Running a hedge fund requires a starkly different skill set from what’s required to manage a publicly traded company.

Yet hedge fund managers Kyle Cerminara and Lewis Johnson, the co-founders and co-managers of Charlotte, North Carolina–based Fundamental Global Investors, have been doing both.

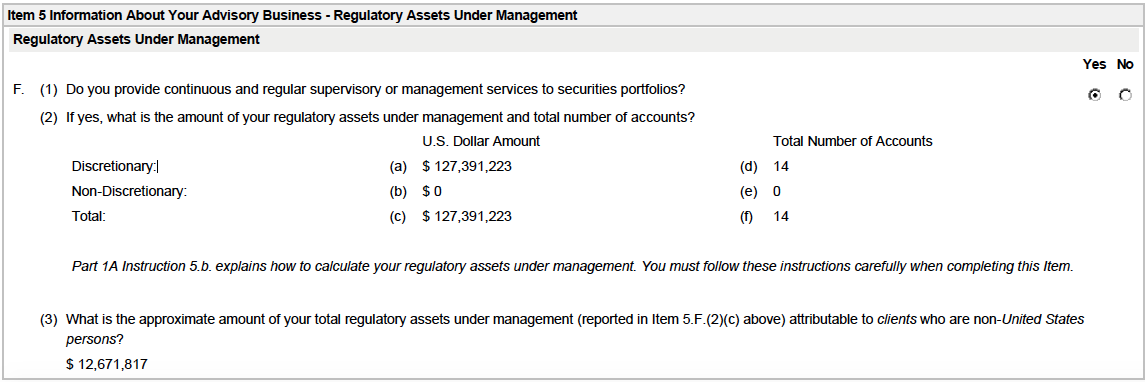

In 2015, Cerminara and Johnson began to closely direct the operations of three publicly traded companies in Fundamental Global Investors’ now $127.3 million-in-assets portfolio: Ballantyne Strong Inc. of Charlotte, North Carolina, BK Technologies Corp. of West Melbourne, Florida, and 1347 Property Insurance Holdings Inc. of St. Petersburg, Florida.

But after five years of Fundamental Global Investors’ oversight, all three of these public companies have weakened financially and their share prices have collapsed. Many minority investors in these three public companies, as well as the hedge fund’s limited partners, have absorbed steep losses.

A just-completed in-depth Foundation for Financial Journalism investigation has uncovered how, despite Cerminara and Johnson’s apparent mismanagement of these public companies, the two money managers are doing quite well for themselves.

Cerminara and Johnson have received a combined $6 million in fees and compensation from the companies they control since 2015, according to Securities and Exchange Commission filings.

This is unusual: Despite the hedge fund industry’s legacy of excesses, most fund managers typically keep their interests at least broadly aligned to their limited partners. Nearly every hedge fund has a so called high-water-mark provision, prohibiting a manager from taking performance fees (and thereby sharing in the profits) until limited partners’ losses are fully recovered.

Cerminara and Johnson have circumvented these norms. Just as important, their decisions appear to have rarely favored all investors: Cerminara and Johnson have steered clear of buying back stock or making substantial investments to improve these public companies’ operations.

Their strategy might be best referred to as parasitic investing: Cerminara and Johnson are faring well, but Fundamental Global Investors’ limited partners are suffering along with the employees and minority shareholders of these public companies.

———————

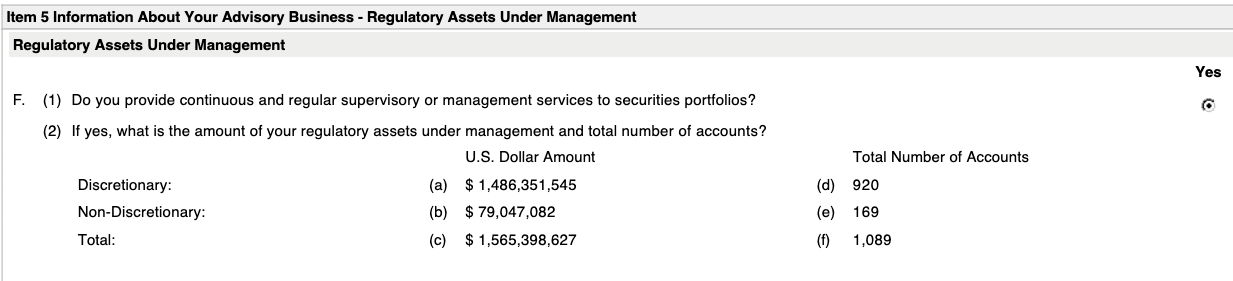

Fundamental Global Investors has owned 50 percent of Capital Wealth since 2013. Staffed with 31 advisers, Capital Wealth Advisors has $1.56 billion in client assets under management, according to its most recent regulatory disclosure.

A crucial aspect to Fundamental Global Investors’ stake in Capital Wealth is its history of achieving significant profits. Since most registered investment advisers charge clients a fee of 1 percent of assets under management, Capital Wealth’s current $1.5 billion in assets is likely generating about $15 million in annual revenue.

In contrast to the thinly capitalized underpinnings of many hedge funds that operate independently of a corporate parent (and are thus unable to absorb sustained losses), Cerminara and Johnson have their Capital Wealth Advisors income stream. This gives them the financial freedom to pursue an atypical strategy for their hedge fund. Fundamental Global Investors has embraced the high-risk strategy of holding small capitalization stocks in its portfolio for years at a time.

