Derrick Snowdy is probably as close to a celebrity as Canada’s private investigator community has.

Starting in 2010, Snowdy burst into view as a prime mover in the political controversy colloquially known as “the busty hookers’ scandal.”

Snowdy proved to be a quick study at capturing an audience’s attention, ever ready to regale listeners with some of the inside stories from his investigations.

So when Catalyst Capital founder Newton Glassman brought a stemwinder of a defamation litigation in 2017 against a host of hedge fund managers and journalists, it was not surprising to see Snowdy involved.

(Foundation for Financial Journalism readers will recall our two 2018 investigations that looked into the quality of disclosures at Callidus Capital and Catalyst Capital, the two investment vehicles Glassman controlled. In July 2019 Catalyst amended the initial defamation claim to add Bruce Livesey, the article’s co-author, as a defendant.)

After all, given the numerous well-heeled defendants — and their lawyers, many sporting big litigation budgets — the prospects for an investigator with a knack for digging into corporate fraud seemed attractive.

There was just one thing.

A series of filings were unsealed late last week in Catalyst’s litigation revealed that Snowdy had indeed been hard at work on these types of issues for several years. (The filings were made by West Face Capital and the other defendants.)

But it had been for the other side.

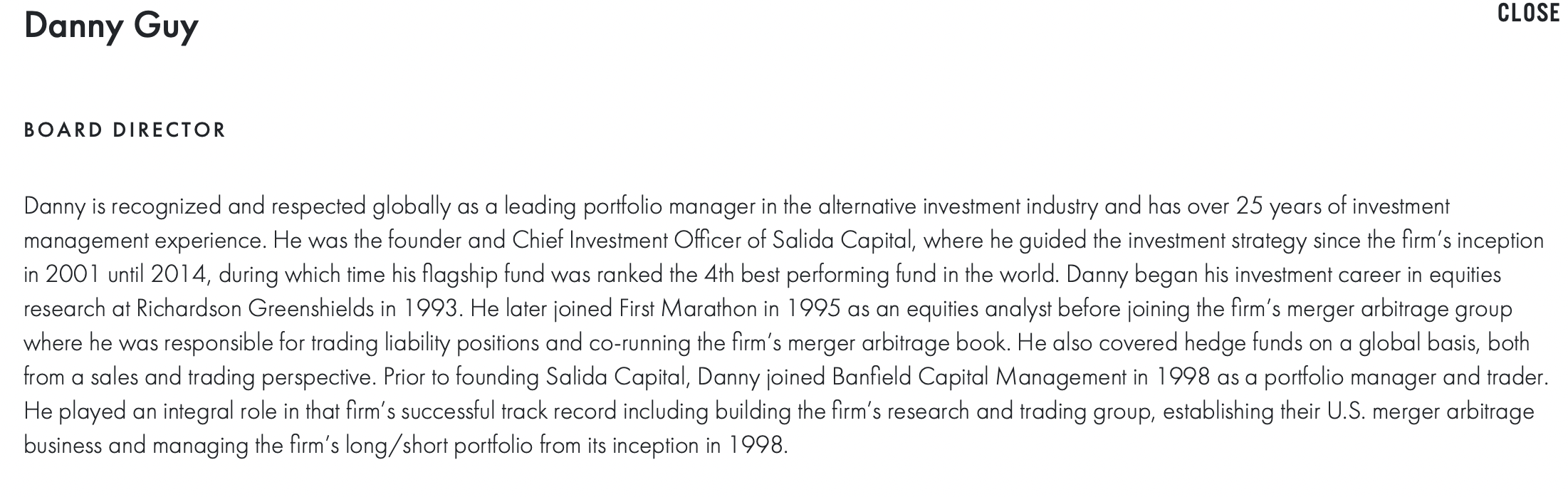

So who bankrolled Snowdy’s efforts? A single client: Danny Guy, a veteran Canadian money manager and the general partner of Harrington Global Opportunities Fund.

{kind=link}

{kind=link}

Meet Danny Guy

Little about the arc of Daniel Gerrison Guy’s career in finance would imply a disposition towards garish conspiracy theories.

After starting in brokerage research in 1993, Guy joined Banfield Investment Management, a then prominent Toronto risk arbitrage fund in the late 1990’s. In 2001, Guy led a buyout of the fund and renamed it Salida Capital. Becoming Salida’s chief investment officer, Guy changed the fund’s investment strategy to a more directional, commodities oriented focus with a heavy emphasis on private equity.

(Salida is Spanish for “exit,” a commonly used term in private equity that means an investment was successfully concluded via a fund either selling an asset at a higher price or to the public through an initial public offering.)

