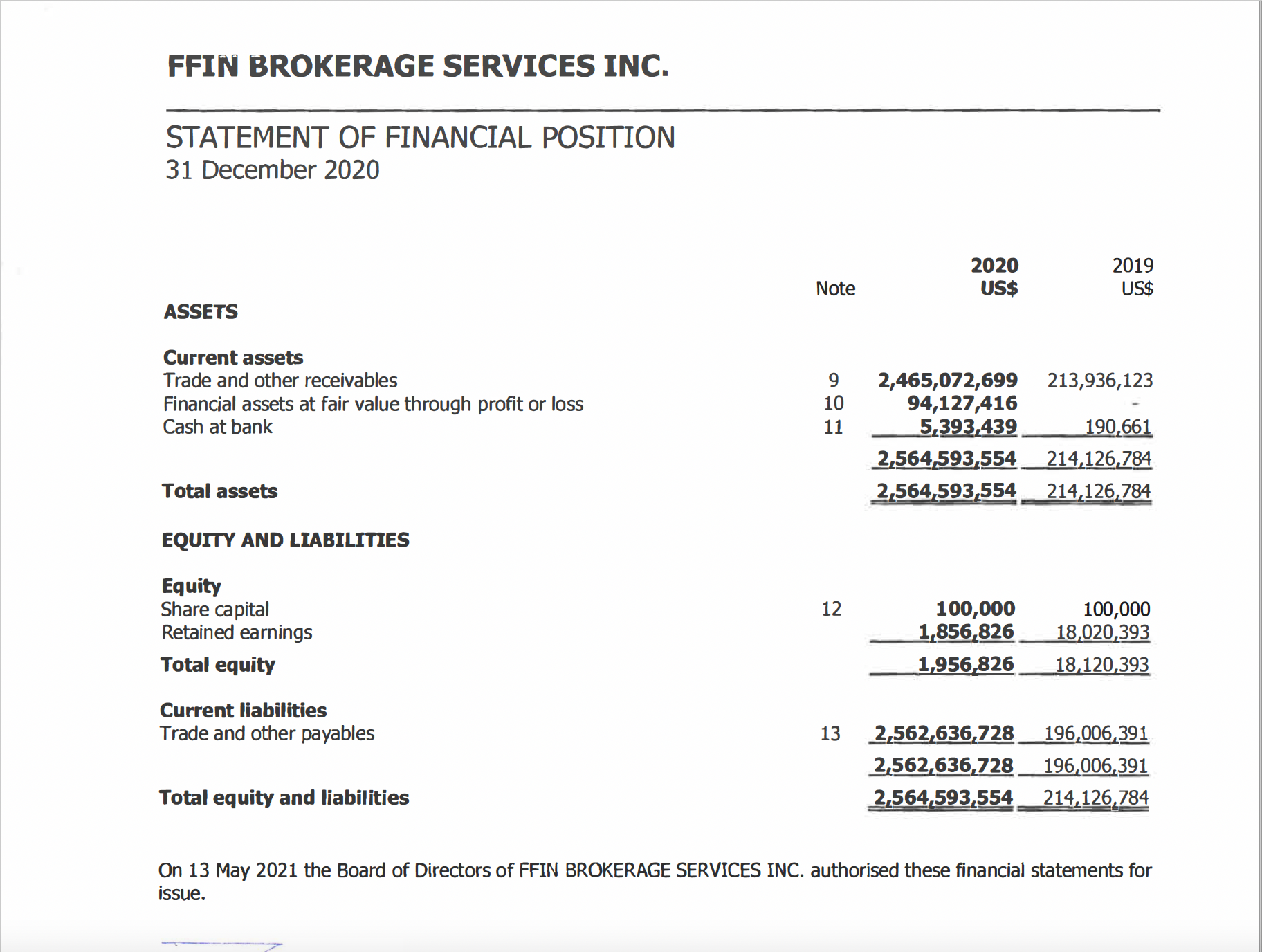

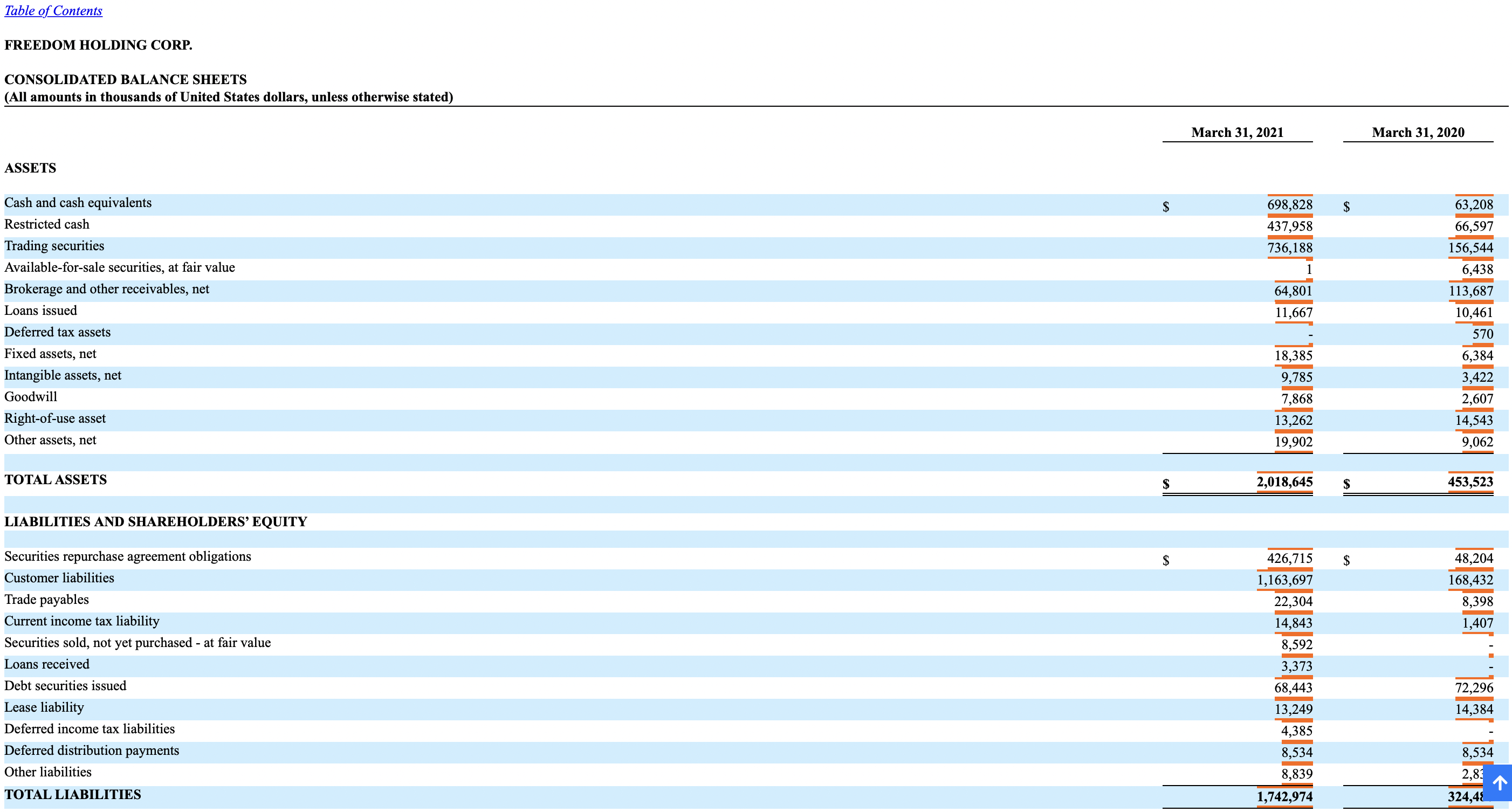

But FFIN’s own annual report, also released in June, ought to give Freedom Holding investors pause: In just a year, FFIN’s assets grew almost 1,100 percent, to more than $2.5 billion. That’s significantly larger than Freedom Holding’s $2 billion in assets.

{kind=link}

{kind=link}

Were FFIN ever to hit dire financial straits, Freedom Holding could be in real trouble.