————————

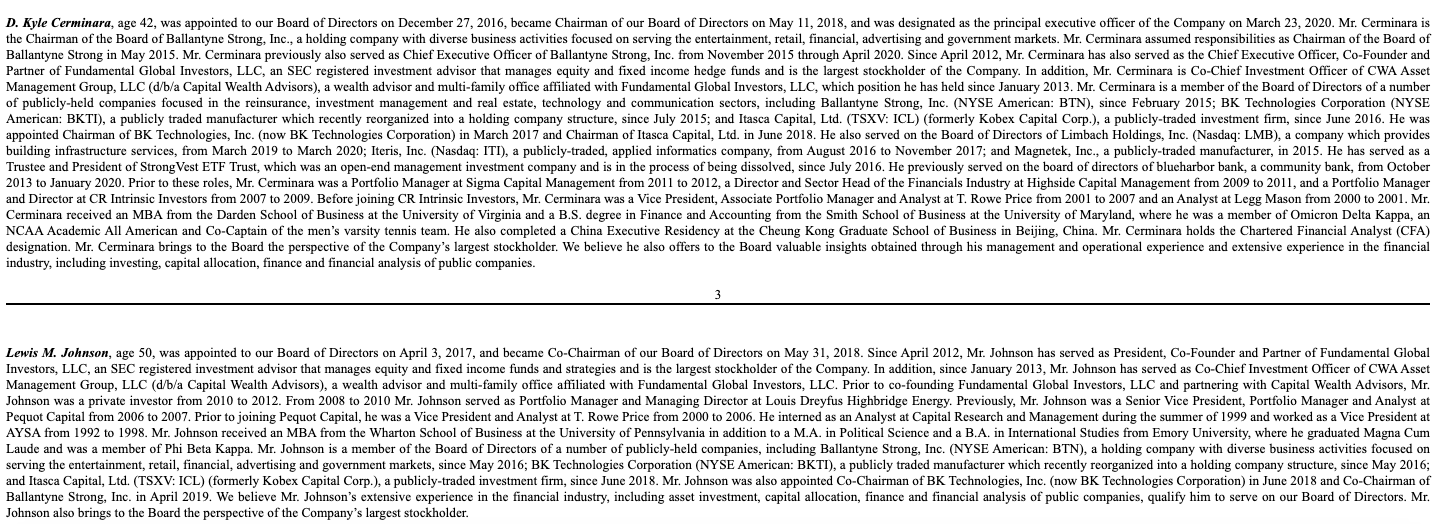

Cerminara and Johnson met while working at T. Rowe Price over the last decade and founded Fundamental Global Investors in 2012. The third FGI partner is Joseph Moglia, who at the time of the fund’s founding was then chairman of TD Ameritrade’s board of directors. (From 2000 to 2008 he was also TD Ameritrade’s CEO.)

While Moglia is one of Fundamental Global Investors’ three general partners he does not manage any of its portfolios. In 2013 Capital Wealth appointed Moglia as its chairman, a position he retains today along with chairing TD Ameritrade’s board. (Moglia also spent seven years as the head coach of the football team at Coastal Carolina University in Myrtle Beach, South Carolina, until January 2019.)

During Moglia’s tenure Capital Wealth has benefited substantially from its ties to TD Ameritrade: Through TD Ameritrade’s AdvisorDirect referral program, Capital Wealth has picked up about $400 million in new assets since 2014. And Capital Wealth’s assets under management have grown from $200 million in 2013 to almost $1.5 billion in 2020.

Like most registered investment advisers, Capital Wealth has a client base primarily composed of high-net-worth individuals who have diverse sources of wealth and varying levels of capital markets exposure. The firm’s co-chief investment officers regularly provide their staff advisers and clients a model portfolio, replete with recommendations for weighting assets, such as stock, bonds and cash, according to their tolerance for risk.

And Capital Wealth’s co-chief investment officers just happen to be Kyle Cerminara and Lewis Johnson, Fundamental Global Investors’ leaders. They have regularly suggested that Capital Wealth’s clients assign 5 percent to 10 percent of their portfolios to so-called alternative investments (such as hedge funds or private equity). Nonetheless, Fundamental Global Investors has not had much luck in attracting many of Capital Wealth’s wealthy clients to invest in its hedge fund as limited partners.

Until 2018 a key recommendation of Cerminara and Johnson was promoted in Capital Wealth’s model portfolio: Clients should acquire their own shares of Ballantyne Strong, BK Technologies and 1347 Property Insurance Holdings.

Capital Wealth stopped this practice in 2018 for two reasons: The three companies’ poor share price performance led several Capital Wealth advisers to opt out of marketing Cerminara and Johnson’s model portfolio to clients. And the combined value of the stakes in these three companies owned by Capital Wealth and Fundamental Global was so large relative to the daily trading volume of the three stocks that concerns were raised about Capital Wealth clients’ ability to sell their stocks in an orderly fashion.

————————

About one-fifth of Fundamental Global’s capital has come from its three general partners: Cerminara, Johnson and Moglia. That’s $26.9 million of its $127.3 million in capital, according to Fundamental Global’s March 30 Form ADV filing.

No limited partners appear to be institutional investors: The Foundation for Financial Journalism searched hedge fund databases ― both those publicly available and private ones ― and could not find any records of a pension fund or another institution that had invested in Fundamental Global.

Institutions such as pension and sovereign wealth funds, private foundations and university endowments have traditionally been key sources of capital for hedge funds. These institutions (or their advisers) often conduct rigorous due diligence before investing in hedge funds. And even after making an investment, such institutions require extensive communication from a fund’s general partners about the results.

Lacking such oversight, Cerminara and Johnson have proceeded to run their hedge fund in a rather unique fashion.

———————

Consider the actions Fundamental Global has taken with Ballantyne Strong, a maker of both digital movie equipment and taxicab signage.

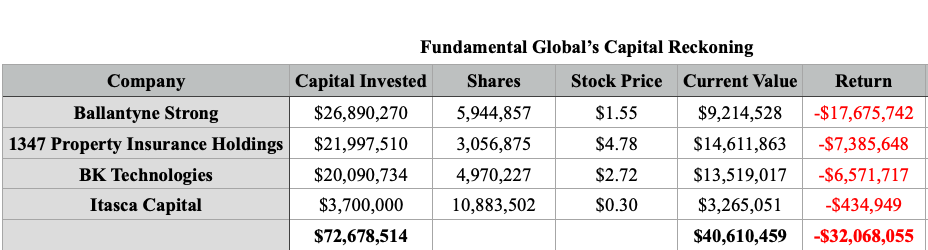

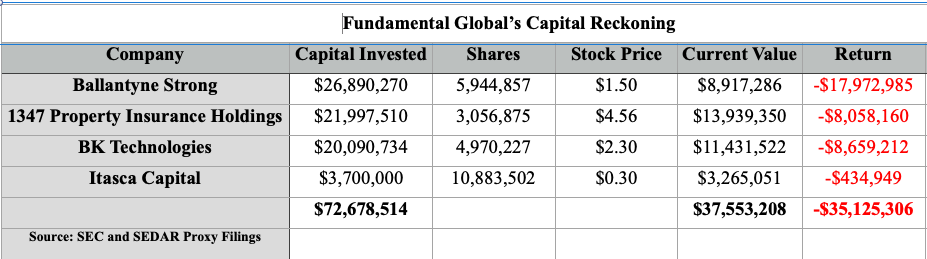

Fundamental Global has spent almost $26.9 million to buy 5,994,857 shares of Ballantyne Strong, according to Ballantyne Strong’s Schedule 13D filings from Sept. 3, 2014, to March 16, 2020. With Ballantyne Strong’s stock priced at just $1.50 a share as of May 4, Fundamental Global Investors’ shares are now worth about $8.85 million, meaning the fund has lost slightly more than $18 million from these purchases.

Of course, virtually every professional money manager has made investments that have not panned out, and most limited partners recognize that.

Nonetheless, since November 2015 when Cerminara became Ballantyne Strong’s CEO, Ballantyne Strong’s revenue has declined and its losses have mounted. (In 2015 Ballantyne Strong took a $11.2 million charge against its earnings to reduce expenses and reorganize its operations; this helped it report a profit in 2016, the only time it did during Cerminara’s tenure.) On April 15 Ballantyne Strong announced that Cerminara is no longer its CEO; he is now the non-executive chairman of the board.