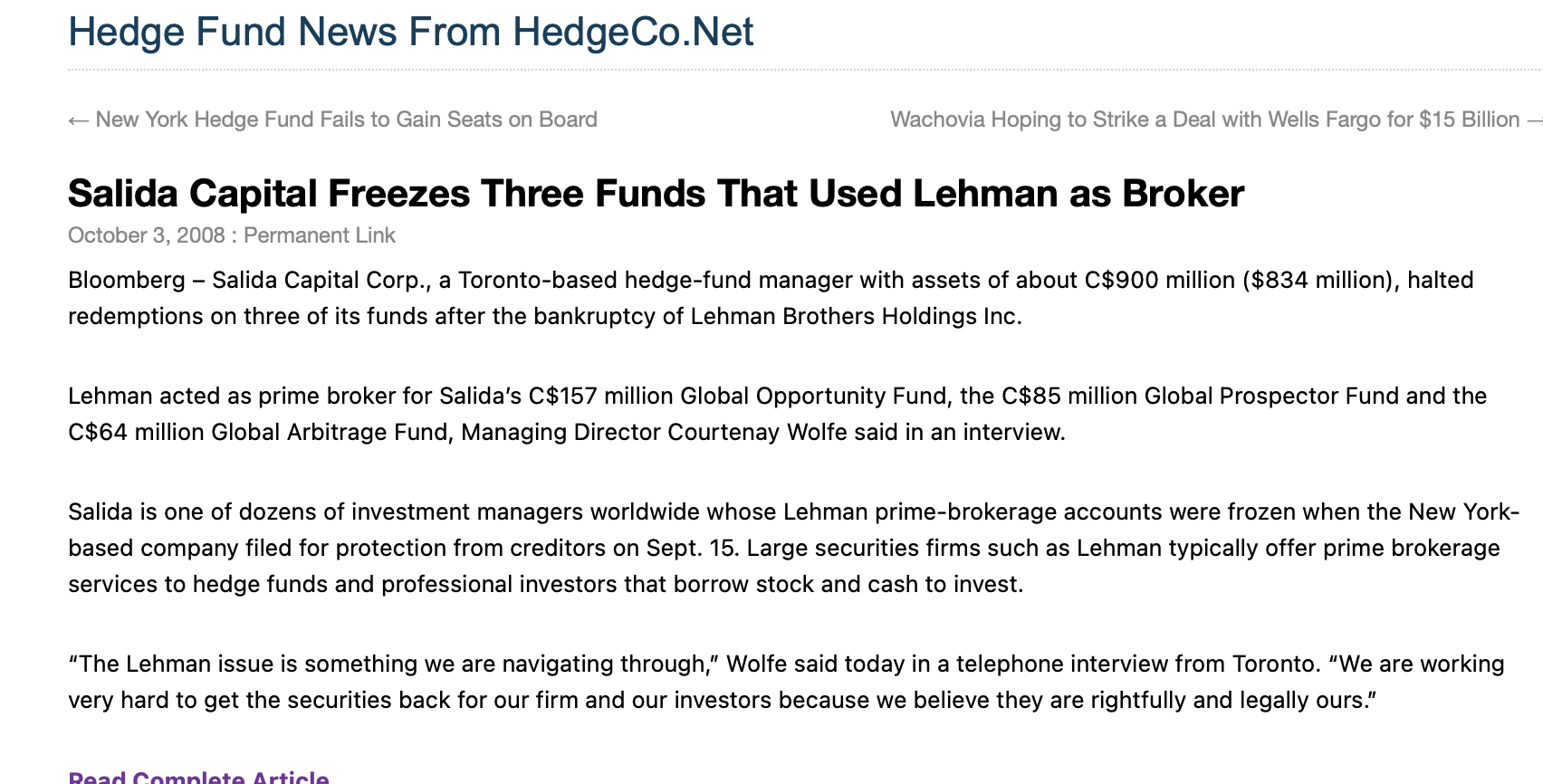

From 2002 through 2007, Salida posted very handsome returns, but in 2008, the one-two punch of the global financial crisis and the collapse of Lehman Brothers, the fund’s prime broker, led to disastrous losses. Though Salida’s performance in 2009 and 2010 was stellar, restoring the fund’s assets under management proved much more difficult, and in 2013 it began to shutter its portfolios.

{kind=link}

{kind=link}

In 2011 Guy moved to Bermuda, but it is unclear when the Luxembourg-domiciled Harrington Global was formally launched, or if it has limited partners. The fund does not appear to report to hedge fund industry databases.

Snowdy told the Foundation for Financial Journalism that his connection with Guy began when Salida Capital’s then CFO asked him to perform some due diligence on an investment Salida had made that the fund was concerned about.

“It was to look at a company called StarClub. I did some work and determined it was pretty much a fraud,” he said. (StarClub’s product was a software application that purported to help so-called social media influencers track the reach and impact of their endorsements.)

Snowdy continued that he delivered a report and forgot about it until November 2016 when Salida’s CFO called him and said, ” ‘It looks like you were really right on [StarClub] and asked me if I could I help them build a case for a lawsuit.’ ”

Snowdy said in the course of investigating StarClub in 2016 he wore a hidden recording device while posing as a potential investor during a meeting at Goldman Sachs’ headquarters, and he identified and obtained photos of a yacht that StarClub’s founder Bernhard Fritsch allegedly owned. The FBI knew about and approved everything he did, Snowdy said.

In August 2017 federal prosecutors in Los Angeles unsealed an indictment that charged Fritsch with a series of fraud-related counts. The case is scheduled to go to trial in January 2022.

According to the indictment, Guy invested more than $22.4 million of Salida and Harrington Global’s capital in StarClub.

The road to vengeance

Guy’s experience with a pharmaceutical concern called Concordia Healthcare is why he became consumed by the idea of exposing how short sellers operate.

Concordia was a once high-flying company in which Harrington Global had a 2.7 million share stake, at one point amounting to over 5.2 percent of its shares outstanding.

{kind=link}

Concordia’s business model was similar to that of Valeant Pharmaceuticals International, in that it used aggressive borrowing to fund purchases of established drugs. The goal was to simultaneously raise drug prices while avoiding costly (and recurring) research and development expenses.

It was a model that worked for a little while.

Unfortunately for both Concordia and Guy, when presidential candidate Hillary Clinton sent out a 21 word tweet on September 21, 2015, everything changed.

Clinton’s retweet of a New York Times article about a series of astronomical price hikes in a drug called Daraprim brought the issue of drug prices front and center in the 2016 presidential race.

And much of that ensuing dialogue centered on how constant drug price increases were forcing brutal sacrifices and trade-offs for many American families.

Congressional hearings soon followed.

A month later Valeant Pharmaceuticals came in for its own reckoning: On October 15 the Foundation for Financial Journalism exposed how the company’s Philidor subsidiary helped it keep certain drug prices artificially high, as well as evade pharmacy ownership regulations.

Concordia, with about $4 billion in debt and reliant on acquisitions to fund the revenue growth investors were demanding, was suddenly hamstrung in its ability to boost prices.

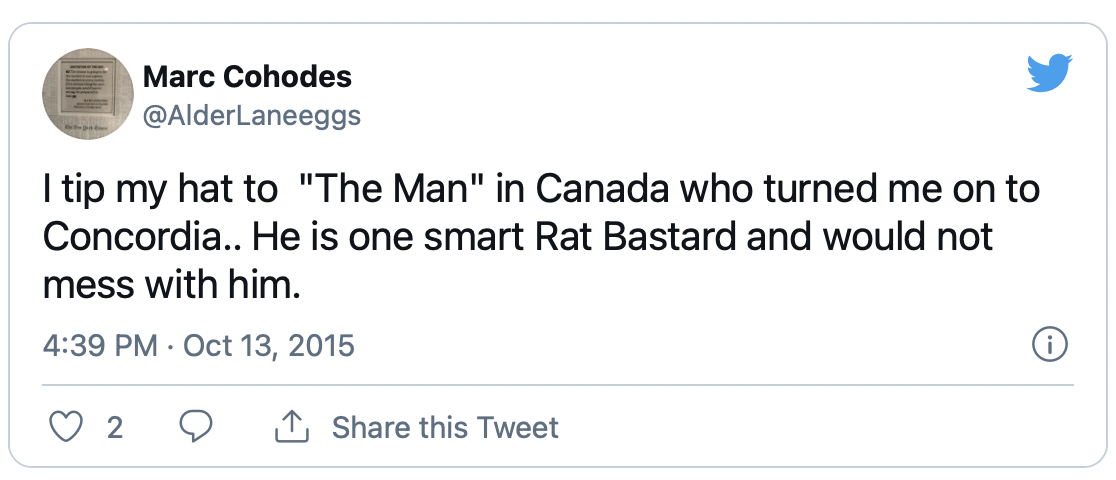

With a business model whose future had suddenly become an open question, Concordia’s share price soon began to slide. Moreover, it attracted numerous short sellers, including Marc Cohodes, an ex-hedge fund manager who uses his twitter account to offer unfiltered, often profane takes on companies he is short.

Starting in October 2015 Cohodes began building a short position in Concordia’s shares. In June 2016 company CEO Mark Thompson sued Cohodes for defamation; Cohodes happily fired back with lengthy letters to U.S. and Canadian regulators in July and August enumerating several ways he thought the company was misleading investors.

{kind=link}

In August, six weeks after suing Cohodes, Thompson was subject to a humiliating margin call, and two months later he quietly resigned. He withdrew his suit against Cohodes soon after.

Cohodes, asked for comment about Concordia, said he was happy to have shorted it, “in the $70 range,” but declined to elaborate more on the experience, beyond noting tersely, “[Concordia] was a piece of shit.”