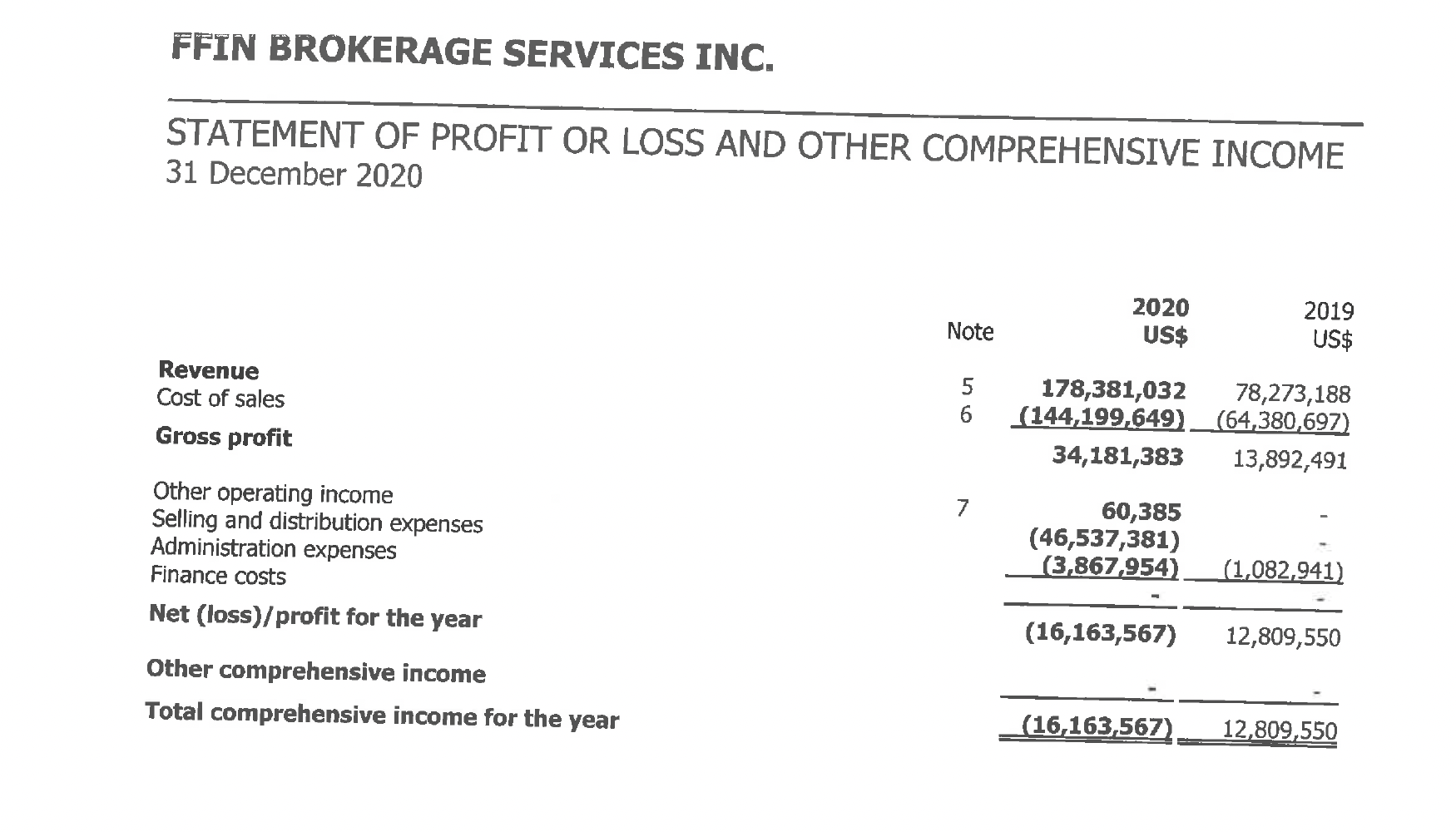

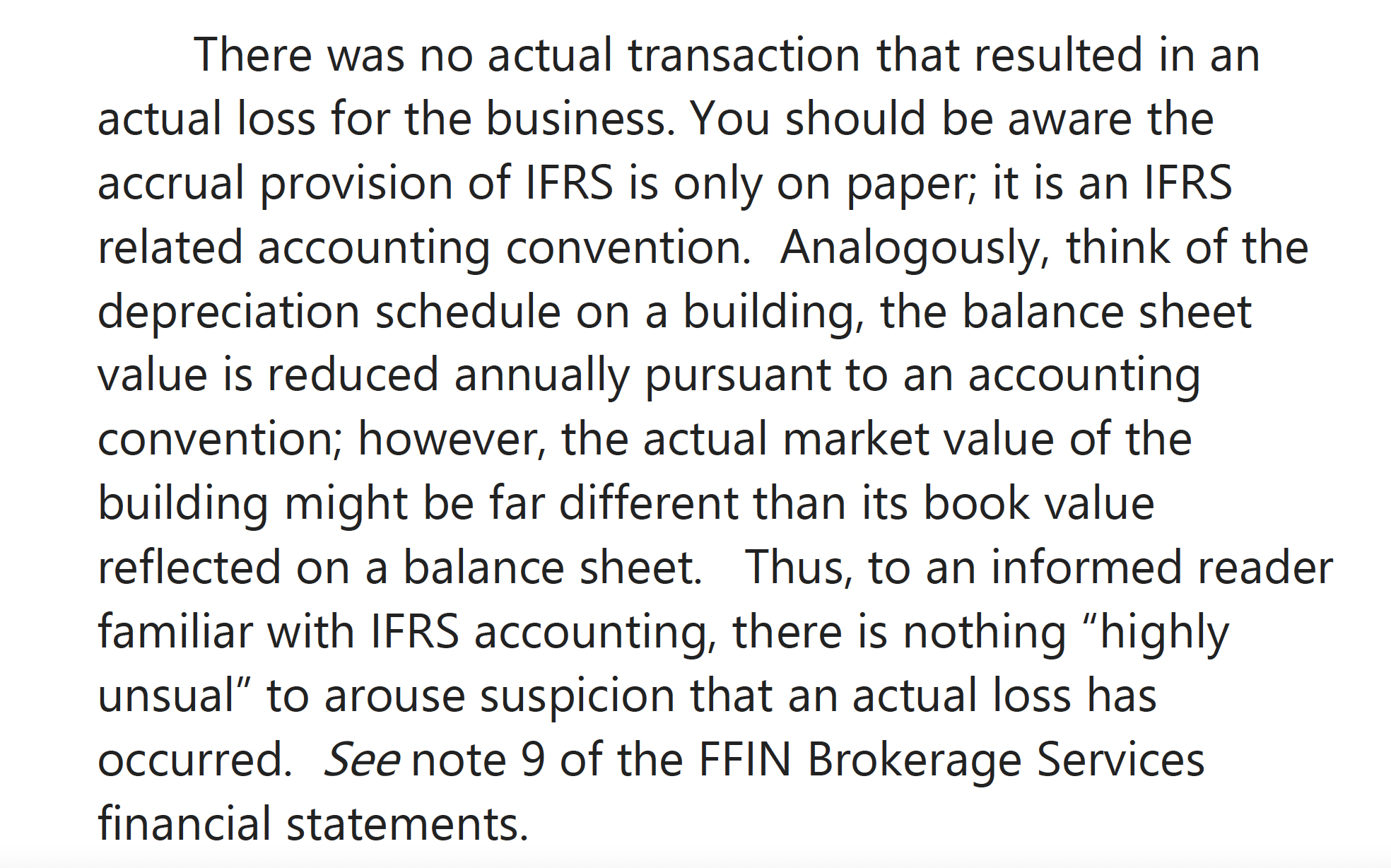

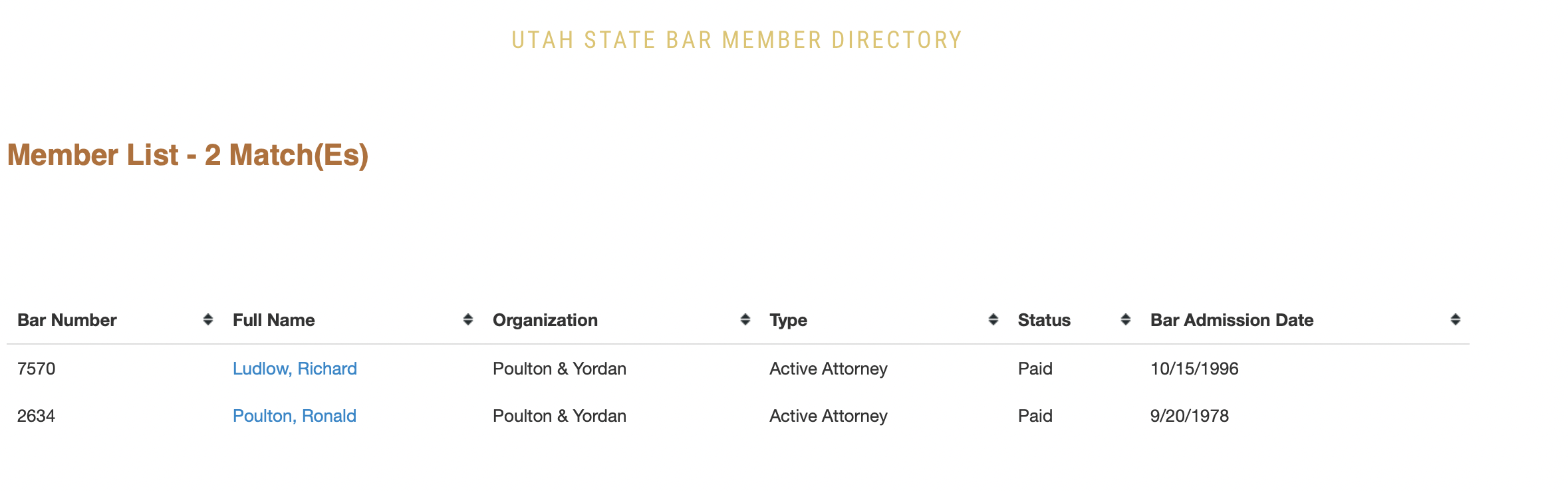

And FFIN’s profits have put substantial cash in Turlov’s pockets: $12.8 million in 2019 and more than $30 million last year. (Although FFIN recorded a $16 million loss last year, Freedom Holding’s outside legal advisor Ron Poulton of Salt Lake City explained that no actual loss occurred. The $46.53 million in impaired trade receivables recorded by FFIN were not losses resulting from clients failing to pay but an “accounting convention” to document a charge like a noncash expense such as depreciation, he said.)