Sharp market observers would be unsurprised that no pension or sovereign wealth fund has opted to become a limited partner of Fundamental Global as it has continually added capital to a losing bet (Ballantyne Strong) for more than half a decade.

———————

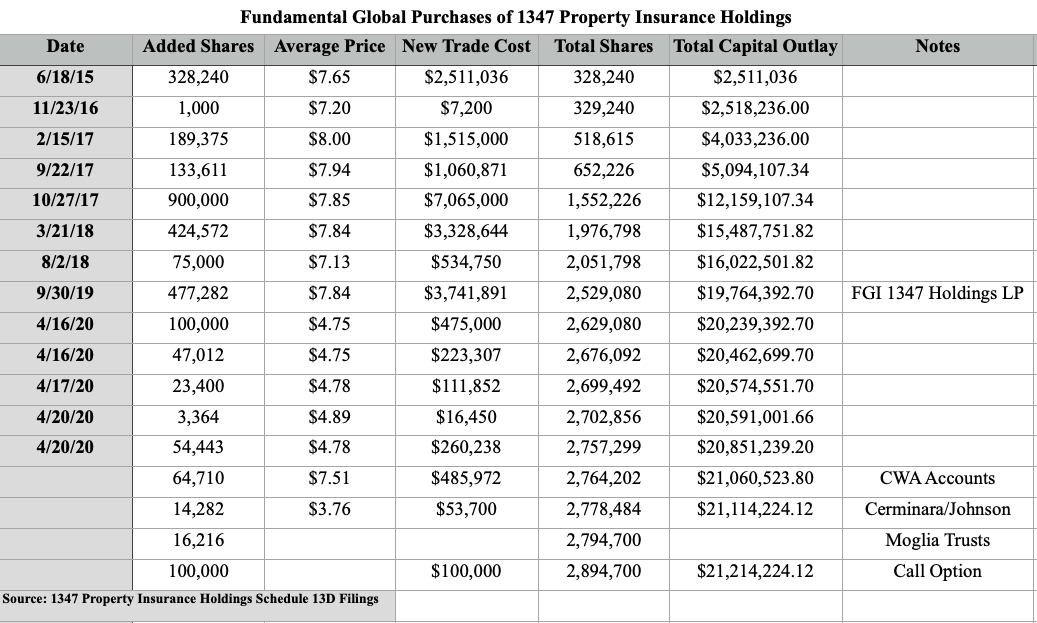

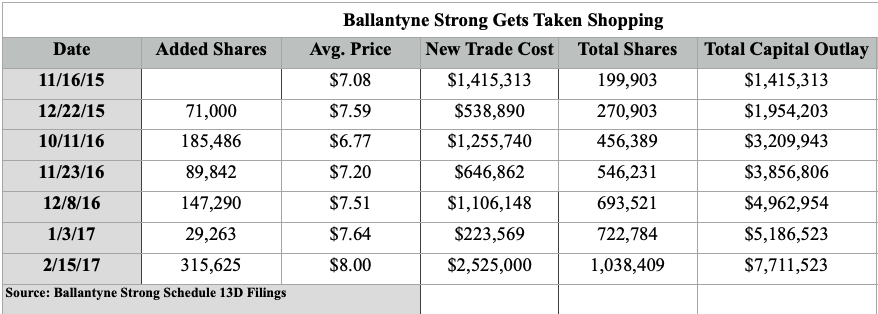

The first instance of Fundamental Global’s unusual use of its related public companies’ capital cropped up nearly five years ago. On Nov. 16, 2015, Fundamental Global disclosed that it had used Ballantyne Strong’s cash to purchase a block of shares of 1347 Property Insurance Holdings, a residential property insurer with operations primarily in Florida, Louisiana and Texas.

This transaction seems to have become a template of sorts that Fundamental Global has repeatedly used over the next couple of years to carry out elaborate cross-ownership stock schemes with Ballantyne Strong, BK Technologies and 1347 Property Insurance Holdings. Under Fundamental Global’s management, the balance sheets of these three public companies have rapidly expanded and contracted with one another’s shares.

From November 2015 to February 2017, Cerminara and Johnson spent $7.71 million of Ballantyne Strong’s cash to purchase a little more than 1 million shares of 1347 Property Insurance Holdings.

The primary benefit to Fundamental Global Investors from using Ballantyne Strong’s balance sheet appears to have been capital efficiency: Less of Fundamental Global Investors’ own capital had to be expended for it to attain voting control over 1347 Property Insurance Holdings. As of April 22, Fundamental Global Investors controls 50.4 percent of 1347 Property Insurance Holdings.

———————

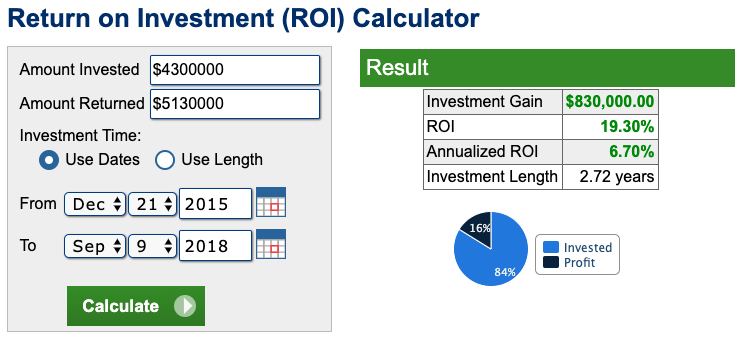

Another clear demonstration of how Cerminara and Johnson have used Ballantyne Strong’s cash to further Fundamental Global Investors’ goals surfaced on Dec. 21, 2015, when Ballantyne Strong disclosed its nearly $4.3 million purchase of 1.14 million shares of BK Technologies (then known as RELM Wireless). On Sept. 9, 2018, Fundamental Global Investors bought these very shares for $4.53 million, generating a $200,000 profit for Ballantyne Strong. (In addition, during this period, BK Technologies paid $600,000 in dividends to Ballantyne Strong.)

On the surface, Fundamental Global Investors’ use of Ballantyne Strong’s cash to buy and hold a BK Technologies stake for almost three years might appear to have paid off for Ballantyne Strong’s shareholders, by generating a modest 6.7 percent annual return on investment.

But a closer look at Ballantyne Strong’s filings reveals a very different picture.