(A word of disclosure: In 2017 Cohodes made a donation of $344,593.20 to the Foundation for Financial Journalism. He is discussed further below.)

Guy approached Canadian securities regulators in 2016 to allege that short sellers were depressing Concordia’s share price through illegal trading tactics such as “spoofing” in order to trigger a wave of algorithmic selling. No regulatory action was taken.

Concordia sought protection from creditors in October 2017, and Harrington Global liquidated its Concordia position at an approximately $150 million loss. (After reorganization, the company is now known as Advanz Pharma Corp.)

{kind=link}

Sustaining such brutal losses galvanized Guy’s thinking about Concordia’s demise: A cabal of short sellers spread disinformation about the company’s prospects while using illegal trading tactics to pressure its share price.

Central to proving this claim, Guy felt, was obtaining the identities of those responsible for perpetrating the “short-and-distort” campaign on Concordia. His attempts to get the information through hearings with regulators failed because of concerns over privacy.

To that end, Harrington Global petitioned for a Norwich Order — a motion delivered on a third-party in possession of material information — that would have compelled Canada’s brokerage regulator, the Investment Regulatory Organization of Canada, to disclose those names.

But Harrington Global’s request was denied in a 2018 Ontario Superior Court ruling.

In January Harrington Global sued a series of U.S. and Canadian banks in the U.S. District Court for the Southern District of New York. The claim primarily alleges that traders at large banks used illegal tactics that served to manipulate Concordia’s price downward.

Asked about Guy’s views on Concordia’s collapse, Snowdy assessment was blunt.

“I told Danny that [Concordia CEO] Mark Thompson was a lying sack of shit,” Snowdy said.

But, Snowdy continued, “Danny defended Mark Thompson. And then [Guy] would start screaming about naked short sales, Marc Cohodes’ role in all this, and that crap. I told him that [Cohodes] was right about Concordia.”

In a long, rambling letter to West Face’s lawyers in which Snowdy discusses his role in the Catalyst case, he said that his take on Concordia’s collapse antagonized Guy a great deal. On one occasion, when Snowdy was vacationing with his kids in the Bahamas, Guy accused him of being there to only to make secret financial arrangements — the implication being that Snowdy would only have said that because short sellers paid him off.

{kind=link}

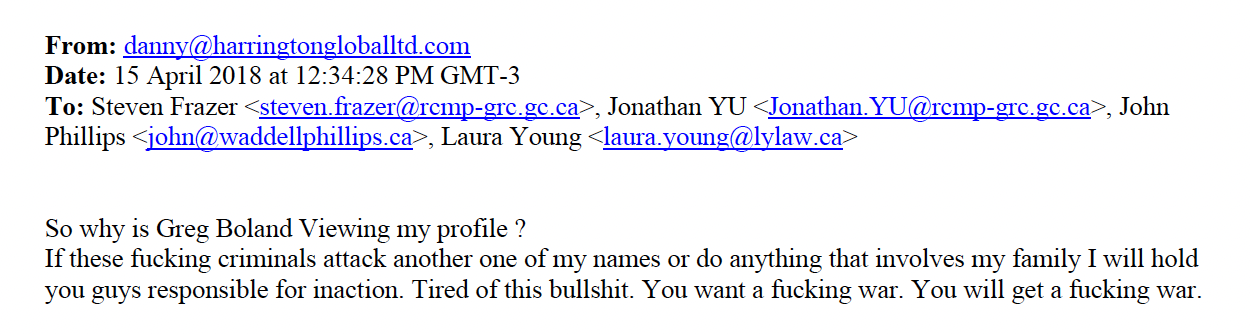

This darker turn in Guy’s worldview was on display in an April 2018 email to the Ontario Securities Commission. After Guy saw that Greg Boland, West Face Capital’s general partner, looked at his LinkedIn profile, Guy wrote an a threatening email to several OSC attorneys that promised “a fucking war” if short sellers targeted other companies he was invested in, or if anything happened to his family.

{kind=link}

[Guy was not the only one being paranoid. In a phone interview, Snowdy related how in 2018, en route to a meeting with Nate Anderson — also a defendant in the Catalyst case — he detected two people following him. This led him to believe that perhaps Anderson’s office had been somehow compromised. Anderson said that in that period his office was at a WeWork, and he didn’t think that being infiltrated by private investigators was a very big risk.]

The Foundation for Financial Journalism repeatedly sought to interview Guy. His conditions — fly to Bermuda and interview him — proved unworkable. In a response to a text message about his opposition to short selling, Guy said, “I have no problem with shorting when it’s done right.”

Penetrating the wolfpack

There was nothing terribly complex about what Snowdy did.

Starting in 2017, Snowdy began posing as a sympathetic, knowledgeable fraud-fighting ally to many of the reporters and short sellers named in the Catalyst claim. More importantly, Snowdy leveraged this nascent rapport to obtain introductions to other investors and forensic analysts who were researching and shorting publicly traded companies.

A big part of Snowdy’s operating methodology was taping phone calls, according to emails he sent; one of his two phone numbers was set to automatically record and was stored on his home computer. That may pose a prospectively large legal headache for him since he described recording California resident Marc Cohodes, and the state’s laws require both parties to consent to having a call recorded. (Cohodes strongly denied having given his consent for recording.)

{kind=link}

The unsealed documents, however, do not specify what information he got from taping Cohodes. When asked about taping Cohodes and the absence of his consent, Snowdy did not reply.

In a recently unsealed, multi-month WhatsApp message exchange between Guy and Glassman, Guy called this strategy “penetrating the wolfpack.” This echoes the theme Guy began enunciating with his angry email to the OSC: Short sellers are dangerous people.

{kind=link}

Simultaneously, Snowdy was providing what he overheard — the gossip, the sources, targets and methods – to a small group of corporate executives who felt short sellers were unfairly (or illegally) attacking their companies.

The pay for doing these infiltrations was at least decent.

According to a memorandum of an August 2017 meeting between Snowdy and private investigators working for Catalyst and its lawyers, Guy paid Snowdy $25,000 per month and covered his expenses.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

What Snowdy found

What Snowdy told people he uncovered, according to the court filings, looks very much like a version of a common short selling conspiracy trope. It usually follows along these lines: A loose network of short sellers — taking their cue from one individual leader — manipulate the press with misleading information, and then game the greedy or incompetent prime brokerage units at investment banks to allow them to flood the market with improperly borrowed stock. The result is a rapidly sinking share price for any company targeted.

Elements of this idea have been around for decades, but it was not until former Overstock.com CEO Patrick Byrne, during a 2005 presentation he called “The Miscreant’s Ball,” that these disparate complaints about reportorial malfeasance and short selling perfidy were housed in a unified theory.

Byrne claimed a Sith Lord — later revealed to be former Drexel Burnham Lambert executive Michael Milken — was then orchestrating (somehow) much of the dubious short selling activity to his benefit. He also argued that a large group of business journalists were merely transcriptionists for short sellers, and that the miscreants preferred to wage their campaigns in groups.