{kind=link}

{kind=link}

Keeping terms of a relationship under wraps

While the specifics of FFIN and Freedom Holding’s arrangement have not been publicly disclosed, the basic contours are clear: FFIN acts as a broker for Freedom Holding, primarily executing trades in popular U.S. exchange-listed equities and initial public offerings.

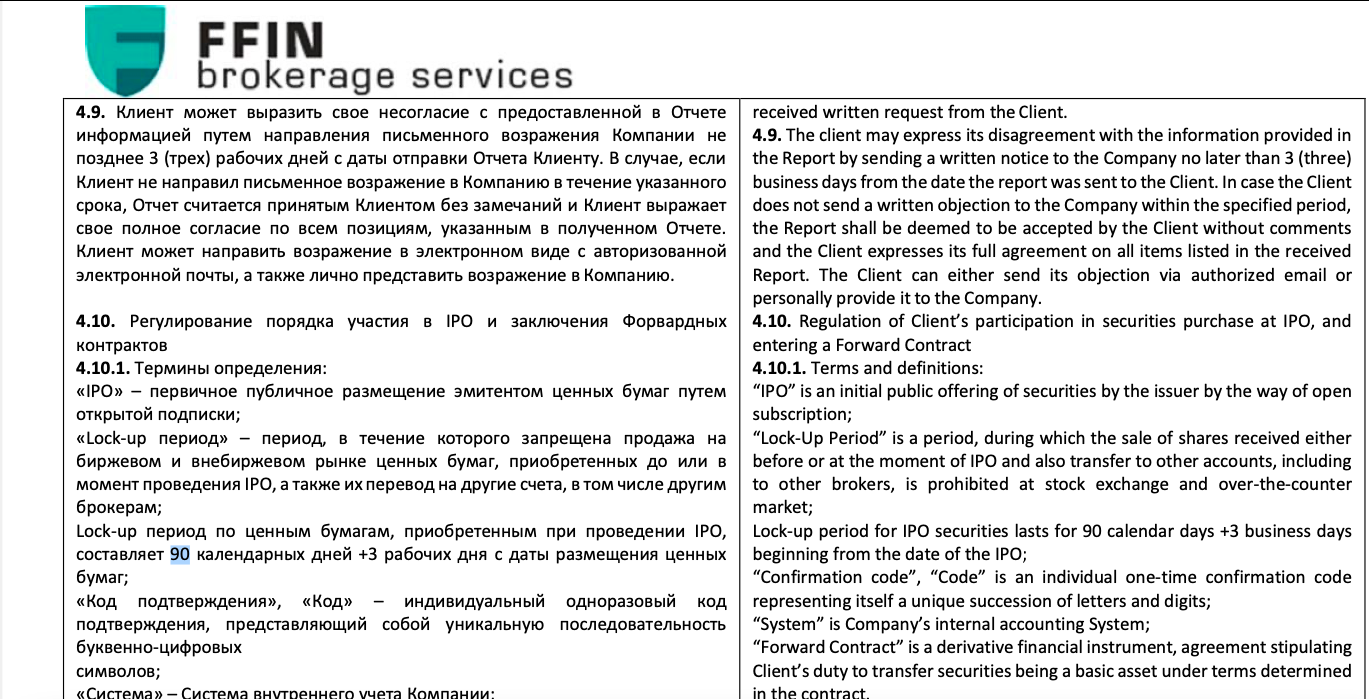

Peddling IPOs is Freedom Holding’s most aggressively promoted line of business, and FFIN handles the firm’s IPO-related customer service issues. For its part, FFIN has a distinctive business practice: requiring clients to observe a 93-day lockup period for any IPO shares they purchase. Customers cannot sell or even transfer to an outside account the newly purchased shares for that three month period.

{kind=link}

{kind=link}

This is starkly at odds with the typical U.S. and European brokerage practice, whereby clients are free to trade their shares immediately after receiving an allocation. Any other brokerage that tried to impose this constraint would likely be assured of an immediate customer exodus and a wave of litigation.