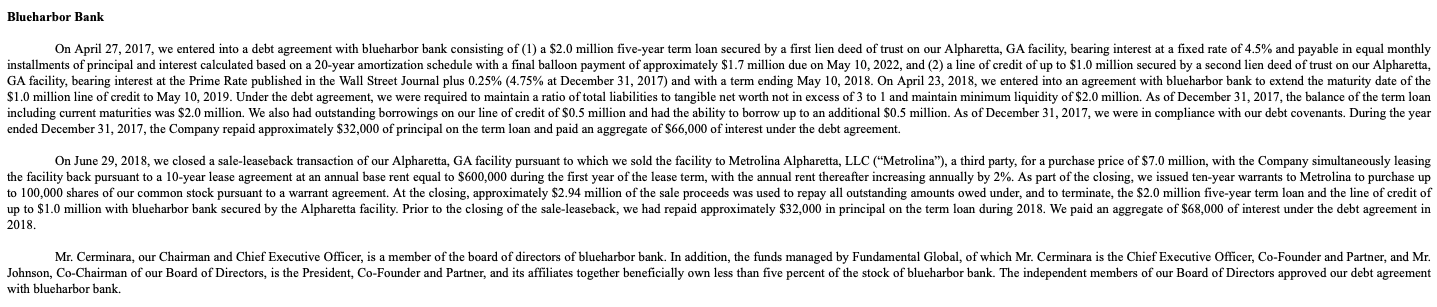

While Fundamental Global Investors was directing Ballantyne Strong to spend more than $12 million to build its stock positions in both BK Technologies and 1347 Property Insurance Holdings, one of Ballantyne Strong’s key subsidiaries was strapped for cash: In April 2017 it borrowed money against its headquarters building. A year later, Ballantyne Strong orchestrated a sale-leaseback transaction for this property. (A sale-leaseback deal, allowing a company to sell an asset and lease it back for a period of time, can indicate that the business is under acute financial stress.)

The sale-leaseback filing, attached as an exhibit to Ballantyne Strong’s 2018 annual report, lays out the deal’s fine points: the $7 million price tag for the Alpharetta, Georgia, facility and the $612,000 annual charge for leasing it back. After closing the deal, Ballantyne Strong immediately paid down a $2.94 million debt to BlueHarbor Bank from a term loan and a lien against the headquarters.

Until late 2019 Cerminara served on this bank’s board; Ballantyne Strong disclosed in 2018 that Fundamental Global Investors held “less than five percent” of BlueHarbor Bank equity.

Jim Marshall, BlueHarbor Bank’s CEO, recently explained Cerminara’s departure from the board of Blue Harbor Bank to the Foundation for Financial Journalism in this way: “He wanted to leave quietly and we saw no problem with that,” said Marshall, adding, “He is a busy man, with a lot of irons in the fire.” (Cerminara retains a BlueHarbor Bank tie since Capital Wealth still operates an investment advisory joint venture with BlueHarbor Bank that it initiated in 2014 under the name BlueHarbor Wealth Advisors.)

Marshall declined to discuss the specifics of BlueHarbor’s loan to Ballantyne Strong other than declaring, “Everything [about the loan] was above board and beyond reproach.”

All told, Ballantyne Strong has become a weaker, less healthy company in terms of revenue, net income and cash generation since Cerminara took the helm as CEO in November 2015.

Shareholders have borne the brunt of the company’s decline: On Sept. 3, 2014, the date that Fundamental Global Investors disclosed its initial equity stake in Ballantyne Strong, the company’s market capitalization was $63.24 million. On May 4, 2020, it was only $22.26 million.

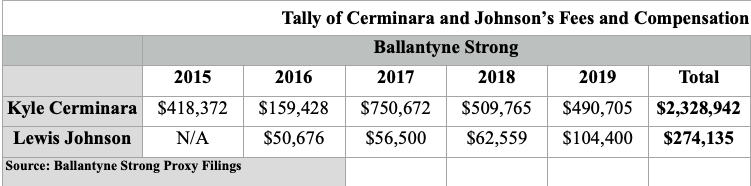

Yet despite this destruction of the company’s value, from 2015 to 2019 Ballantyne Strong paid slightly more than $2.6 million to Cerminara and Johnson in compensation and director’s fees, with almost $2.33 million of that going to Cerminara.