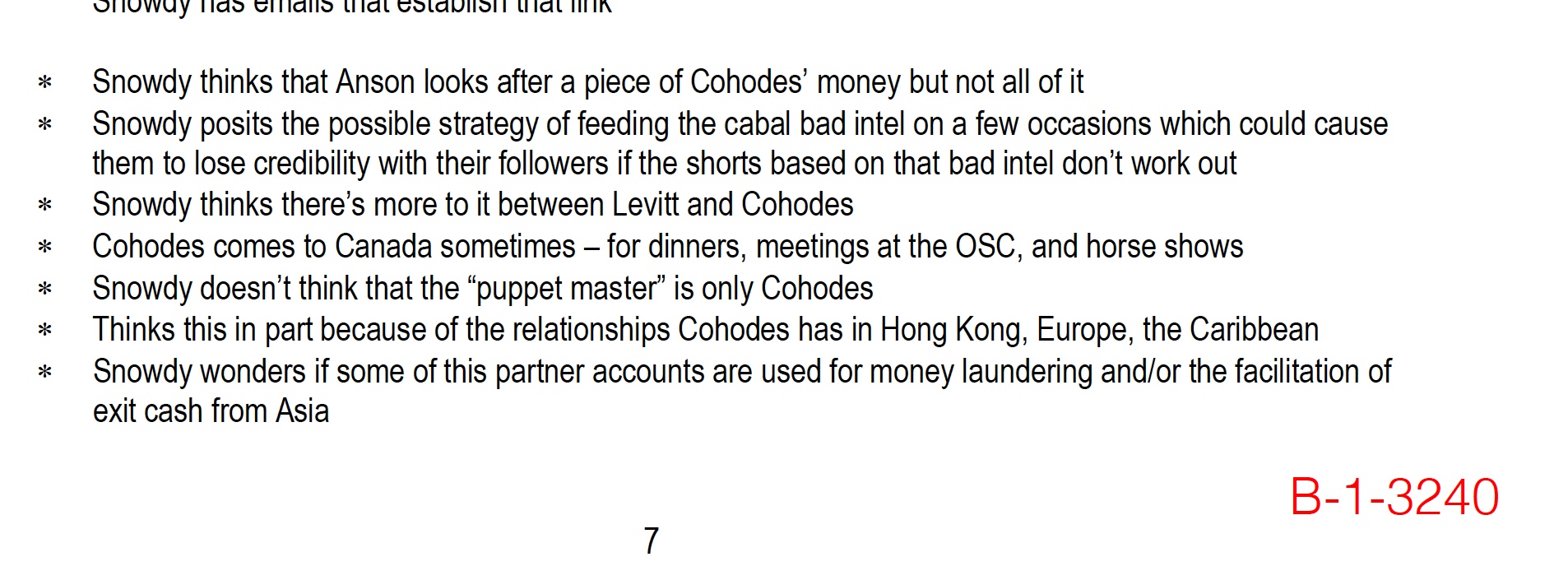

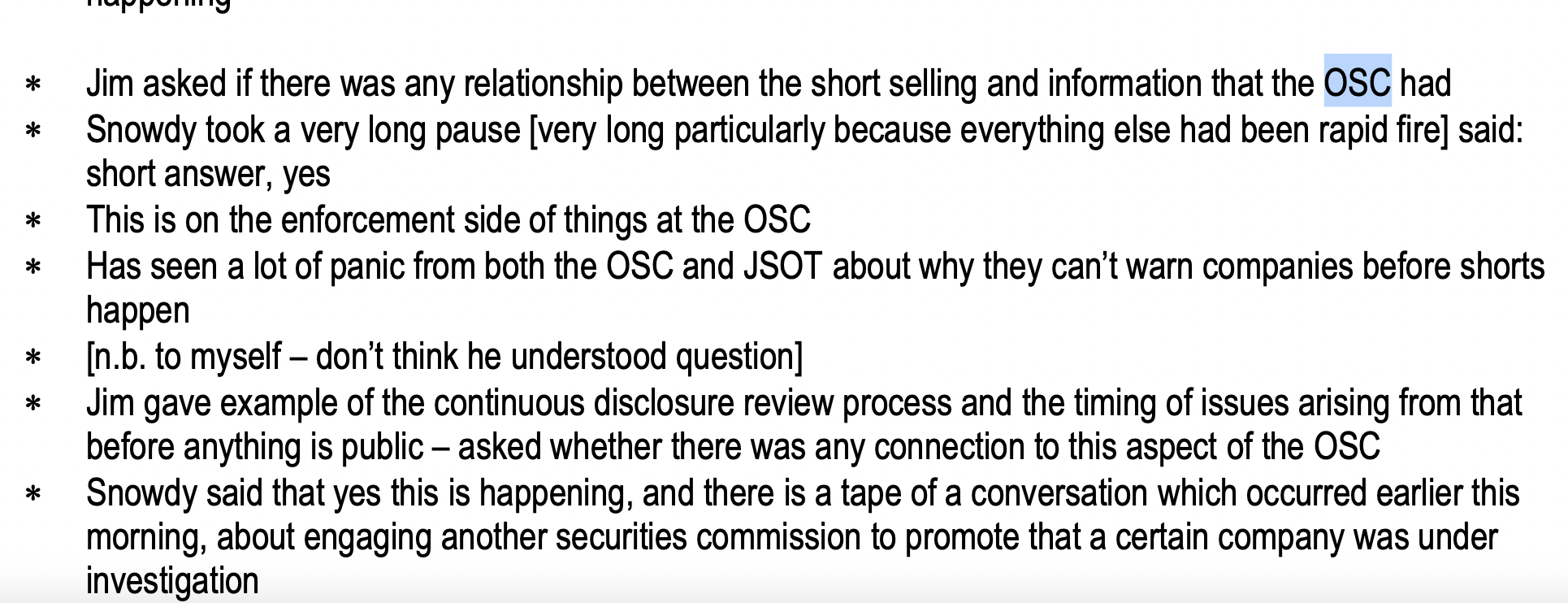

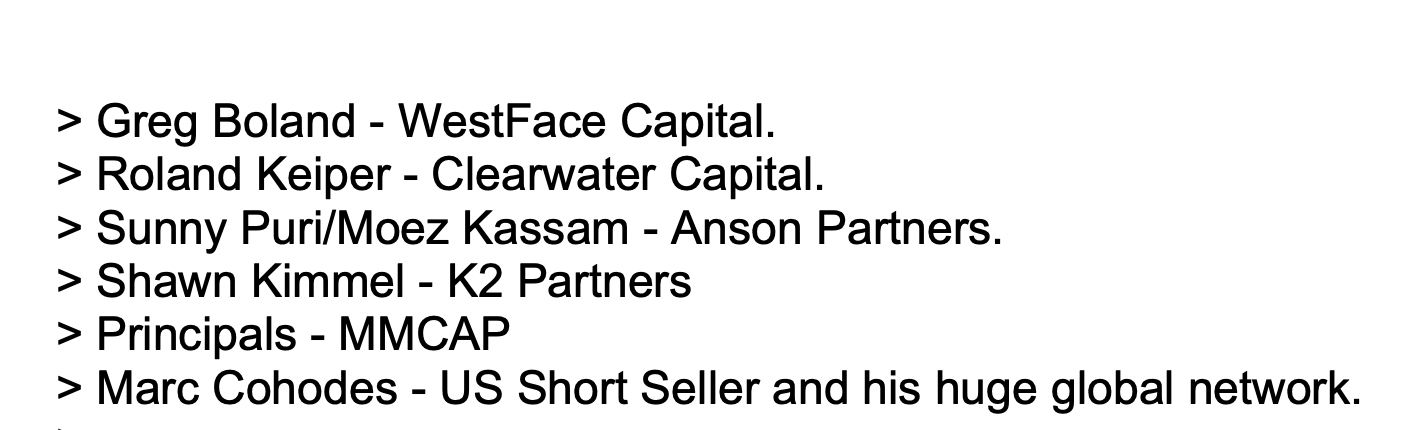

Snowdy, during a September 2017 meeting where he presented his findings to Jim Riley, former Catalyst COO and general counsel and others, leveled allegations that seemed to check many of the same boxes Byrne had complained about.