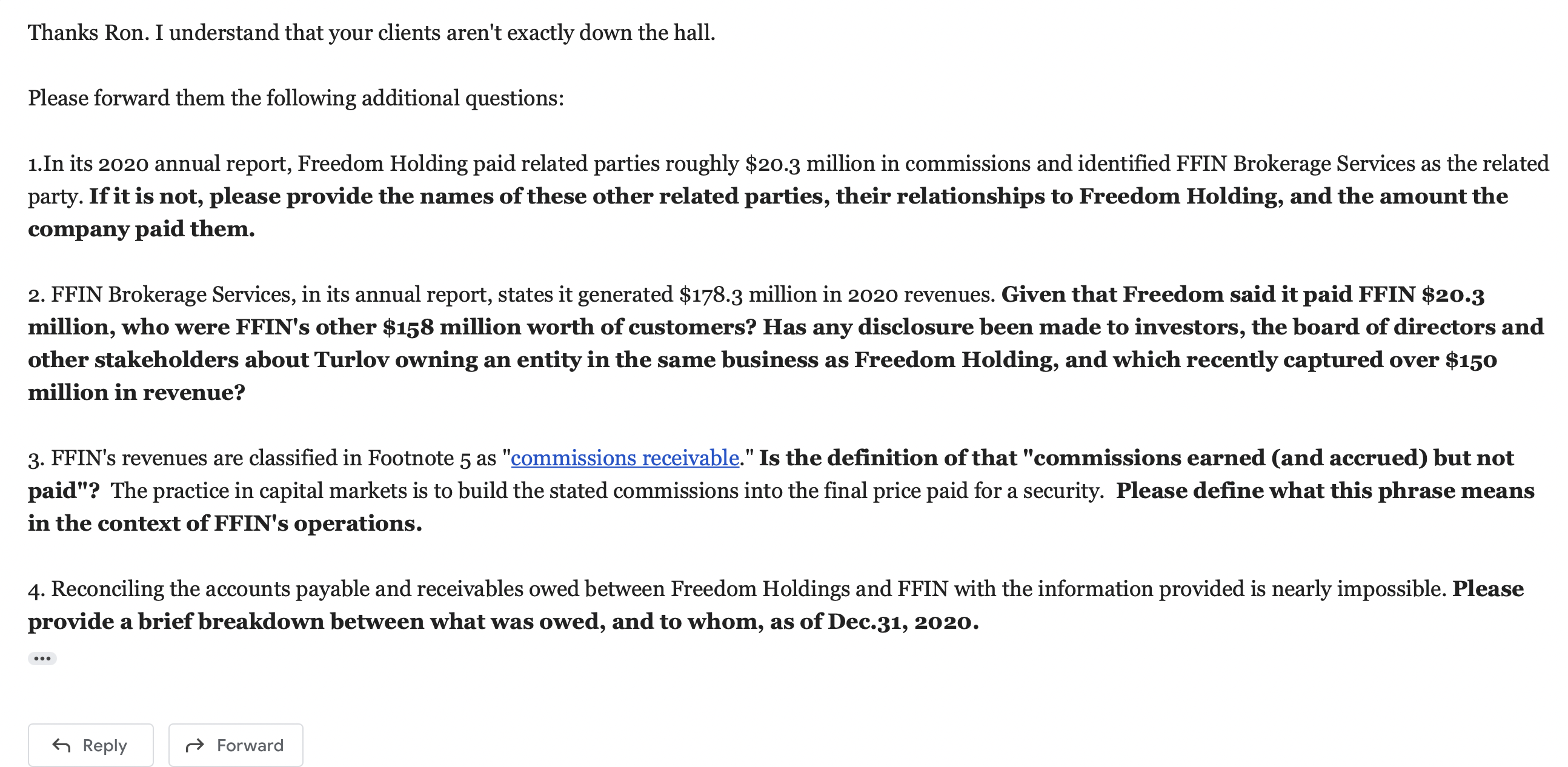

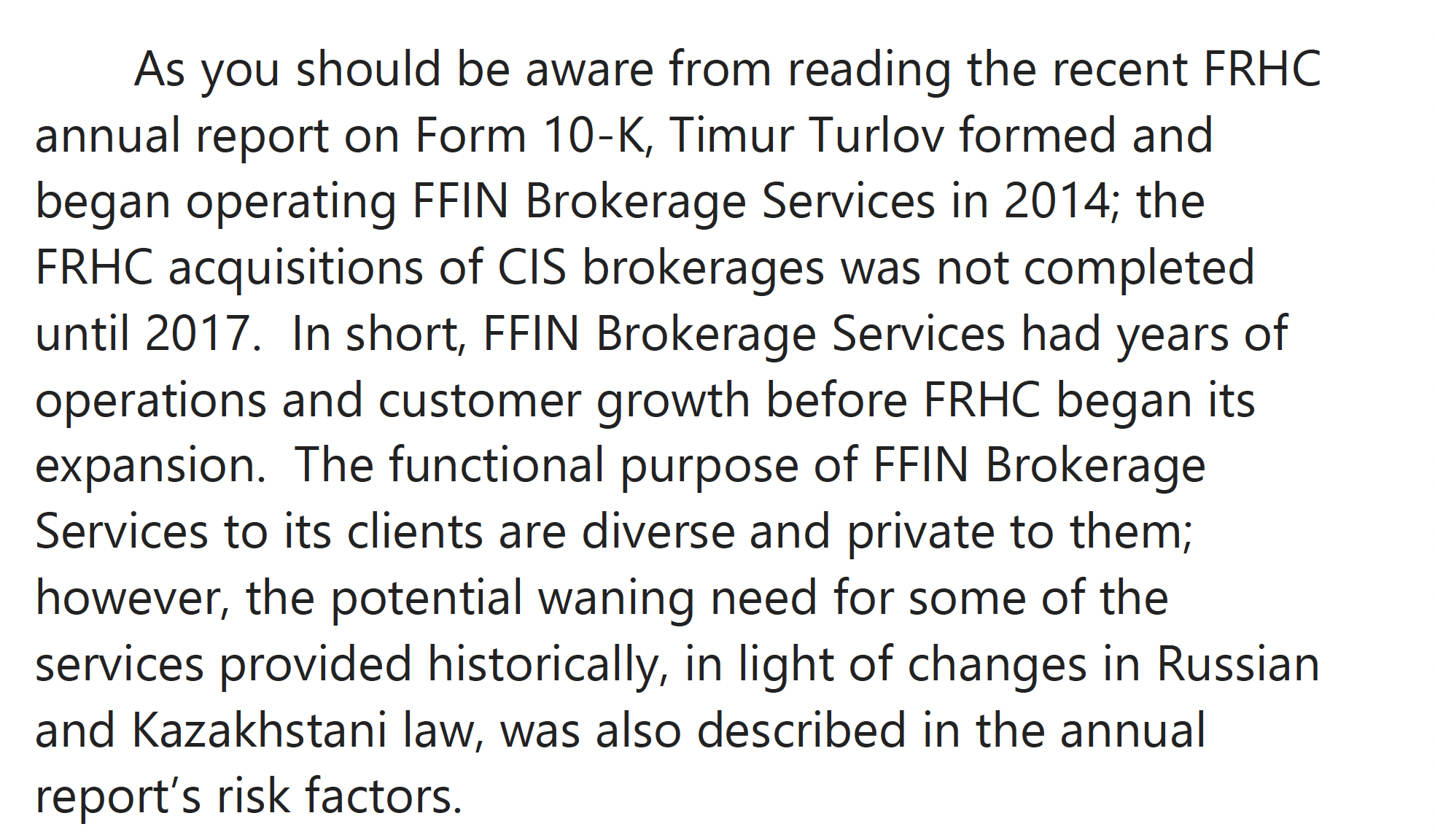

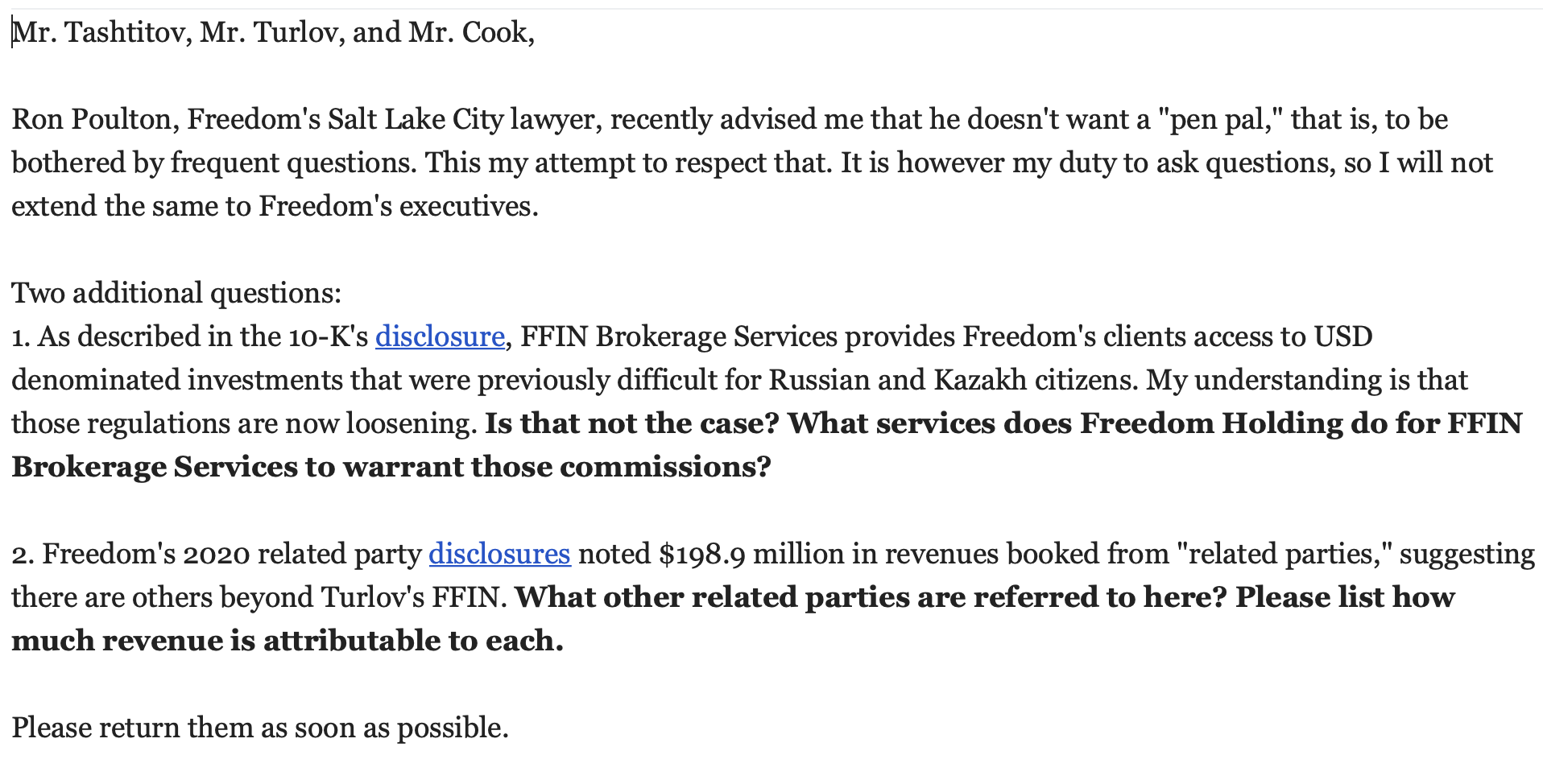

The Foundation for Financial Journalism asked Poulton several questions about the particulars of the Freedom Holding-FFIN relationship. (Poulton addressed one group of questions but refused to answer a second, more specific set.) He would speak only generally about FFIN, saying, “The functional purpose of FFIN Brokerage Services to its clients are diverse and private to them.”

{kind=link}

{kind=link}

{kind=link}

Poulton also cited changes in Russian and Kazakh laws that might reduce Freedom Holding’s reliance on FFIN. Turlov set up FFIN in 2014 to offer Russian and Kazakh residents access to U.S. dollar-denominated investments, Poulton said. At the time, Russian regulators frowned on individuals owning British pound- and U.S. dollar-denominated investments. In 2018, however, the two countries started to ease such regulations.