———————

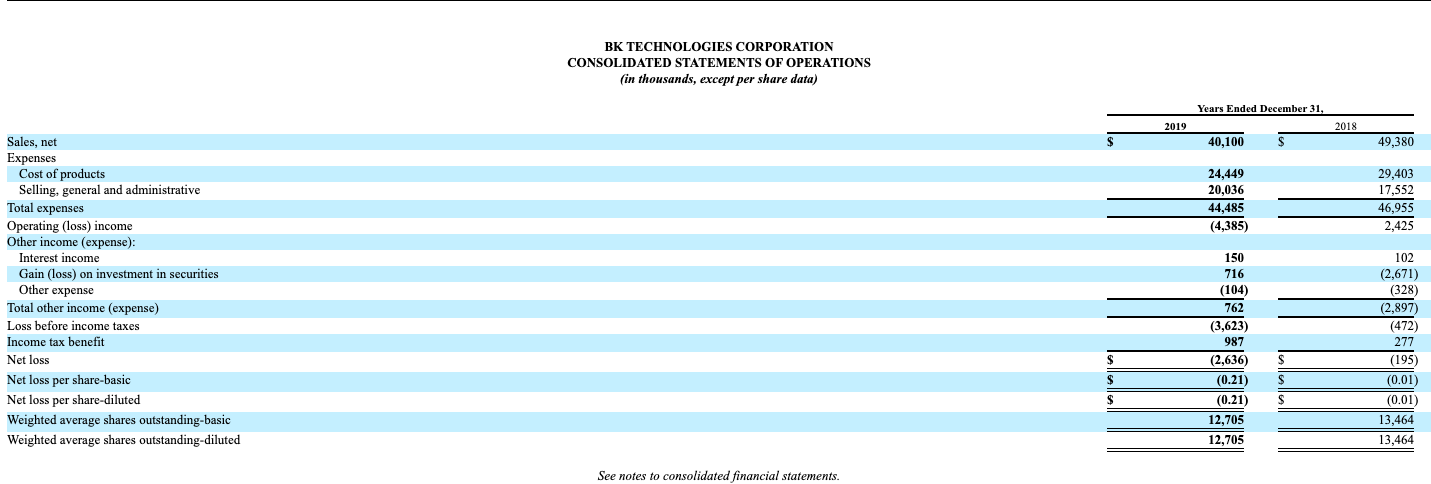

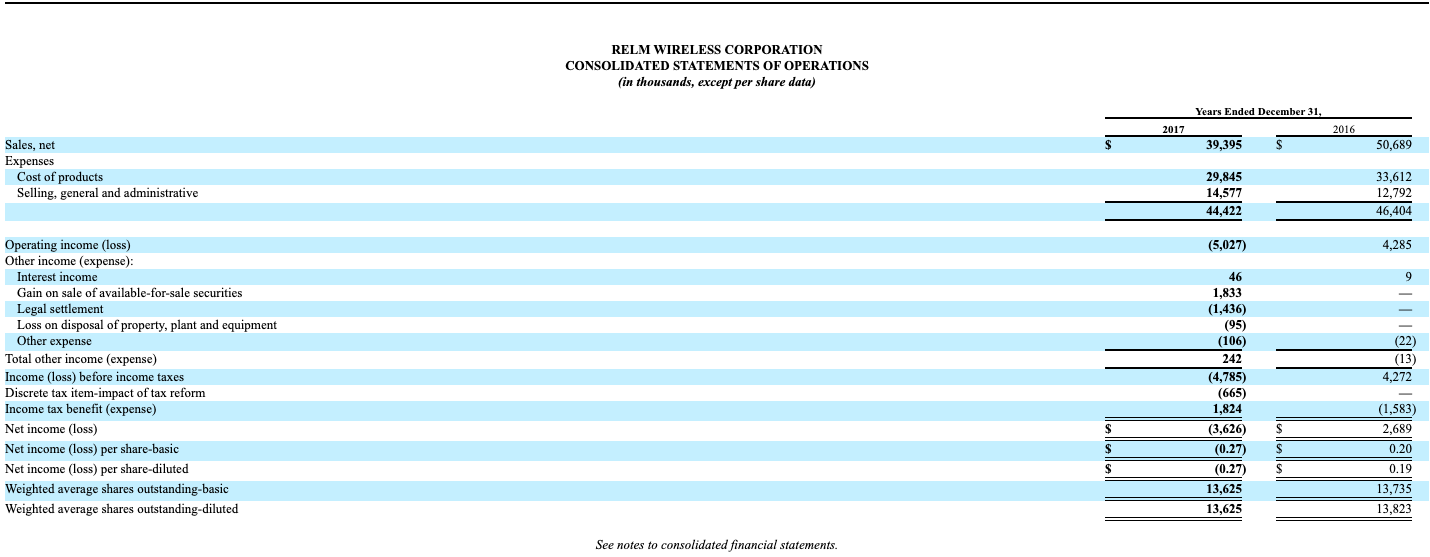

A misalignment similar to the one between the interests of Ballantyne Strong’s majority shareholders and those of its minority investors has also occurred at BK Technologies.

Established more than 70 years ago, BK Technologies has a mission, according to its website, “to remain deeply rooted in the critical communications industry for all military, first responders, and public safety heroes.” And 45.1 percent of its shares are owned by Fundamental Global Investors.

On March 17, 2017, when Cerminara became BK Technologies’ chairman of the board, its share price was $5.10, and the company had just announced it had $2.68 million in net income for 2016. Three years later, BK Technologies reported a cumulative $6.45 million in losses. Now its share price is just $2.30.

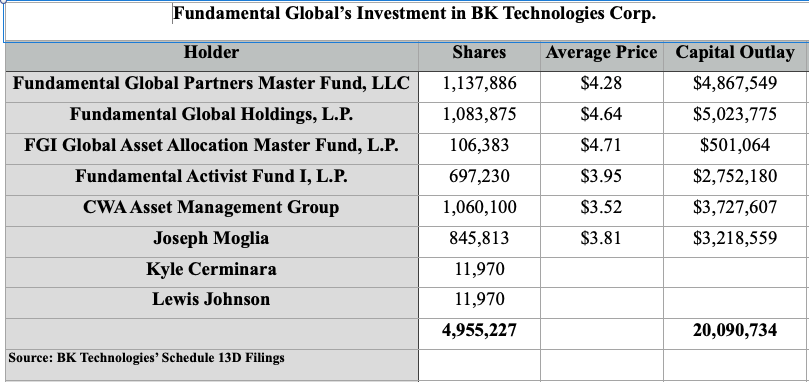

It is likely cold comfort to BK Technologies’ minority investors that they have fared somewhat better from this arrangement than Fundamental Global Investors’ limited partners. Fundamental Global Investors purchased a cumulative total of 4.97 million BK Technologies shares for $20.09 million, according to filings from Sept. 3, 2014, to March 17, 2020. The limited partners’ stake in BK Technologies is now worth only $13.47 million, representing a loss of $6.61 million for all the limited partners.

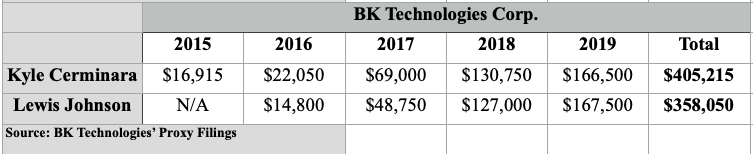

Yet, from 2015 to 2018, BK Technologies paid a total of $763,265 to Cerminara and Johnson, or $405,215 and $358,050, respectively, for their serving as chairman and co-chairman of its board of directors. (Cerminara and Johnson did not respond to an April 8 question from the Foundation for Financial Journalism about whether Fundamental Global Investors’ limited partners had been directly told about these payments.)

On April 24 BK Technologies announced that Cerminara and Johnson had resigned their roles as co-chairmen of its board of directors, in a move that became effective immediately. They retain positions as directors of the board.

———————

Much like what Ballantyne Strong and BK Technologies shareholders have experienced, Fundamental Global Investors’ involvement with 1347 Property Insurance Holdings has done no favors for its investors.

On June 15, 2015, the date Fundamental Global Investors reported that it had begun building a stake in 1347 Property Insurance Holdings, the company’s market capitalization was $50.64 million. By May, it had plummeted to $27.68 million.

In addition, the limited partners of Fundamental Global Investors are hardly benefiting from its investment in 1347 Property Insurance Holdings. The 3.05 million shares of 1347 Property Insurance Holdings that Fundamental Global Investors purchased for almost $22 million are now worth just $13.94 million, leaving Fundamental Global Investors’ limited partners and Capital Wealth’s clients with an $8 million loss from this investment.

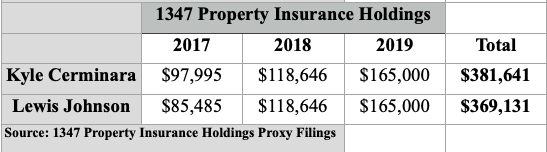

Cerminara and Johnson became chairman and co-chairman, respectively, of 1347 Property Insurance Holdings’ board of directors in May 2018. In 2019 Cerminara and Johnson each earned $165,000 in director fees, and since 2017 have earned a combined total of $750,772 from these duties.

But a recent corporate restructuring at 1347 Property Insurance Holdings makes its situation very different from the dynamics at play at Ballantyne Strong and BK Technologies. Cerminara and Johnson, as the general partners of the hedge fund that owns 50.4 percent of 1347 Property Insurance Holdings’ stock, are carefully remaking the public company from the bottom up and taking care to ensure they have numerous opportunities for profit at every turn.