{kind=link}

There are “puppet masters” that control the network and their connections to shadowy foreign capital, as well as a slew of seemingly nefarious linkages between everyone he named. And for good measure, Snowdy touched upon regulatory capture, a favorite theory of Byrne’s, when he appeared to suggest short sellers had somehow neutralized the Ontario Securities Commission.

{kind=link}

For his part, Guy seems to agree with Deep Capture.

Guy sent Glassman a link, and told him that the article will “make your head spin.” (Snowdy, speaking about Guy’s support for Deep Capture in a meeting with Catalyst’s lawyers in September 2017, said that he felt that 25 percent of it was so untrue it calls into question the balance of the work.)

{kind=link}

And it ought to be recalled that making these types of allegations can have consequences, especially in Canada, where libel and defamation laws favor the plaintiff.

In 2008, Overstock.com’s Byrne and his then colleague Mark Mitchell published “Deep Capture,” a conspiratorially virulent expansion upon Byrne’s “Miscreant’s Ball” thesis. Altaf Nazerali, an occasional small cap stock promoter depicted in Deep Capture as an international terror finance operative, sued for libel in British Columbia’s Supreme Court. After a lengthy and expensive trial, Byrne, Mitchell and the other defendants lost the case, and in a scathing judgment, were ordered to pay $1.2 million dollars in damages.

Wearing a wire

One company that appears to have placed great stock in Snowdy’s information is MiMedx Group, an Alpharetta, Georgia-based manufacturer of skin graft and wound care products.

MiMedx filed suit in October 2017 against a series of short sellers, claiming the company had been libeled and that its business prospects were interfered with. A month later, Parker “Pete” Petit, MiMedx’s outspoken founder and CEO, began making public remarks about short selling that were nearly identical to Guy’s.

Petit focused particular ire on Marc Cohodes, accusing him in an October 13, 2017, post on the company’s website of being the ringleader of a short seller “circus” and spreading misinformation. This was baffling in that, as Cohodes put it, “I had never heard of the company until that moment.” (Cohodes also won the fight against MiMedx’s management: On February 23, Petit was sentenced to one year in prison; the COO received the same sentence.)

To get more information on Cohodes and other short sellers, MiMedx’s outside law firm, Wargo French, hired Snowdy. (David Pernini, the firm’s Atlanta-based partner that directed Snowdy’s engagement, did not return a phone call seeking comment.)

Snowdy confirmed that he had worked in 2018 for MiMedx, but that it was not a standard engagement for him. He said that he was doing so within the context of “working undercover” for an unspecified federal agency.

“Any email or report I wrote for [Wargo French] was scripted” by this federal agency, said Snowdy.

Pressed on the identity of this purported agency over several weeks, Snowdy would only say this organization’s mission is, “criminal justice, with the power to arrest people.”

Asked how much MiMedx paid him to report on Marc Cohodes and other investors critical of the company, Snowdy said he didn’t get a dime. When Snowdy was asked why he would work for free, and if that triggered any suspicions at MiMedx, he declined to comment.

Incredibly, this story gets even more unusual, with Snowdy alluding to “settlement terms” in the U.S. and Canada that prevented him from discussing his MiMedx activities.

A call to the FBI seeking comment was not returned.

Vincent Hanna dials in

Guy initiated contact with Glassman on August 11, 2017, via email, and using the pseudonym “Vincent Hanna,” a character portrayed by Al Pacino in the 1995 movie “Heat.”

(In a strange aside, Snowdy, in his letter to West Face’s lawyers, recounted meeting a pair of individuals in a New York office lobby in early 2018 who introduced themselves as “Vincent Hanna” and “Neil McCauley,” the name of the movie’s Robert DeNiro character.)

{kind=link}

While Guy used a pseudonym for an additional 12 days, he wasted little time in telling Glassman the names of short sellers he suspected were involved with Callidus Capital’s stock. Ironically, given Snowdy’s role, as well as Catalyst’s extensive use of Black Cube, Guy warned Glassman that private investigators were likely tailing him and that Russian hackers could be trying to disrupt his fund’s operations.

{kind=link}

(There has been no suggestion Guy or Snowdy had anything to do with Black Cube’s operations; Snowdy, in remarks to the Foundation for Financial Journalism, said that he believed he was a target of Black Cube too.)

In notes from an August 23, 2017, conference call with Catalyst executives and lawyer’s, Guy — still using the “Vincent Hanna” moniker — continued to frame his objection to short selling along familiar lines: Arguing Concordia was “a dry run” for taking down the much larger Valeant Pharmaceuticals, making allegations of possible Russian and Hong Kong money laundering, speculating about organized crime money at work shorting stocks, and Marc Cohodes.