The Foundation for Financial Journalism posed the same questions to Adam Cook, Freedom Holding’s corporate secretary; Askar Tashtitov, Freedom Holding’s president; and Turlov but did not receive a reply.

{kind=link}

{kind=link}

Generating huge profits via a small Cyprus unit

Notwithstanding the steady skyward march of Freedom Holding’s share price, its financial statements are surely catnip for short sellers and financial skeptics.

Embedded in the filings is the prominent role Freedom Holding’s Cyprus unit plays in the company’s growth. That subsidiary, which used to be the prime component of Freedom Finance Europe Limited, has been formally renamed Freedom Finance Europe Limited; the unit opened in 2017 and its main task is operating Freedom 24, an electronic trading system.

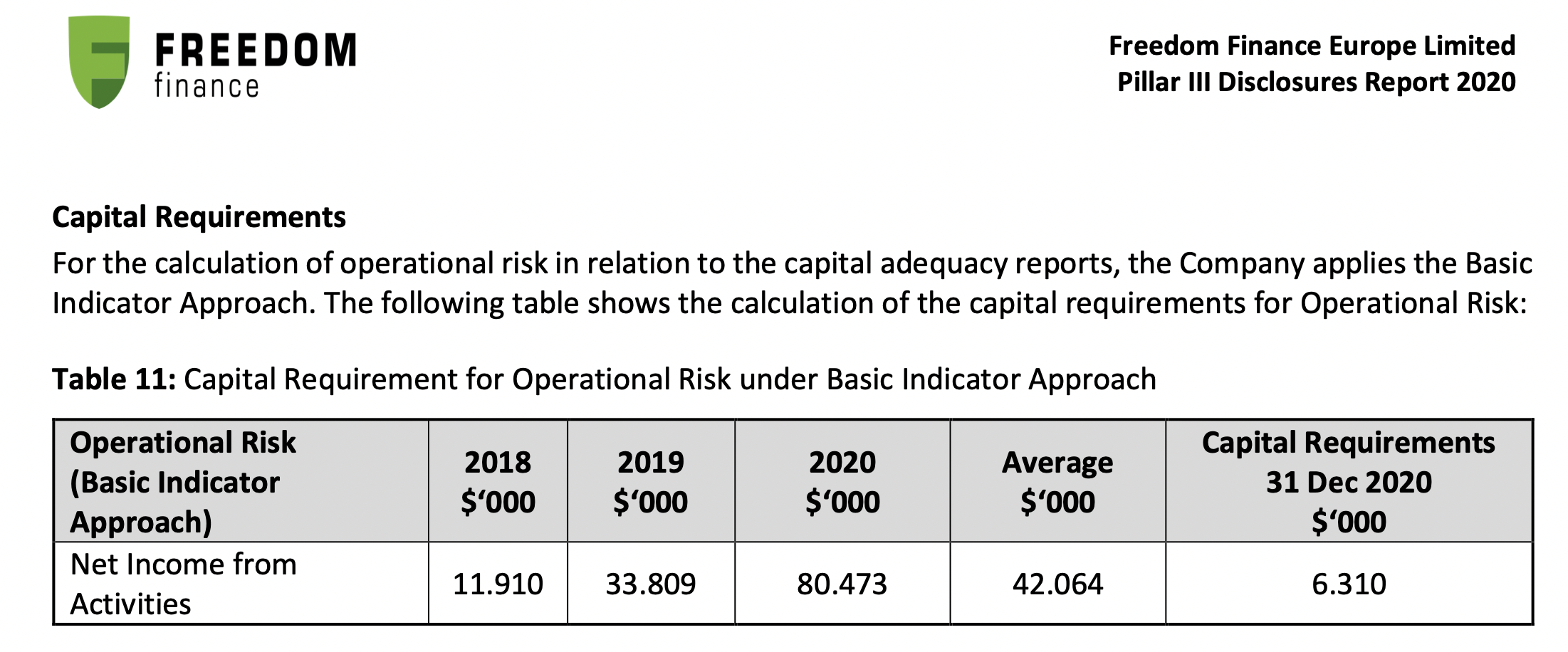

As described in the December article, the Cyprus subsidiary’s defining feature is achieving astronomical profit growth, unrivaled on Wall Street. Although in 2017 the Cyprus unit reported a $30,000 loss, by 2019 it had $33.8 million in earnings. In 2020, the subsidiary’s income rose to $80.4 million.

{kind=link}

Freedom Holding’s earnings growth story is entirely a function of its Cyprus subsidiary. One way to track this is to compare the published financial results for both Freedom Holding and its Cyprus subsidiary from Jan. 1, 2020, through Dec. 31, 2020. (The Cyprus unit files a risk disclosure statement once a year that includes its annual net income, but corporate parent Freedom Holding releases its income quarterly and its fiscal year ends on March 31.)

For the nine months that ended Dec. 31, 2020, Freedom Holding reported $90.1 million in net income, with $80.4 million of this derived from the Cyprus subsidiary.

{kind=link}

Thus, for nine months of Freedom Holding’s most recent fiscal year, the Cyprus unit contributed at least 56 percent of the parent company’s $142.9 million in net income.

{kind=link}

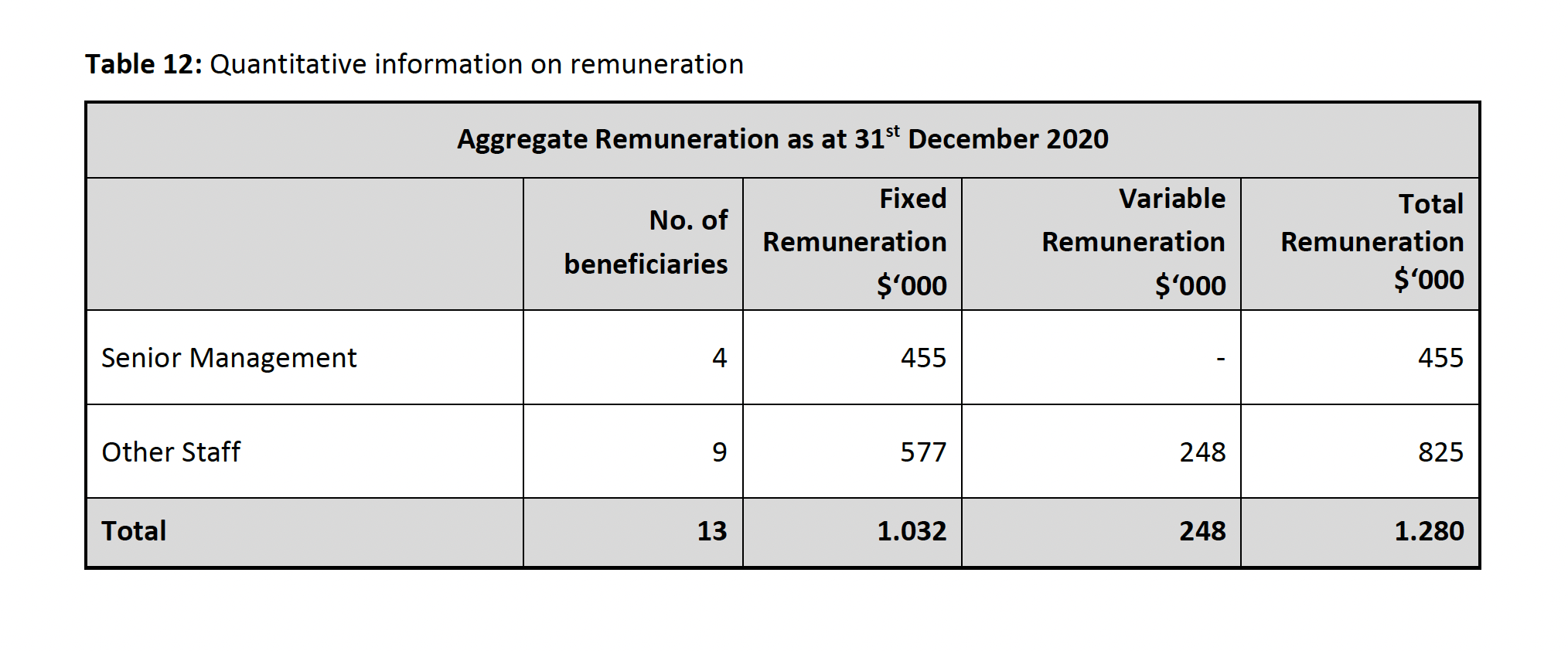

And according to a recent regulatory filing, the Cyprus subsidiary achieved those results with minimal resources. Making that sum of money took only 13 employees and $6.3 million in capital.

{kind=link}

Taken at face value, the Cyprus unit’s gaudy performance likely catapults it to the top of the list of the most profitable trading desks in history. (The distant second: Michael Milken’s high-yield trading operation at Drexel Burnham Lambert, which in 1987 generated a purported $2 billion in revenue, with Milken pocketing an estimated $550 million.)