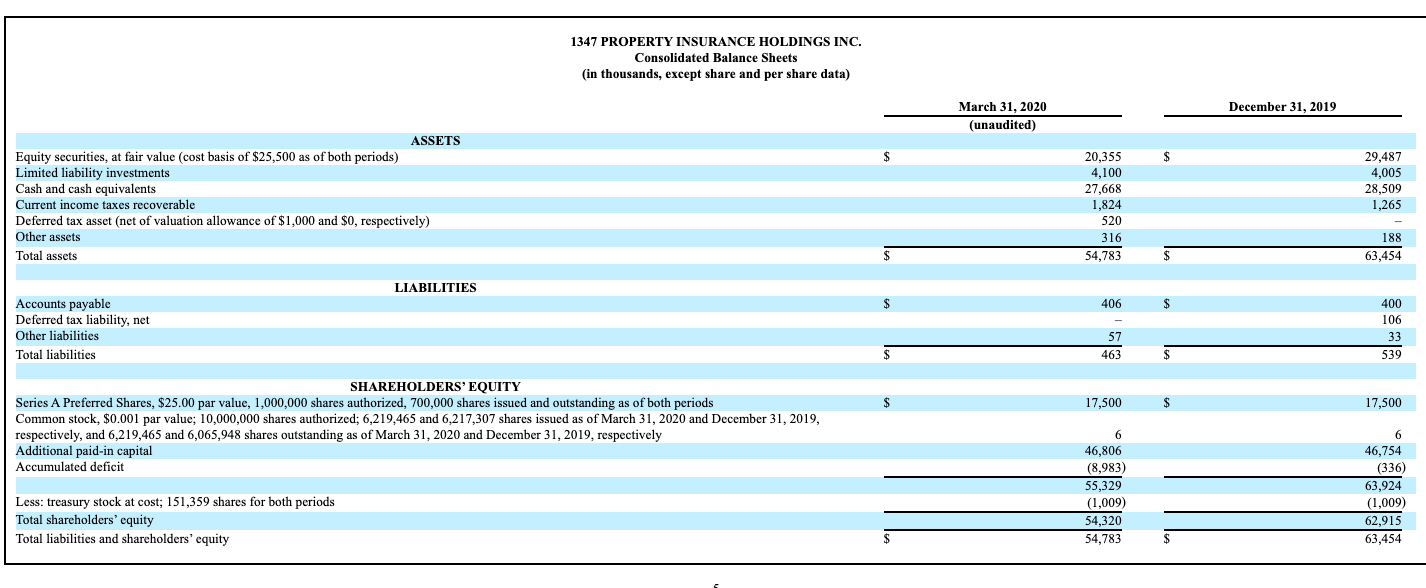

On Feb. 25, 2019, the management of 1347 Property Insurance Holdings agreed to sell its property insurance operations to FedNat Holding Company for $51 million. By Dec. 31, 2019, the sale was completed and all these operations were transferred to FedNat. Thus, 1347 Property Insurance Holdings began this year without any specified business operations.

But what apparently makes 1347 Property Insurance Holdings so attractive to Cerminara and Johnson is that the company has no debt and nearly $6 a share’s worth of liquid assets: cash, FedNat stock and other investments. And with 1347 Property Insurance Holdings’ current share price of $4.56, the company is trading at a discount to its book value, a rare occurrence for a publicly traded company.

Typically when a company’s stock is trading at a discount to its book value, investors will take advantage of the pricing inefficiency by buying the stock, sending the share price back into line with its book value. Alternatively, investors could decide to liquidate the company and distribute the assets on a pro rata basis and obtain roughly the same level of risk-free return.

What Cerminara and Johnson have in mind is apparently something different.

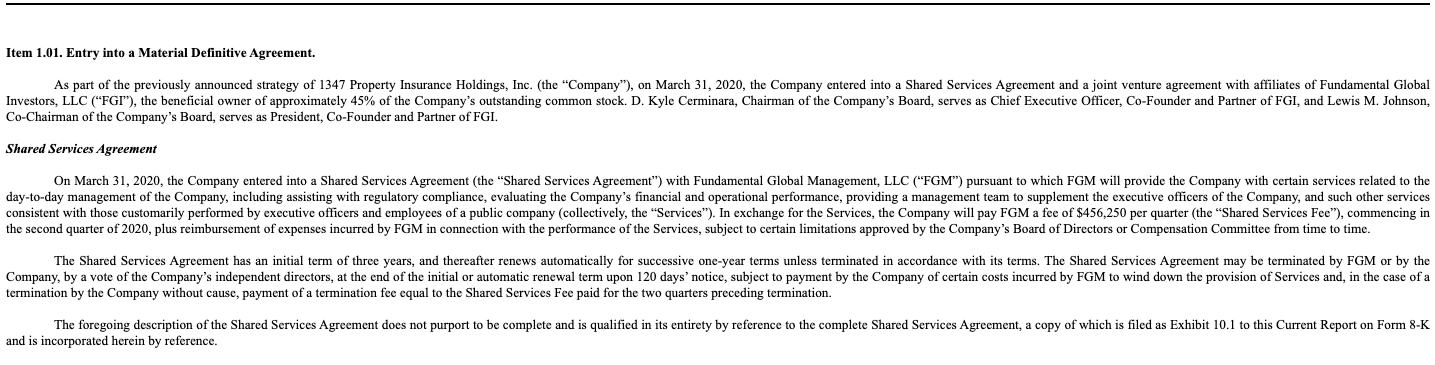

On March 30, 2020, the management of 1347 Property Insurance Holdings issued a press release announcing a June name change for the company to Fundamental Global Financial Corporation, along with plans to launch a reinsurance company, invest in real estate and provide asset management services.

But by April 6, the managers of 1347 Property Insurance Holdings disclosed a “shared services agreement” with a newly created entity, Fundamental Global Management LLC. This agreement requires 1347 Property Insurance Holdings to pay Fundamental Global Management’s owners $1.82 million a year for management and advisory work. While the agreement stated that it was between 1347 Property Insurance Holdings and “affiliates” of Fundamental Global Investors, the “owners” of Fundamental Global Management were not named. One logical guess is that the “owners” are none other than Cerminara, Johnson and Moglia.

A tiny clause in this agreement also assigned 1347 Property Insurance Holdings responsibility for reimbursing Fundamental Global Management for its operating expenses.

The April 6 agreement also announced the formation of a joint venture between 1347 Property Insurance Holdings and Fundamental Global Investors called Fundamental Global Asset Management. This new entity is charged with identifying investment management funds; it will offer to provide them seed capital in exchange for taking equity stakes. Fundamental Global Investors is also granted the right to offer the opportunity to invest in these funds to a “third party” if the amount of capital required is greater than $5 million.

There is a catch: According to a 2018 hedge fund industry study by the Seward & Kissel law firm, even seeding deals for smaller funds can require commitments of $20 million or more. While the April 6 agreement does not explicitly state it, Cerminara and Johnson will likely use Fundamental Global Asset Management to identify and finance smaller investment management firms and tap Capital Wealth’s wealthy clients to fund larger deals.

———————

Cerminara and Johnson’s side deals for Fundamental Global Investors achieved by their dipping into these three public companies’ assets are not the full extent of their quirky dealings with publicly traded enterprises.