Glassman was not a fan of Snowdy

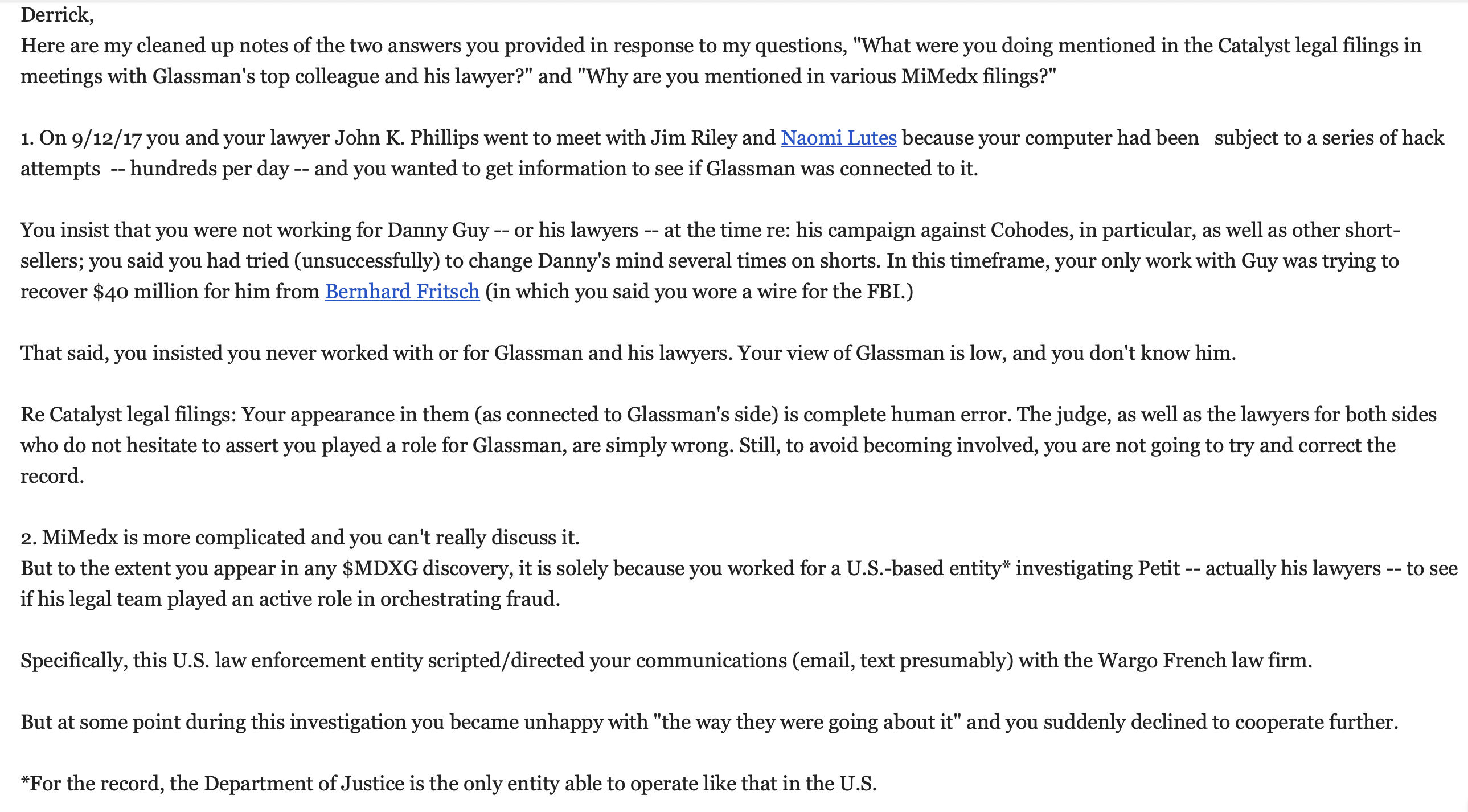

The unsealed documents show Catalyst executives and lawyers eagerly anticipating Snowdy’s research, and they afforded him three separate opportunities to present his findings.

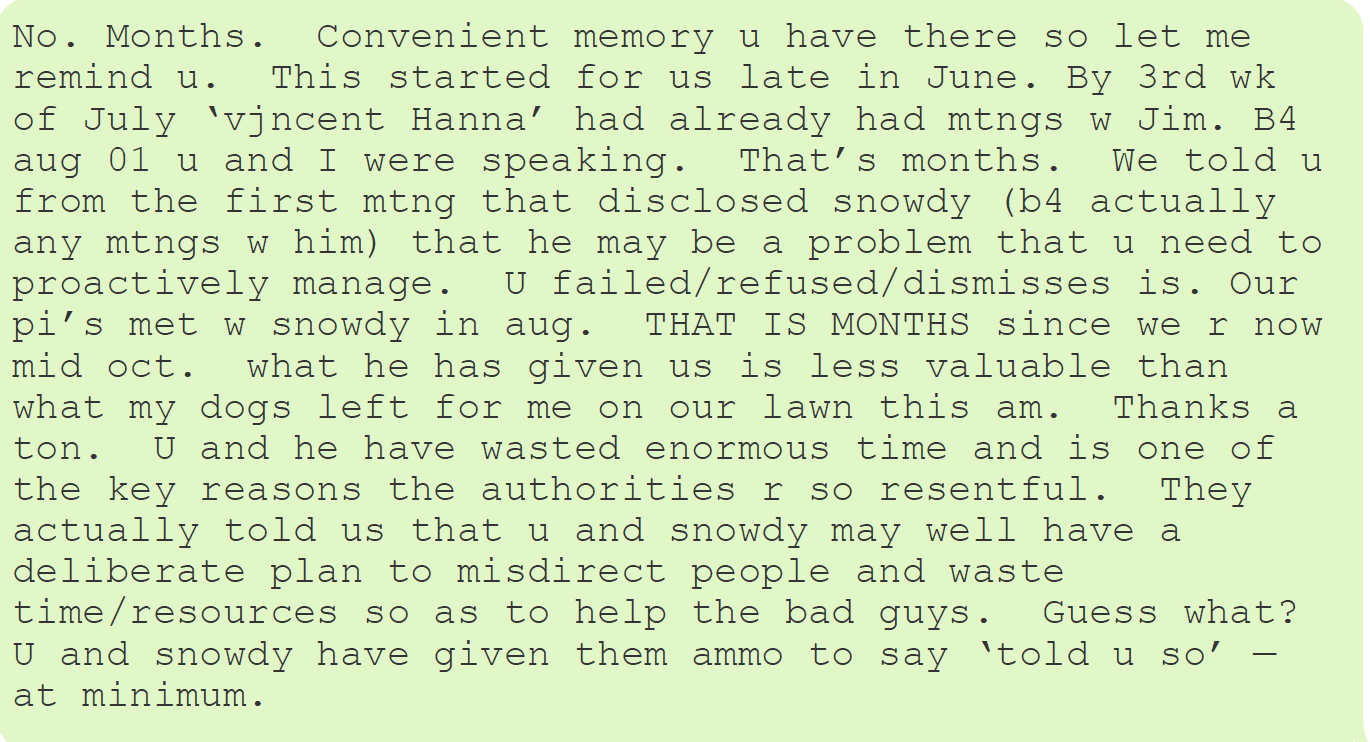

But when Snowdy could not — or would not — produce the desired recordings and emails that Guy had assured them his investigator possessed, Glassman became a vehement critic.

Glassman, quoting his lawyer after one meeting with Snowdy, said he provided, “Two and a half hours of interesting but unusable bullshit — and two and a half minutes of food for thought.”

{kind=link}

And Glassman appeared especially angry at Guy’s inability to force Snowdy to produce them since any of his work product would belong to Guy as the client.

“Right now [Snowdy] is using u and hurting u badly. U clearly r too stupid or blind to see it,” wrote Glassman.

Snowdy’s evidence, “was less valuable than what my dog’s left for me on my lawn this [morning.]”