To an outside observer, the fact that the Cyprus unit could generate profits at this scale is baffling. After all, it is a no-frills online trading operation that facilitates individual investors’ stock trades. It definitely is not an elite proprietary trading division; compensation for its 13 employees last year totaled less than $1.3 million.

Carrying out trades in a circuitous fashion

Freedom Holding employs a remarkably circuitous order execution process for its customer’s trades. It is labyrinth to a degree that suggests that obtaining the best possible price for the client is a secondary concern.

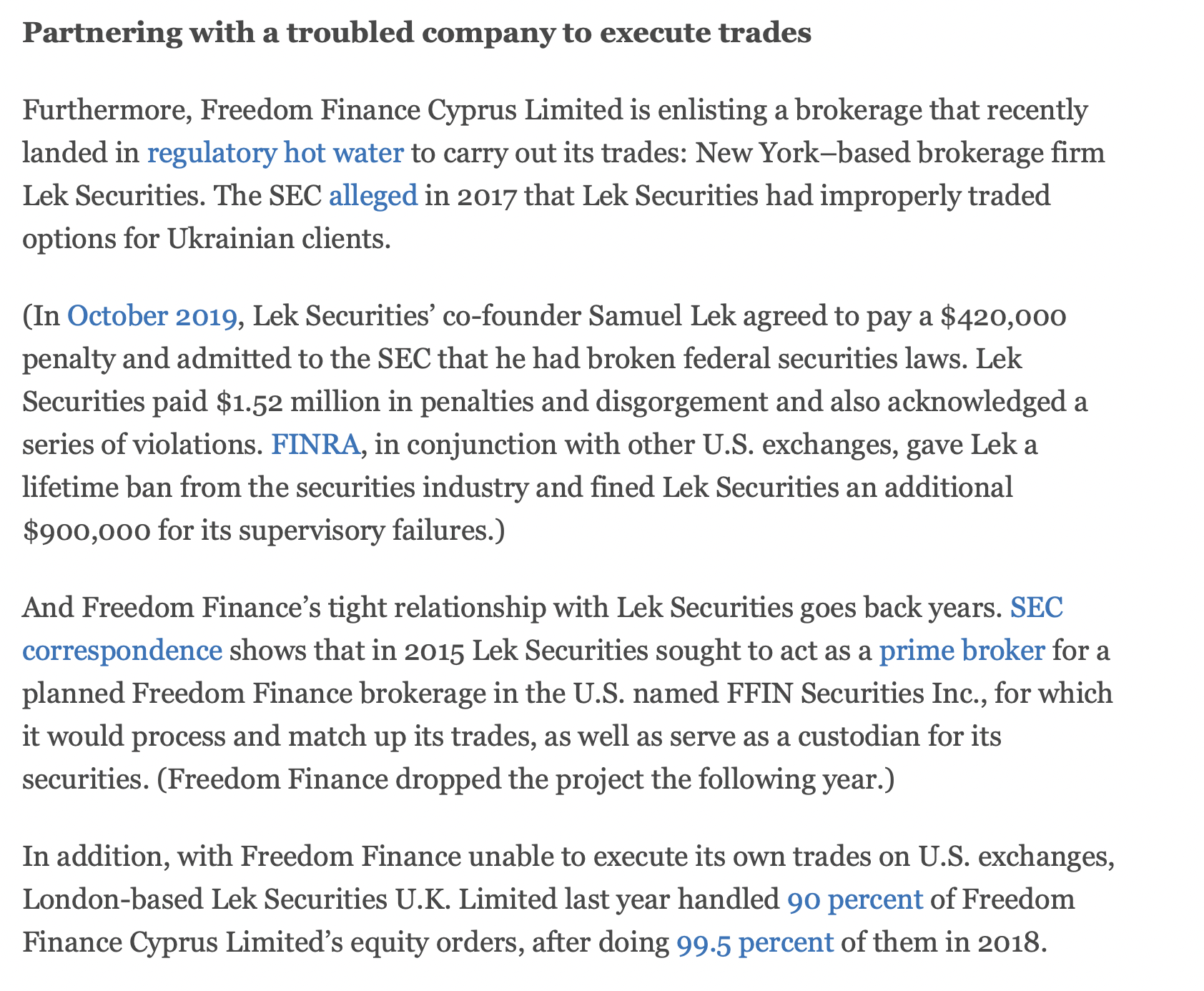

A transaction might look something like this, according to conversations with current and former Freedom Holding clients, as well as a former company executive: A client of Freedom Holding who attempts to buy shares online is promptly directed outside its platform to FFIN, which then routes the order to Freedom Finance Europe in Cyprus. But final execution of the client’s order appears to require another handoff, either to a Freedom Holding subsidiary in Moscow or (frequently) to a firm with a troubling regulatory history, Lek Securities U.K. Limited in London.

{kind=link}

One possible reason for this complexity? Fee layering, the practice of charging a client multiple fees on a single transaction.

Layering is a legal, albeit controversial, practice that has fallen out of favor in the U.S. money management industry, given the rise of lower-cost index and exchange-traded fund investing. But for Turlov and his colleagues, elongating a trade’s life cycle in order to collect two or three sets of fees might be tempting since their largely Russian and Kazakh client base might have scant experience with Wall Street practices or robust consumer advocacy.

A further puzzle: The Cyprus unit’s 2020 risk disclosure statement noted that last year FFIN executed 24 percent of the trades made by the unit, up from 9 percent in 2019. This is odd since neither FFIN nor the Cyprus subsidiary hold any U.S. brokerage licenses.

{kind=link}

{kind=link}

Doing business with companies of questionable repute

One of the nicer things about managing an expanding and profitable company is having options. For example, if a customer poses a reputation risk or is too demanding relative to his or her economic value, ending the relationship is generally a low-risk proposition.

Timur Turlov and his managers do not seem to hold this view, however, because they have regularly done business with people and companies whose extensive legal problems would cause most U.S.-based managers to stop in their tracks.