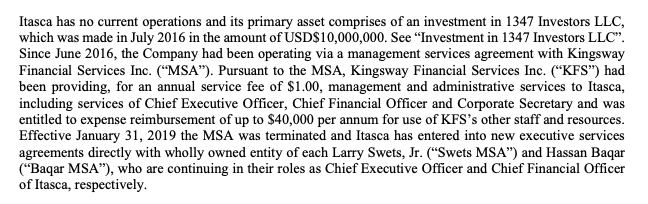

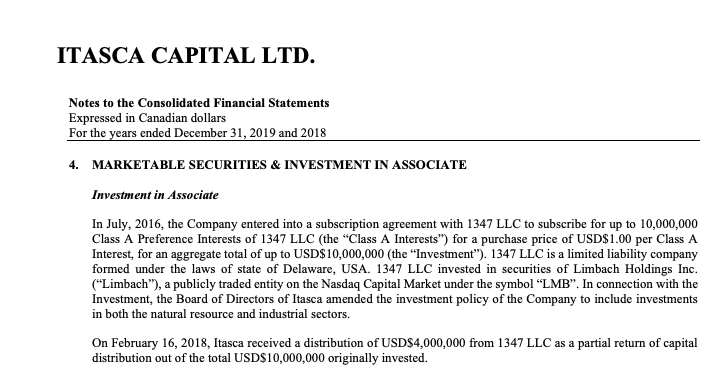

The filings of little-known Itasca Capital of Vancouver may demonstrate the purest expression of Fundamental Global Investors’ use of a public company for private gain. Itasca Capital’s board of directors includes Cerminara and Johnson, and the company has no operations.

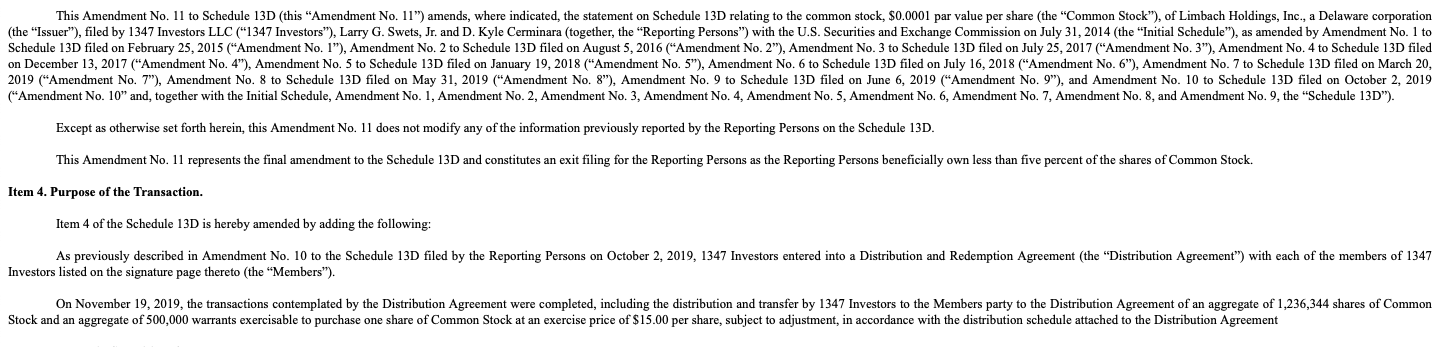

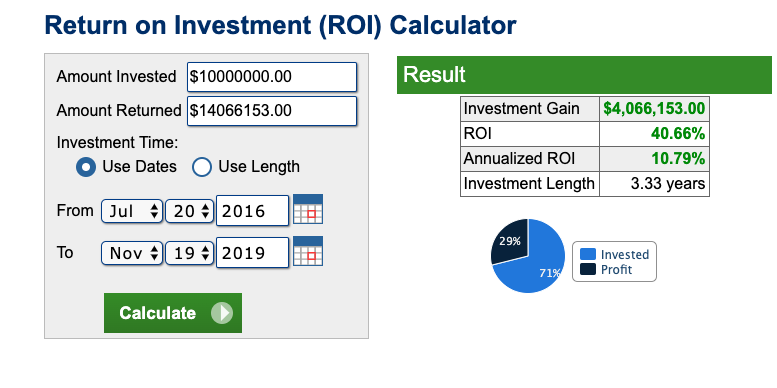

Itasca Capital’s structure is similar to that of a Russian nesting doll: Its only asset is 1347 Investors LLC, a holding company that is jointly managed by Cerminara and Larry Swets Jr. (This second executive, Swets, founded Kingsway Financial Services, a predecessor of 1347 Property Insurance Holdings.) And until very recently, 1347 Investors LLC itself had just a single asset: a $10 million investment in redeemable preferred stock issued by Limbach Holdings, an unprofitable commercial contractor. That investment was redeemed on Nov. 19, 2019, and 1347 Investors LLC netted a respectable 10.79 percent annualized return on the investment for Swets, Cerminara and others.

Under Cerminara and Johnson’s direction, Ballantyne Strong in 2016 spent $3.7 million to purchase shares of Itasca Capital; today Ballantyne Strong owns 32.3 percent of Itasca Capital.

Over roughly three years Ballantyne Strong has received $2.9 million in dividends from Itasca Capital, but that sum must be weighed against $1.2 million in write-downs.

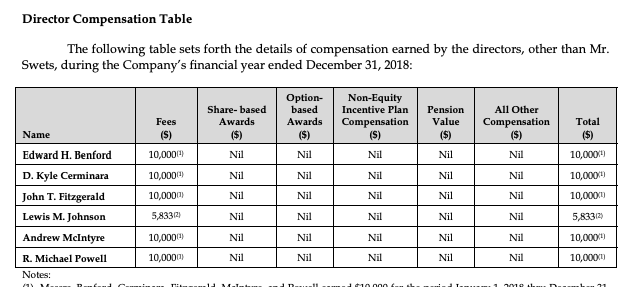

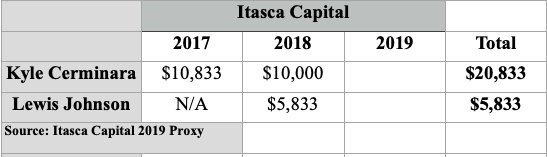

Cerminara and Johnson receive modest annual payments for being members of Itasca Capital’s board of directors. In 2018, the last year for which information is available, Cerminara received $10,000 for being Itasca Capital’s board chairman, and in 2017 he made $10,833. Johnson, who joined the board in 2018, was paid $5,833.

Ballantyne Strong’s investors would be well served to ask why their company still owns Itasca Capital. And Fundamental Global Investors’ limited partners should be curious to know why Fundamental Global Investors did not participate in the profitable 1347 Investors LLC transaction with Limbach Holdings.