{kind=link}

All those documents? None of them are real

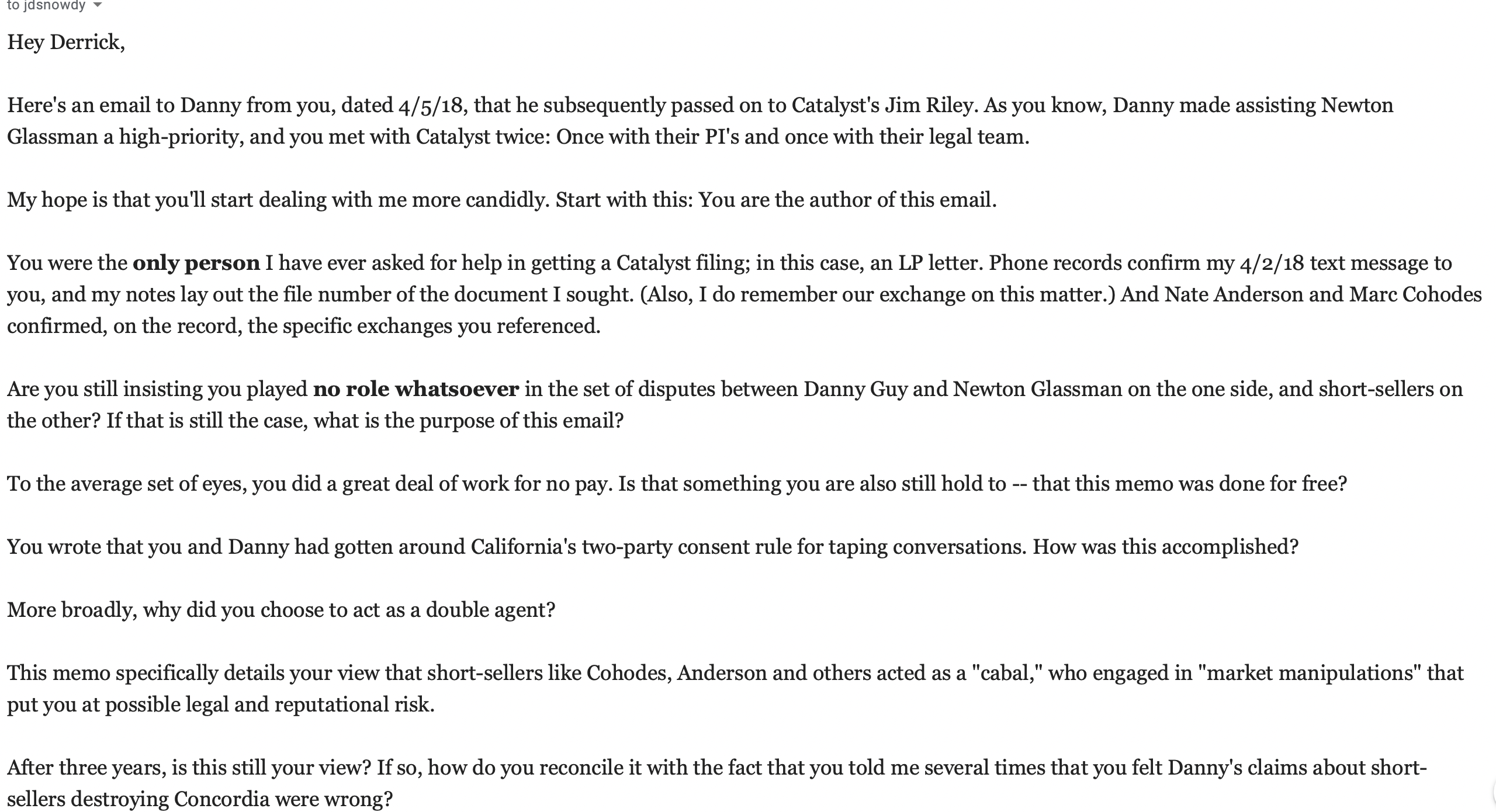

For six weeks the Foundation for Financial Journalism has been in frequent contact with Snowdy about his work for Danny Guy. Questions begat more questions and Snowdy’s response has never wavered.

{kind=link}

{kind=link}

{kind=link}

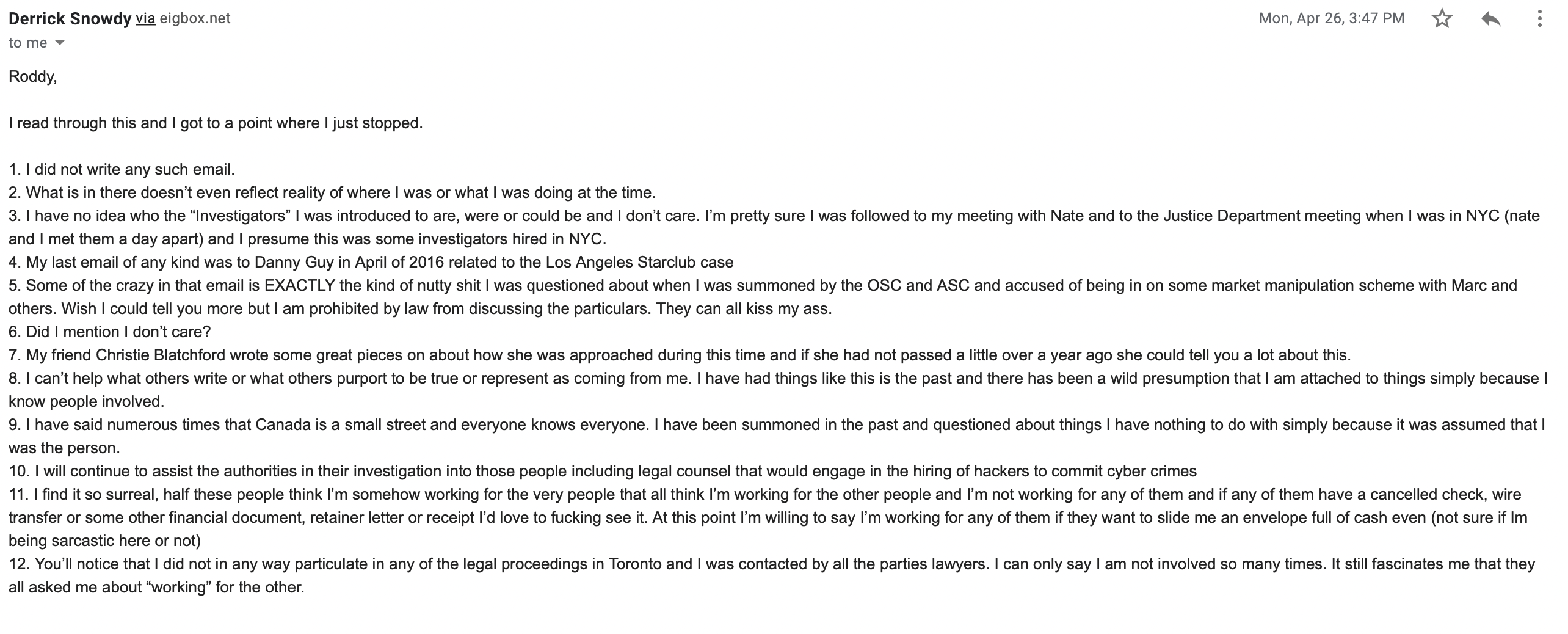

He insists that almost none of it happened.

In other words, Snowdy did not work on behalf of Danny Guy to infiltrate any networks, and has not spoken to Danny Guy since “sometime in 2016.”

The Foundation for Financial Journalism showed Snowdy emails between himself and Guy discussing his assignment in April 2018, naming certain reporters and short sellers of interest to Guy and Catalyst.