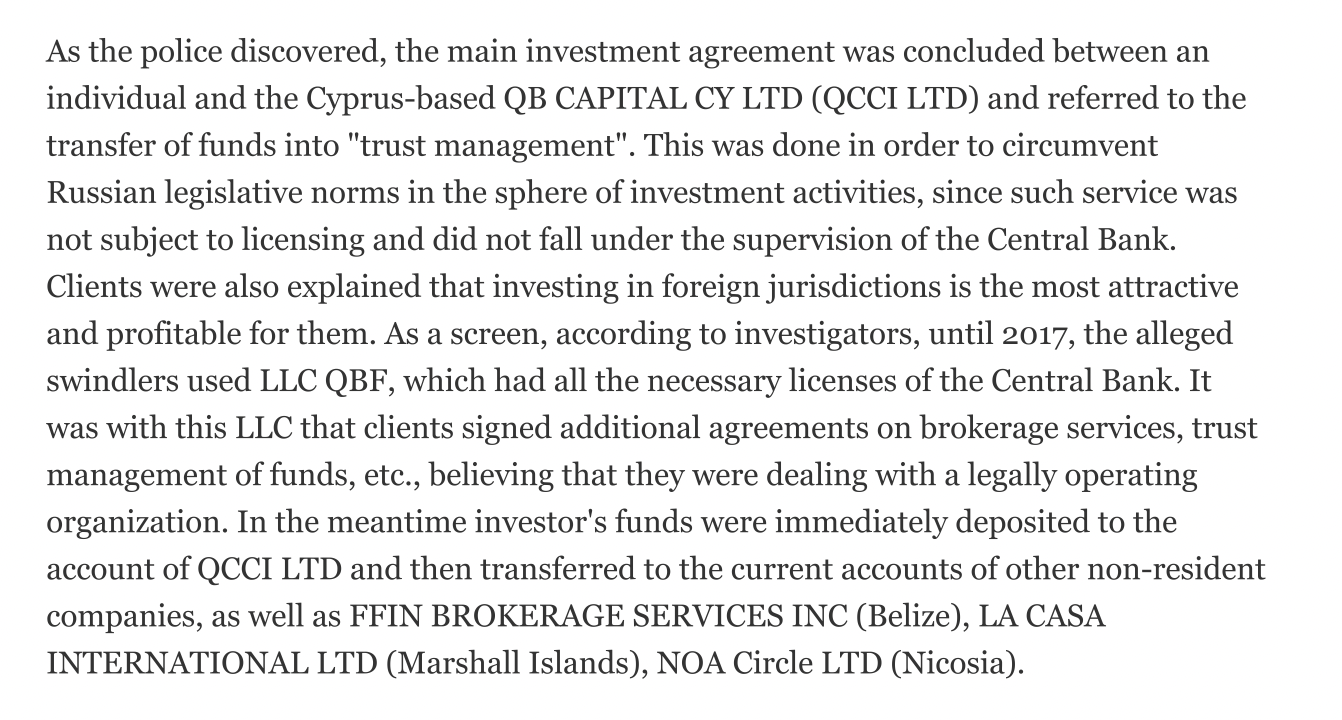

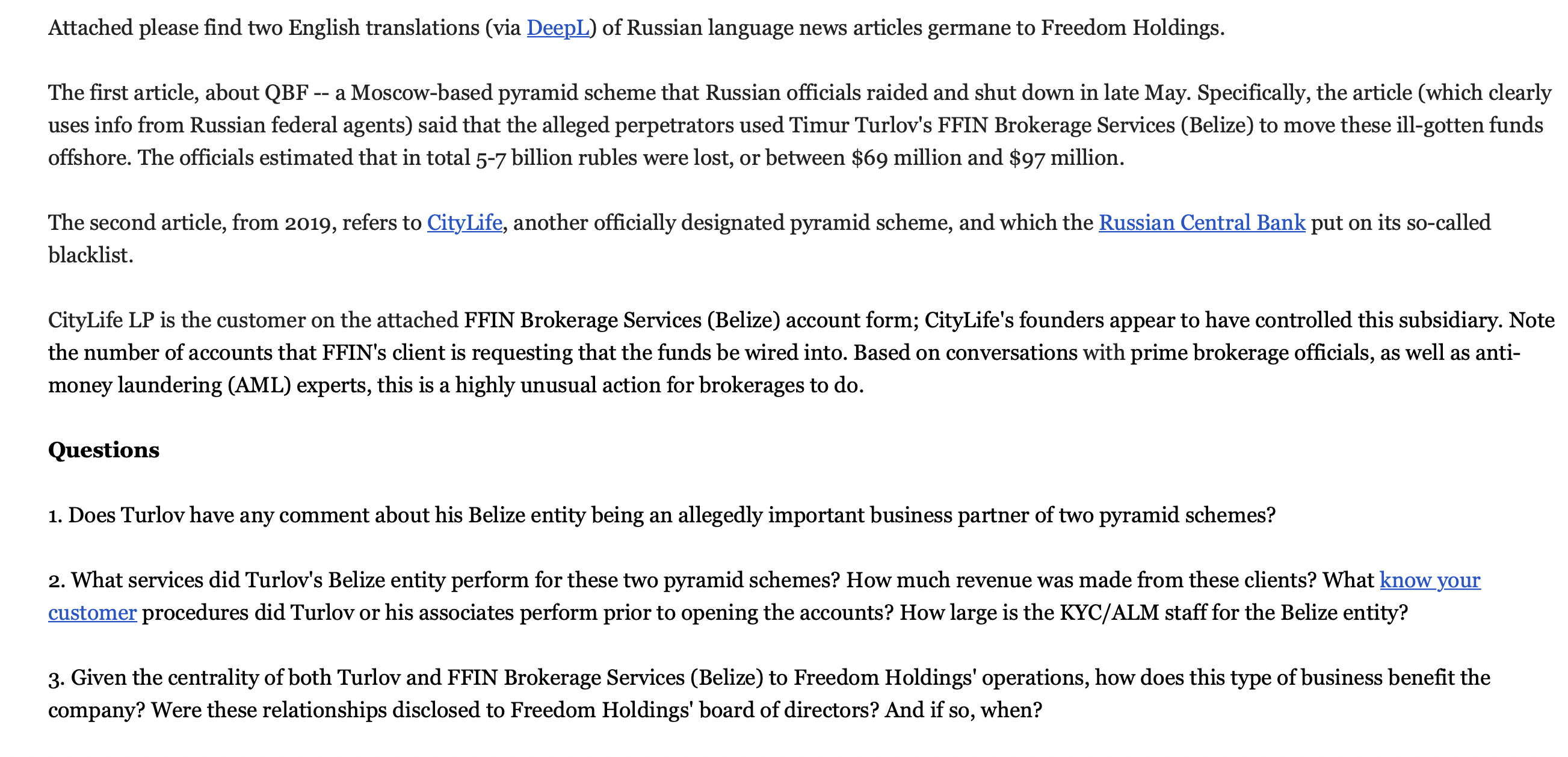

Consider FFIN’s business relationship with two Moscow-based companies: asset manager QBF LLC and network marketer CityLife.

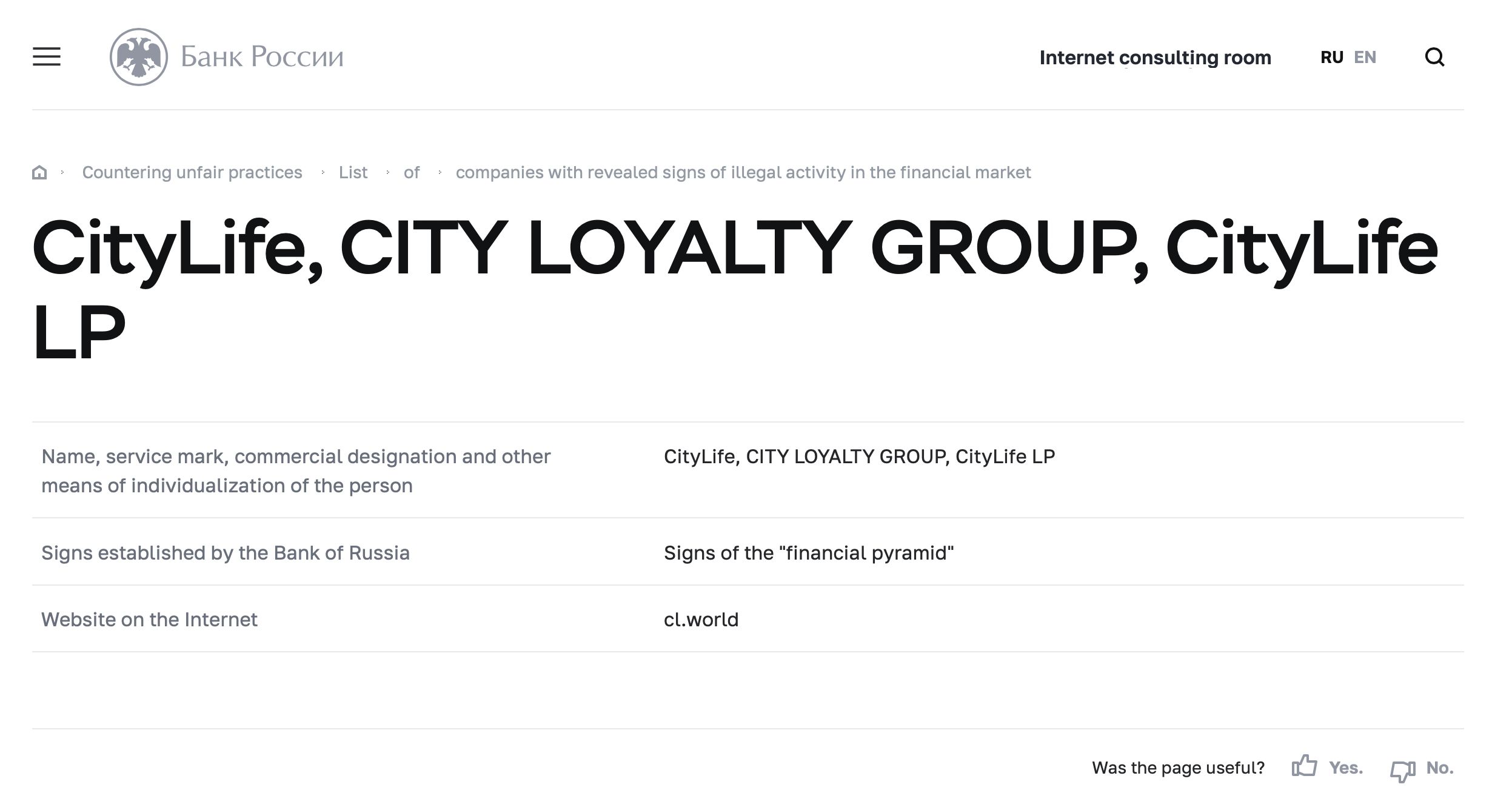

Both QBF and CityLife have attracted the scrutiny of the Russian government: The Ministry of Internal Affairs raided QBF on May 31 and arrested two of its principals for purportedly conducting a Ponzi scheme. And on June 1, the Central Bank of Russia’s Unfair Trade Practices unit added CityLife to a list of companies with identified signs of illegal activity for allegedly showing signs of running a pyramid scheme.

{kind=link}

How does FFIN fit into all this? According to a translation of a Russian language press account of the Interior Ministry’s QBF raid, FFIN was one of several banks and brokerages the asset manager’s executives were said to have used to move investor cash out of Russia. (Neither Turlov nor Freedom Holding were named in the article.)