———————

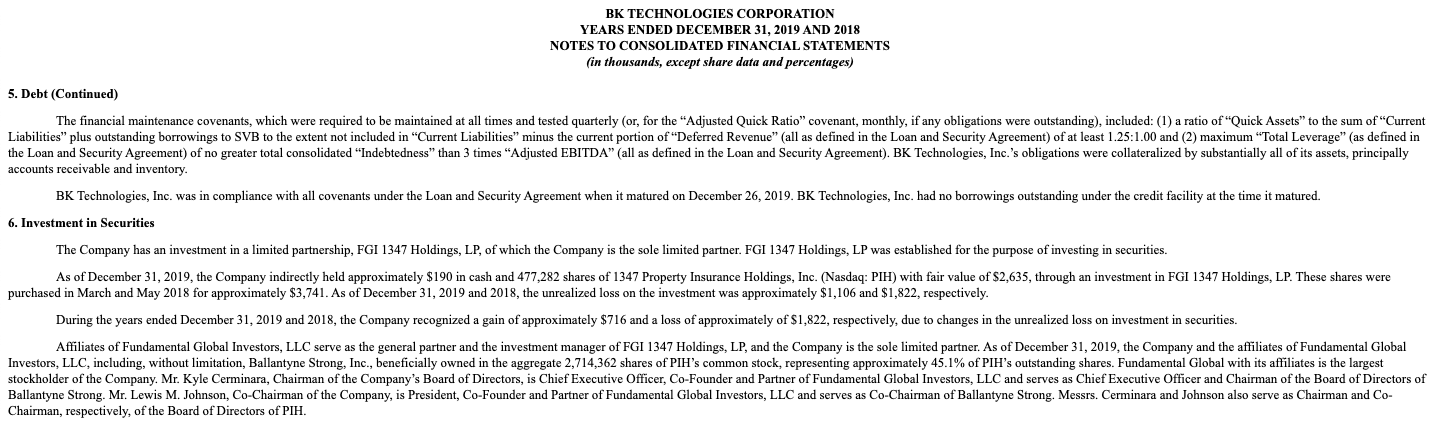

In addition to all their other engagements, Cerminara and Johnson serve as co-general partners of yet another similarly named entity, FGI 1347 Holdings LP. This fund’s sole investor is BK Technologies. Yet FGI 1347 Holdings LP’s only asset, apart from $197,000 in cash, is 477,282 shares of 1347 Property Insurance Holdings. These shares had had been previously purchased by BK Technologies in March and May 2018 for $3.74 million. (BK Technologies disclosed on April 28 that Fundamental Global Investors does not charge any fees for its management of FGI 1347 Holdings LP.)

Tying up almost $4 million in cash, this investment in FGI 1347 Holdings LP must be documented on BK Technologies’ income statement. Thus the swings in FGI 1347 Holdings LP’s value significantly affect BK Technologies’ profits. In 2019, as the share price of 1347 Property Insurance Holdings dropped, the value of BK Technologies’ stake in FGI 1347 Holdings LP declined by $1.1 million, and in 2018 it dipped by more than $1.8 million.

———————

For all Cerminara and Johnson’s other activities and maneuvers, their main claim to fame as financiers – running their nearly 8-year-old hedge fund – has been a dramatic failure from the perspective of its limited partners. Fundamental Global Investors’ filings show the hedge fund, the three main public companies it controls and Capital Wealth’s clients spent $72.67 million on the shares of Ballantyne Strong, BK Technologies and 1347 Property Insurance Holdings. The part of Fundamental Global Investors’ portfolio invested in these three public companies and Itasca is now worth just $37.55 million.

While the Foundation for Fina’ncial Journalism could not obtain Fundamental Global Investors’ exact performance results, Securities and Exchange Commission filings paint an ugly picture of the fortunes of the fund’s limited partners. A comparison of Fundamental Global Investors’ SEC Form D filings since 2012, which list each time it has raised capital, with its most recent Form ADV filing, containing each of its funds’ current value, indicates that the hedge fund’s amount of capital has sharply fallen.

Because most limited partners are content to leave a profitable investment alone, a hedge fund’s capital would typically decline only if realized losses occur or redemptions are made.

From Sept. 6, 2012, to May 21, 2019, Fundamental Global raised a total of $236.75 million for 14 different funds. The fund’s March 30, 2020, Form ADV lists $127.39 million in capital from all these funds.

The Fundamental Global fund that has experienced the most profound decline in assets under management is the Fundamental Global Partners Master Fund LP.

With three different feeder funds that investors have contributed to since September 2012, the Fundamental Global Partners Master Fund LP has taken in $105.18 million. These feeder funds had only a total of $17.92 million in capital left by March 30, 2020. Given the fact that Fundamental Global Partners Master Fund LP has been operating for almost eight years, much of the decline in assets has likely resulted from wealthy investors redeeming their investments.

One fund alone among Fundamental Global Investors’ 14 offerings was a bright spot in 2019: The CWA FGI Special Opportunities Fund LP posted about a 12 percent return. Orchard Global Asset Management manages its portfolio through its Taiga fund, and Cerminara and Johnson have no investment responsibilities for this account. The fund’s $20.3 million in assets were raised in November 2018 primarily from 37 Capital Wealth clients.

———————

The Foundation for Financial Journalism made extensive efforts to obtain comment from the three general partners of Fundamental Global Investors. After an exchange of text messages with Kyle Cerminara, an April 8 email to Cerminara, Johnson and Moglia requested a response to 13 questions. A follow-up email went out on April 20, and Cerminara gave a brief reply. On April 24 another set of 13 questions was sent. On May 3, a last request for comment was made. There was no response.

Corrections: An earlier version of this story erroneously stated that Kyle Cerminara and Lewis Johnson had received a combined $6 million in fees and compensation from Fundamental Global Investors since 2015. But the source of that $6 million was the three public companies they control.

In addition, this article originally stated Cerminara and Johnson had resigned BK Technologies’ board of directors. In fact, they resigned as the board’s co-chairmen but remain directors.

The original version also erred in stating Fundamental Global Investors spent $72.67 million on shares of Ballantyne Strong, BK Technologies and 1347 Property Insurance Holdings. Fundamental Global Investors, the three main public companies it controls and Capital Wealth’s clients purchased this amount. These corrections were made in May 2020.

The piece was also corrected and updated on Dec. 2, 2021, to change the article’s title to reflect the fact that losses to the limited partners of Fundamental Global Investors resulted from its unsuccessful asset allocation strategy, as opposed to abusive conduct by the general partners.

Three paragraphs in the original article incorrectly noted that Capital Wealth Advisors owned a 50 percent stake in Fundamental Global Investors and that a real estate fund FGI Metrolina, then managed by Cerminara and Johnson, had purchased the mortgage of a Ballantyne Strong facility in Alpharetta, Georgia. These paragraphs were deleted.

Update: This article was updated with share prices of May 6, 2020.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}