“Forgeries,” he speculated in a phone interview. “But I can’t really be sure. You would be amazed at the shit I’ve seen go down up here in terms of corruption.” (He was entirely indifferent to a reporter’s speculation that no one would believe a word of what he said.)

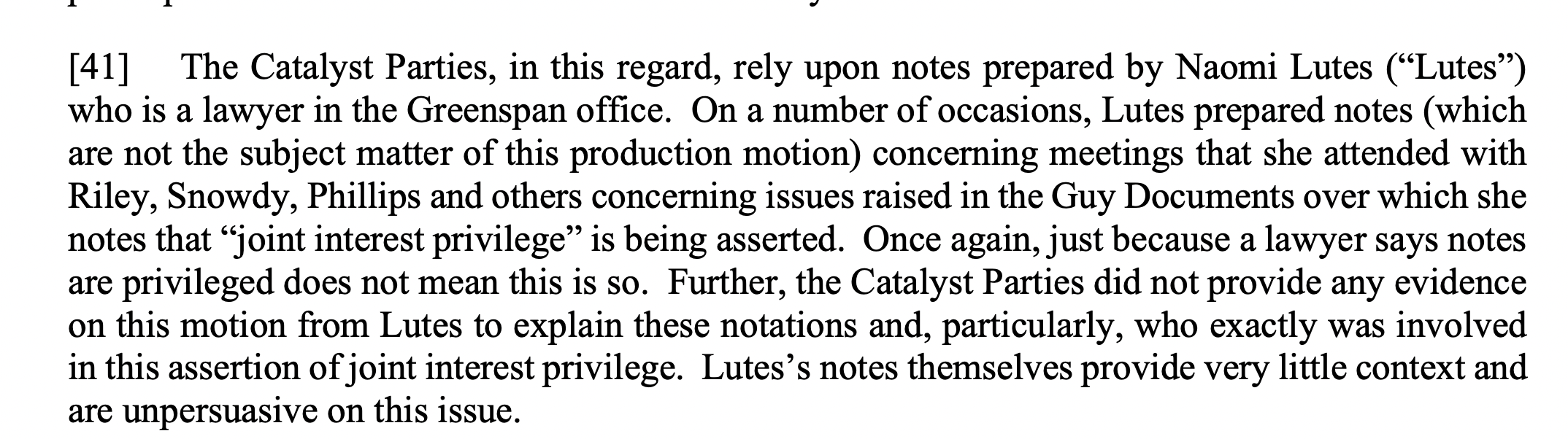

What about Snowdy’s prominence in numerous documents written by Glassman’s own lawyers, which a judge – as part of a broader 55 page ruling — ordered submitted into discovery? Snowdy told the Foundation for Financial Journalism that he did not care to speculate “who got what wrong, or why.”

{kind=link}

Snowdy did admit being at the meetings with Catalyst’s Jim Riley and the firm’s outside lawyers, but said he primarily discussed whether Catalyst had a role in some hacking attempts he had discerned on his own smartphone and computers.

Not so strong on the facts

There is a chasm between what Snowdy reported to Guy, Catalyst’s lawyers and investigators, and what can be objectively verified.

Snowdy said that he had worked with Carson Block on his Sino-Forest short and was an attendee at a Christmas party he threw. Block, however, said Snowdy had nothing to do with Sino-Forest — which he shorted in 2011, and which filed for bankruptcy protection in 2012 — and that apart from one breakfast with him in 2015 in San Francisco, he has never met him again.

[In disclosure: In 2020 Carson Block donated $5,000 to the Foundation for Financial Journalism.]

“Over the years, maybe from 2016 to 2018, we used [Snowdy] to help us track down documents on a handful of Canadian marijuana companies [Muddy Waters Capital] was considering shorting. I’m confident that we didn’t pay him over $10,000,” said Block. “And it’s been awhile since the fund worked with him, I can tell you that.”

Snowdy claimed Cohodes asked him to short stocks along side him, that he was invited to stay at his house, and, as “a loyalty test,” that he had been left alone with his son Max, Cohodes’ 33-year-old son with cerebral palsy. Nothing close to that happened.

“My God what bullshit,” said Cohodes.

“None of that happened. The part with Max is maybe the most insulting,” he said.

More stuff that Cohodes said didn’t happen: Having offshore bank accounts — something he denies in full throat — and using Anson Funds (a Canadian money manager named in the litigation) to manage his money.

“I don’t need help from [Anson] to make money,” Cohodes said.

The truth of the matter, according to Cohodes, is that Snowdy came to his house once for lunch. When he traveled to Toronto for business on several occasions, Cohodes said Snowdy drove him around.

For all that, Cohodes said he had been dragged into this controversy despite never having shorted a share of Callidus’ stock.

A personal disclosure and a mea culpa

One thing Snowdy was at least partially correct on: The introduction to Cohodes, an obvious ticket into the broader short seller community — came from me.

So some first person disclosure is called for.

First off: How did I get introduced to Snowdy? Carson Block.

According to Block, in early 2015 Snowdy contacted him out of the blue and pitched him on a story on Canadian Rail. He passed on it but suggested to Snowdy I might find aspects of the story compelling from a journalism standpoint. Block and I spoke briefly about why he passed on the story at the time and have never again discussed the issue.

I shelved the story for months. Later in the year I re-examined the parts of it that I found interesting, and in 2016 I began to report it. As part of that I reached out to Snowdy — there had been no contact between us since the year before — and he agreed to put me in contact with a man he said was his client. The client had a large cache of Canadian Rail documents that emerged from a litigation he was then involved in.

His client wanted to interact in person so I flew to Toronto. Snowdy picked me up and drove me to his client. We had a few meals in transit, and on two of the four days I was in the area, Snowdy gave me a lift to his client, and he discussed with amusement a judge’s attempt to prevent him from speaking about Canadian Rail. The story I wrote in December 2016 was almost entirely informed by my work in those documents.

It turns out Snowdy lied to me about his legal trouble in that case, having received a restraining order in 2014, according to the recently unsealed documents. (I recall looking for a mention of him in the court record and not finding any, but the ruling may have been sealed at the time or attached to a motion I overlooked.)

{kind=link}

While driving with Snowdy, he repeatedly discussed his skepticism of Concordia and Home Capital Group, a then troubled mortgage issuer Cohodes was publicly critical of. Snowdy asked me for an introduction to Cohodes. I agreed, sent an email introducing them, and never thought of it again.

What emerged afterwards is personally and professionally horrifying: Cohodes took my word that Snowdy seemed like a regular, well intentioned guy; he proved to be the very opposite of that. Over the course of a few years Snowdy used Cohodes’s name to come into his own house, meet numerous investors and it is a fair bet that any number of the people Snowdy met through Cohodes were surveilled, recorded, and through no fault of their own, may yet have some legal headaches.

Worse, with a connection to Cohodes established, Snowdy eventually got work surveilling him from MiMedx, a company that took fighting short sellers to a new level. The campaign initiated by the company’s ex-CEO was so ugly that even baseless money laundering accusations became forgettable after he leveraged his political connections to a Senator who requested that the FBI visit Cohodes’ house and warn him about a threatening tweet.

And all from my brief email introduction. It is a mistake I deeply regret.