{kind=link}

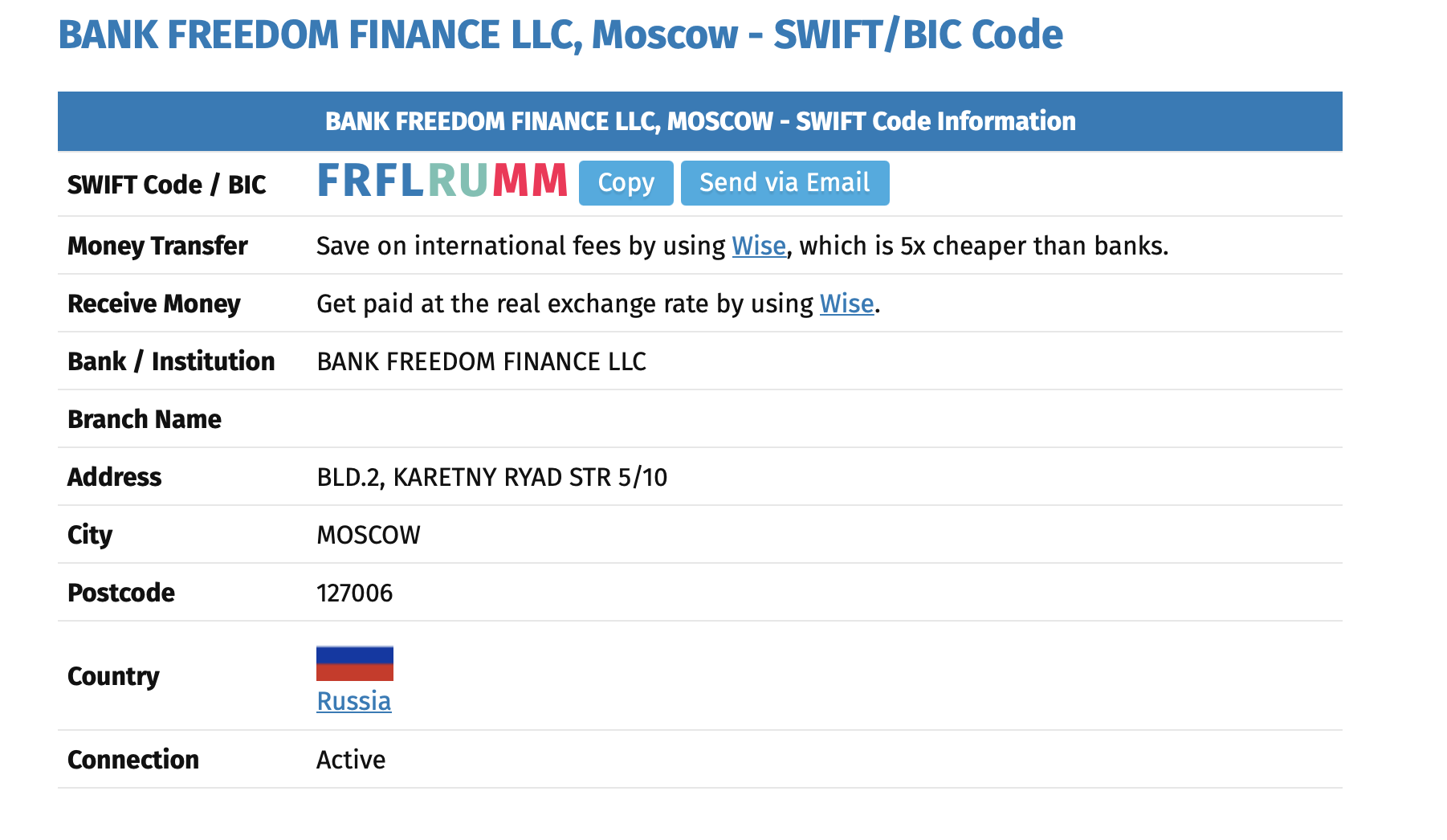

While using a Russian language search engine, the Foundation for Financial Journalism found a CityLife co-founder’s FFIN wire instructions designating 16 separate bank accounts that were to receive funds. It is not clear who posted such a sensitive document online, but the root link is from a CityLife website. One of the banks listed on the form is Freedom Holding’s Bank Freedom Finance LLC.

{kind=link}

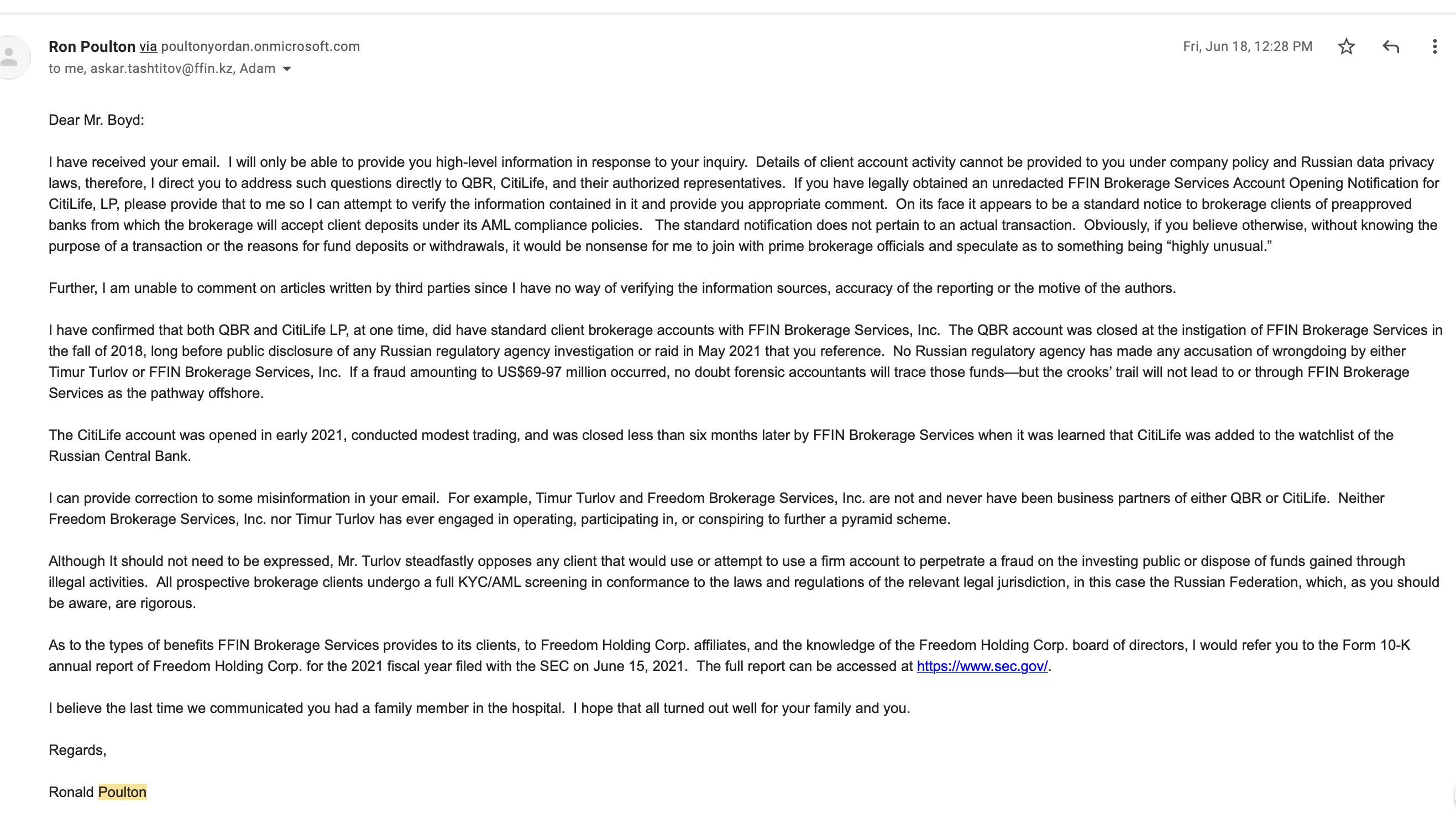

Questioned about FFIN’s relationship with QBF and CityLife, Poulton confirmed that the two firms “at one time did have standard client brokerage accounts with FFIN Brokerage Services.” He said that FFIN closed the QBF account “in the fall of 2018” but did not provide a reason.

{kind=link}

{kind=link}

Poulton added that the CityLife account was opened in early 2021 and “conducted modest trading” and when the Central Bank of Russia added it to its list of companies with identified signs of illegal activity, FFIN closed the account.

{kind=link}

Update: This story was updated on Aug. 8, 2021, to clarify the relationship of the Cyprus unit to Freedom Holding’s Freedom Finance Europe; it used to be referred to as its subsidiary but now is simply called Freedom Finance Europe.